2016 Software User Survey: Sales are looking “Slightly Questionable”

The demands of e-commerce and omni-channel continue to increase, and the need to work smarter and faster is growing. Yet for the first time in years, it looks like companies are taking a step back to rethink their supply chain software investments.

Latest Material Handling News

C-suite Interview with Keith Moore, CEO, AutoScheduler.AI: MODEX was a meeting place for innovation C-Suite Interview with Frank Jewell of Datex, Leading the Way in the Material Handling Industry Give your warehouse management systems (WMS) a boost Agility Robotics and Manhattan Associates partner to bring AI-powered humanoid robots into warehouses Siemens, Universal Robots, and Zivid partner to unveil smart robotic picking solution More Software

Modern Material Handling’s “2016 Warehousing & Distribution Center Software Usage Study” paints a revealing picture of a reader base that’s willing to test out new applications, not quite ready to make big investments, and is somewhat confused about which software platforms handle what specific functions. Combined, these factors all lent themselves to some interesting results for this year’s Peerless Research Group (PRG) survey of Modern subscribers.

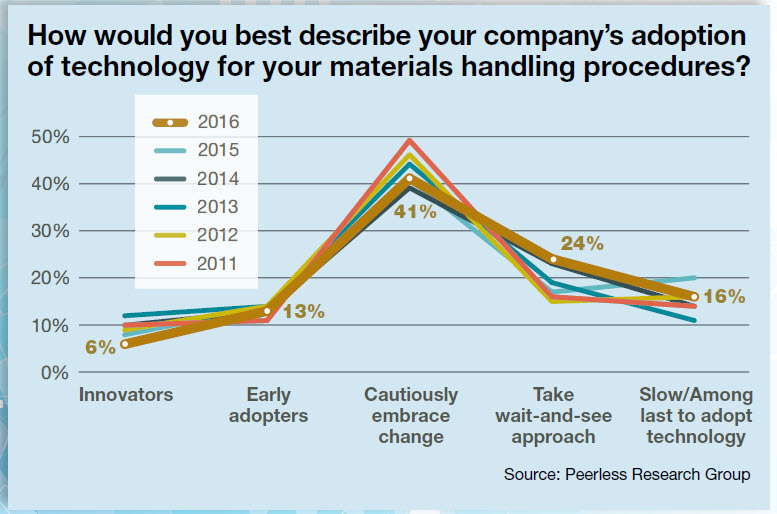

In describing their company’s adoption of technology for materials handling procedures, for example, 41% of readers say they “cautiously embrace change, yet are practical about adopting new technology.” Another 24% say they take a wait-and-see attitude before adoption and tend to wait for the second generation of the technology to come along before jumping in. And, just 13% consider themselves “early adopters” of such technology.

Compare this to 2015, when 17% of readers were taking the wait-andsee approach and 14% called themselves early adopters. “There was a slight change in the adoption curve between 2015 and 2016,” notes Judd Aschenbrand, PRG’s director of research. “What we’re seeing here is more people taking a ‘wait-and-see’ approach rather than categorizing themselves as slow adopters.”

While slight, the change does merit attention, says Aschenbrand, primarily because it could signal a potential reduction in the number of companies willing to jump in and invest in new warehouse and distribution software.

Who’s using what?

