MAPI Survey on the Business Outlook: Index shows slight advance

Composite index edges pp to 56 from 55, breaking 10 straight quarterly declines.

Latest Material Handling News

Beckhoff USA opens new office in Austin, Texas Manhattan Associates selects TeamViewer as partner for warehouse vision picking ASME Foundation wins grant for technical workforce development Consultant and industry leader John M. Hill passes on at age 86 Registration open for Pack Expo International 2024 More NewsThe results of the quarterly Manufacturers Alliance for Productivity and Innovation (MAPI) Survey on the Business Outlook (EO-123) indicate improvement, albeit marginal, from the previous report, and imply that the manufacturing sector is holding its own in uncertain economic times.

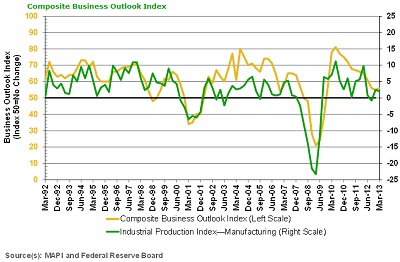

The survey’s composite index is a leading indicator for the manufacturing sector. The March 2013 composite index advanced to 56 from 55 in the December 2012 survey. That breaks a string of 10 consecutive quarterly declines. The index remains above the threshold of 50 for the 14th straight quarter, the dividing line that separates contraction and expansion.

“The March survey results offer a mixed bag,” said Donald A. Norman, Ph.D., MAPI senior economist and survey coordinator. “On the positive side, the composite index ended a long slide, and there is good news in the upswing in the investment indexes and in the profit margin index. Most of the other indexes, however—including current orders, prospective shipments, exports, backlog orders, and capacity utilization—all fell. The outlook over the next three to six months remains the same—growth at a slow pace.”

The Composite Business Outlook Index is a weighted sum of the Prospective U.S. Shipments, Backlog Orders, Inventory, and Profit Margin Indexes. In addition to the composite index, which reflects the views of 59 senior financial executives representing a broad range of manufacturing industries, the survey includes 13 individual indexes that are split between current business conditions and forward looking prospects.

While the overall composite index showed a slight gain, 9 of the 13 individual indexes decreased, including 5 of the 6 current business condition indexes.

Current Business Condition Indexes:

- The Profit Margin Index was a bright spot, improving to 62 in March from 59 in December.

- The Inventory Index, based on a comparison of inventory levels in the first quarter of 2013 with those in the first quarter of 2012, dropped to 48 in March from 54 in December. According to Norman, this could be considered an indicator of future strength in that continued production growth will eventually require an inventory build.

Other areas were more problematic.

- The Capacity Utilization Index, which shows the percentage of firms operating above 85 percent of capacity, dropped to 20.7 percent in March from 31.5 percent in December. The long-term average is 32 percent.

- The Current Orders Index, a comparison of expected orders in the first quarter of 2013 with those in the same quarter one year ago, fell to 47 from 57 in the previous survey.

- The Export Orders Index, which compares exports in the first quarter of 2013 with the same quarter in 2012, also saw a decline, to 45 in the current survey from 49 in the previous report.

- The Backlog Orders Index, which compares the first quarter 2013 backlog of orders with that of one year earlier, fell to 43 in March from 45 in the December report.

Forward Looking Indexes:

Three of the seven forward looking indexes increased.

- The U.S. Investment Index is based on executives’ expectations regarding domestic capital investment for 2013 compared to 2012. The index was 64 in March, a solid increase from 56 in the December survey. The Non-U.S. Investment Index, based on projections regarding capital expenditures abroad in 2013 compared to 2012, advanced to 62 in the current report from 59 in December.

- The Interest Rate Expectations Index increased to 58 from 51, indicating that a growing majority believes that longer-term interest rates will rise by the end of the second quarter of 2013.

- The Annual Orders Index, based on a comparison of expected orders for all of 2013 with orders in 2012, decreased to 74 in March from 78 in December. Still, at 74, this index remains at a relatively high level.

- The Prospective U.S. Shipments Index, which reflects expectations for second quarter 2013 shipments compared with those in the second quarter of 2012, declined to 61 in March from 63 in December. The Prospective Non-U.S. Shipments Index, which measures expectations for shipments abroad by foreign affiliates of U.S. firms for the same time frame, dropped to 53 in the current report from 57 in the December survey.

- The Research and Development Spending Index surveys participants regarding R&D spending in 2013 compared to 2012. The index was 68 in the March report compared with 69 in December.

- In a supplemental section, participants were queried on issues concerning cybersecurity.

- Nearly two-thirds of the respondents (64 percent) report that their company has been subject to attempts to obtain proprietary data over the past two years. Eighteen percent indicated there have been six or more attempts to obtain data.

- ● A malicious attack aimed at disrupting a company’s website is the most common goal of computer hackers, cited by 46 percent of the respondents. The second most common type was aimed at obtaining technical specifications on products or information on production processes, cited by 24 percent of the respondents.

- ● Most companies (83 percent) have put in place new technologies to detect attempts to hack into their computer systems and 19 percent are developing new technologies.

MAPI’s Composite Business Outlook Index (see chart below) is a historically accurate near-term preview of business prospects for the manufacturing sector and is a leading indicator of the Federal Reserve’s industrial production index.

Article Topics

Latest in Materials Handling

Beckhoff USA opens new office in Austin, Texas Manhattan Associates selects TeamViewer as partner for warehouse vision picking ASME Foundation wins grant for technical workforce development The (Not So) Secret Weapons: How Key Cabinets and Asset Management Lockers Are Changing Supply Chain Operations MODEX C-Suite Interview with Harold Vanasse: The perfect blend of automation and sustainability Consultant and industry leader John M. Hill passes on at age 86 Registration open for Pack Expo International 2024 More Materials HandlingSubscribe to Materials Handling Magazine

Find out what the world's most innovative companies are doing to improve productivity in their plants and distribution centers.

Start your FREE subscription today.

April 2024 Modern Materials Handling

Latest Resources