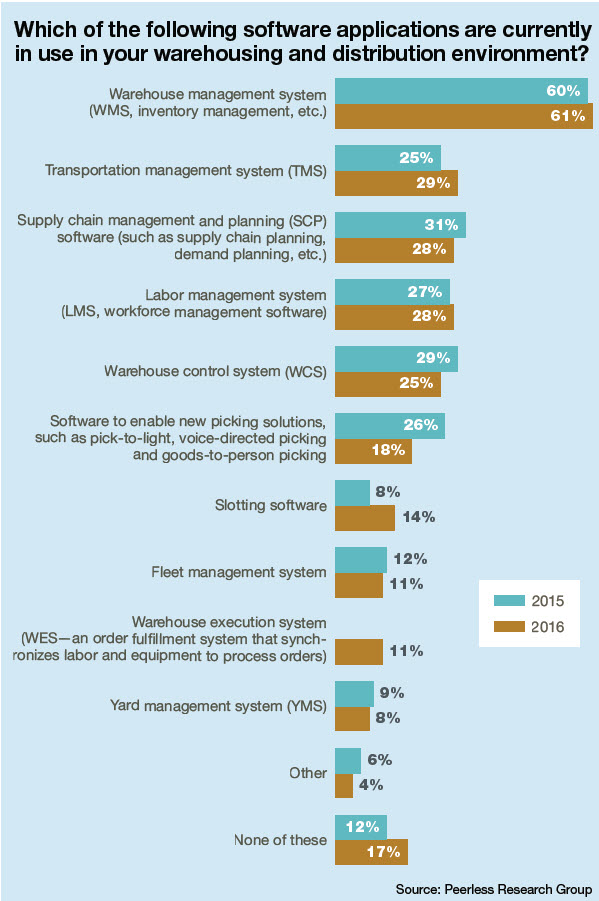

Asked to list the various software applications in use in their warehouses and DCs, 61% have a warehouse management system (WMS), 30% are using a transportation management system (TMS), 29% are using a supply chain management and planning platform (SCP), and 29% use a labor management system (LMS). Other popular applications include warehouse control systems (WCS) at 25%, software to enable new picking solutions (i.e., pick-to-light) at 18%, and warehouse execution systems (WES) at an 11% usage rate.

These usage rates haven’t changed much over the last year. In 2015, for example, readers cited WMS (60%), SCP (31%), WCS (29%), LMS (27%), and software to enable new picking solutions (27%) as the top five software applications currently in use in their warehouse and distribution environments. When asked which solutions they are planning to evaluate, purchase or upgrade within the next 24 months, 38% of readers said WMS, 24% are considering WCS, 17% want to explore their SCP options, and 12% are looking at software to enable new picking solutions.

Clearing up the confusion

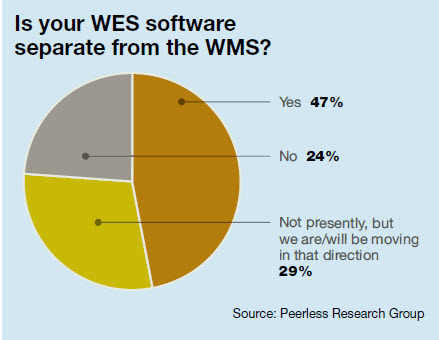

With more companies integrating warehouse automation equipment and software solutions right now, the “WMS vs. WCS vs. WES” discussion is becoming more germane for firms that aren’t sure which of the three that they need (or, if they need all three). When asked if their WES is separate from their WMS, 48% of readers said “yes” and 24% said “no.” In terms of the activities that the WMS controls, readers said the solutions handle receiving, put away to storage, picking, order management and wave planning, and inventory management. On the WES side, they said packing and sorting, shipping, order management and wave planning, and picking.

John Hill, a veteran warehousing expert and consultant at St. Onge Co., said these responses prove the need for better education on WMS, WCS and WES and the role that each plays in the warehouse or DC. “I think the market is confused,” says Hill. “I can make four phone calls right now and ask, ‘What’s a WES?’ and I can guarantee that I will get four different answers. The industry has an obligation to help clear this up—primarily on the supplier side, but also on the side of the market pundits who keep track of what’s going in the marketplace.”

Answering a question that was new to this year’s survey, most companies (80%) are not currently using a distributed order management (DOM) solution to determine the best location from which to source an order when inventory is stored in multiple locations (i.e., stores, multiple DCs, drop ship from a supplier, etc.). We found that 20% of readers say their DOM software considers the following when looking to determine the best location to source an order from: inventory levels (50%), customer requirements (41%) and transit time (37%).

Breaking down the categories

In looking at current software usage among readers, the survey broke down the top categories (WMS, TMS, YMS, SCP and LMS) to find out how long each solution has been in place, when it was last upgraded, and how long it took to realize the return on investment (ROI) for each platform. For WMS, the majority (35%) of companies have had their system in place for less than 10 years while 31% have been using their current WMS for less than five years. The bulk of these systems (46%) were last upgraded less than five years ago and another 17% upgraded their systems less than 10 years ago.

In terms of realizing ROI, most WMS users (34%) have yet to realize their return on investment or “don’t know” if that benchmark has been achieved yet. About 52% of WMS users are leveraging their system’s analytics capability for tasks like evaluating key performance indicators (KPIs), outbound/ shipping, inventory management, inbound/receiving, and order management, among other functions.

For TMS, 38% of companies have had their systems in place for less than 10 years and 28% for fewer than five years. Most of these solutions (38%) were upgraded less than five years ago and 21% less then 10 years ago. According to 25% of readers, it took an average of 12 to 18 months to realize the ROI on their TMS investments, while another 21% say they’ve yet to realize a return (or, don’t know if they have or not). For SCP, most systems (40%) have been in place for less than 10 years, have been upgraded in the last five years (32%), and have yet to meet ROI expectations (46%). Most companies are using the latter to manage inventory visibility, order management, demand and planning, and procurement. Looking ahead, readers expect to buy or upgrade SCP to manage initiatives like order management, procurement, demand planning and collaborative forecasting.

Addressing key challenges

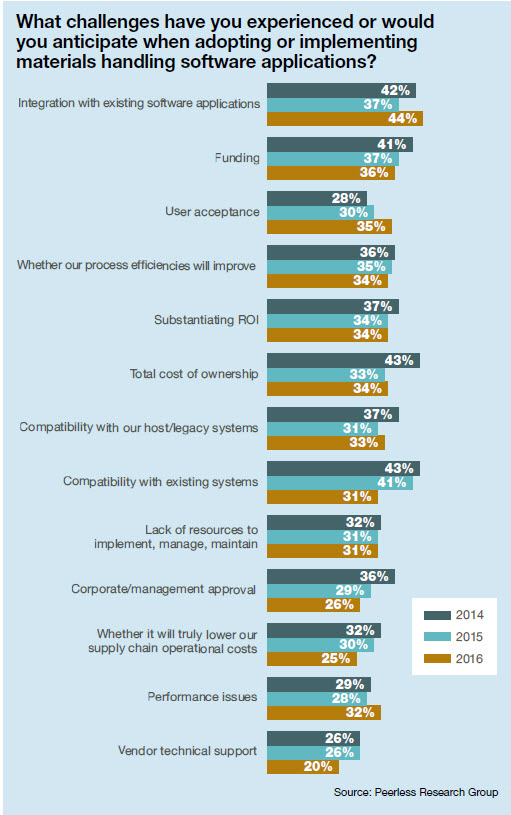

Readers were also asked what challenges they’ve experienced— or, that they anticipate facing—when adopting or implementing materials handling software applications. For 2016, the most popular responses included integration with existing software applications (44%), substantiating ROI (34%), understanding whether process efficiencies will improve (34%), and compatibility with host/legacy systems (33%).

Last year, the biggest issues cited by readers were compatibility with existing systems, integration with existing software applications, funding, and whether process efficiencies will improve. “We saw the ‘compatibility with existing systems’ issue fall from 41% to 31% over a year’s time,” Aschenbrand points out. “This could mean that whatever solutions that companies are embracing, the levels of compatibility among different systems could be becoming less of an issue or challenge.”

The crystal ball

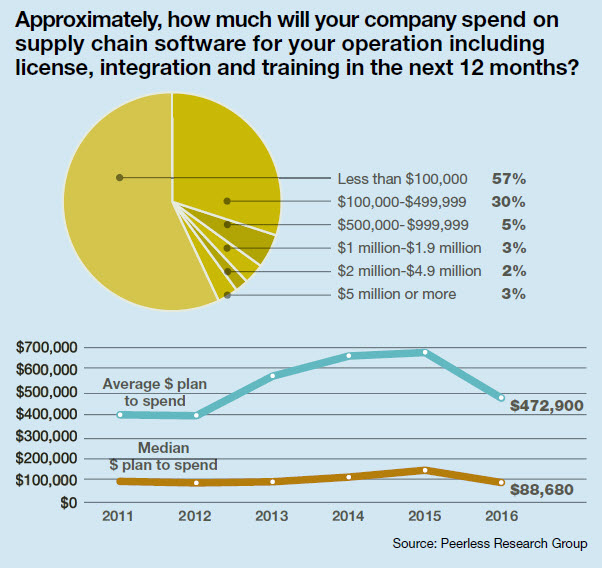

Looking out over the next 12 months, most companies (56%) expect to spend less than $100,000 on supply chain software for their operations (including licenses and integration). Another 30% of readers plan to spend $100,000 to $499,000, while 5% expect to spend $500,000 to $999,999 for supply chain solutions. Compare this to last year, when 47% of respondents were expected to spend less than $100,000; 23% were on target to spend $100,000 to $499,999; and 16% were slated to buy $500,000 to $999,999 in supply chain software.

Overall, Hill says he’s not shocked or surprised by the results of this year’s software usage survey, although he is “puzzled” by some of the individual statistics. For example, he says the idea that seven of the top challenges associated with software purchases have to do with funding and justification in an era where e-commerce and omni-channel distribution are driving the need for automation and speed in the warehouse is not an encouraging sign.

“Prospective users need to spend more time identifying why they should even be interested in one of these systems, and doing the research necessary to determine where the payback is most likely to be,” says Hill. “I don’t know why more people don’t do this at the outset.”

Looking ahead, Hill says the industry as a whole has some work to do when it comes to educating users on the merits and value of the many different types of supply chain software that are now coming together to create a complete, streamlined warehousing operation.

“The statistics on actual [supply chain software] spending are not as good right now as they are for some other commodities or services that the industry offers,” says Hill, who notes that MHI’s most recent data reflects a similar trend. “The industry has had a pretty good ride over the last few years. This is the first time since 2013 that things are looking slightly questionable.”

Respondent demographics

Modern’s annual Software Usage Study collected responses from 109 top materials handling professionals. To qualify, respondents must be personally involved in using, evaluating or purchasing software for their company’s materials handling operations.

This year’s respondents reflect management at all levels across both manufacturing and non-manufacturing vertical industries. Upper level management, meaning vice presidents, general managers and division managers, accounts for 32%, while 55% are responsible for managing their company’s logistics distribution, warehouse, supply chain, operations or purchasing functions.

A number of vertical markets were represented, including food and beverage (15%), chemicals and pharmaceuticals (5%), automotive and transportation (5%), and printing and paper goods (5%). On the non-manufacturing side, wholesale trade (13%), transportation/warehousing services (3%), retail trade(4%) and third-party logistics providers (7%) were among the respondents

Article Topics

Software News & Resources

C-suite Interview with Keith Moore, CEO, AutoScheduler.AI: MODEX was a meeting place for innovation C-Suite Interview with Frank Jewell of Datex, Leading the Way in the Material Handling Industry Give your warehouse management systems (WMS) a boost Agility Robotics and Manhattan Associates partner to bring AI-powered humanoid robots into warehouses Siemens, Universal Robots, and Zivid partner to unveil smart robotic picking solution OTTO Motors showcases latest software release for optimizing floor space Rite-Hite ONE digital platform debuts More SoftwareLatest in Materials Handling

Registration open for Pack Expo International 2024 Walmart chooses Swisslog AS/RS and software for third milk processing facility NetLogistik partners with Vuzix subsidiary Moviynt to offer mobility solutions for warehouses Materials Handling Robotics: The new world of heterogeneous robotic integration BSLBATT is looking for new distributors and resellers worldwide Lucas Watson appointed CSO for Körber’s Parcel Logistics business in North America Hyster recognizes Dealers of Distinction for 2023 More Materials HandlingAbout the Author

Subscribe to Materials Handling Magazine

Find out what the world's most innovative companies are doing to improve productivity in their plants and distribution centers.

Start your FREE subscription today.

April 2024 Modern Materials Handling

Latest Resources