Top 20 3PL warehouses, 2012

Following a post-recession bump, third-party logistics providers are on track to stay flat through 2013.

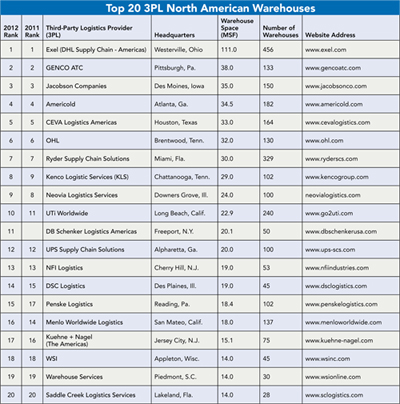

Each year, Modern takes look at the Top 20 third-party logistics (3PL) warehouses to see who’s leading the way in regard to total square footage of storage space. This year’s annual ranking again reflects the general state of the economy, with 2011’s strong performance followed by weaker growth in 2012. Read last year’s list.

This year, we have once again called upon Dick Armstrong, chair of Armstrong & Associates, who closely follows the 3PL sector of the warehousing industry, for his insight. Armstrong predicts 3PL warehousing revenues for 2012 and 2013 will grow by about 6% each year. This follows 8.2% growth in 2011.

In terms of overall square footage, some adjustments to reported figures make an apples-to-apples comparison for the entire Top 20 a bit tricky. At 547 million square feet, this year’s Top 20 sum would appear less than 1% larger than last year’s 543 million. However, square footage for the top eight, whose rankings and reporting practices remain unchanged, has grown by 5.8%. Overall, Armstrong called the growth in square footage modest, and said new construction is very limited.

The value-added segment of 3PL warehousing, which represents about 26%, or $35 billion of the $131 billion 3PL market, has been the fastest-growing segment. The predicted total 3PL market value for 2012 is $142 billion, an 8.4% increase. But growth in net revenues for warehousing tends to be about three times the annual growth in gross domestic product (GDP), according to Armstrong. This year, the International Monetary Fund (IMF) predicted 2013 GDP growth of 1.5%, as compared to 1.3% in 2012 and 1.6% in 2011. Armstrong cited these figures as the basis for his predicted 6% growth in net revenues for 3PL warehouses in 2012 and 2013.

“We’re going to see single-digit revenue growth that’s nothing to get excited about,” says Armstrong. “That reflects where we are in the economy. Anything above 6% in 2013 would surprise me, and in the worst possible case it will only grow by 2% or 3%, but we won’t see negative growth.”

The worst possible scenario essentially revolves around the fiscal cliff and the potential for large government spending cuts, says Armstrong. Although the election is behind us, uncertainty still looms.

“This will be a very challenging year, with the possibility of a global recession,” he says. “There’s only so much the United States can do, given what’s happening throughout the world.”

What 3PL warehousing companies can do is hold their own and continue to nurture the largely organic growth that characterizes this year’s Top 20 list. The top seven companies have remained in the same ranking as last year, with Exel (DHL Supply Chain) pulling even further ahead of the pack. Exel’s current 111 million square feet under management is a full 16.8% greater than last year’s 95 million.

In second place, Genco ATC tacked on another million square feet for a total of 38 million. The only other shift in square footage for the top seven companies is the addition of 1.8 million square feet for OHL, which Armstrong again credited to organic growth.

Kenco Logistics added 4 million square feet, moving from 25 to 29 million and from ninth to eighth place. No. 9 is Neovia Logistics Services, formerly Caterpillar Logistics Services, which last year reported 29 million square feet. Armstrong says the reduction of 5 million square feet is a result of the dedicated Caterpillar facilities being broken out from other contracted warehousing, which now reports as Neovia.

Last year’s 10th place finisher, APL Logistics, has fallen out of the top 20, ranking 22nd with 12 million square feet. Armstrong credited cleaner reporting figures for the shift from last year’s 24.7 million square feet. The new figure now represents only pure warehousing, excluding transportation terminals, forwarding stations, container stations and the like.

DB Schenker jumped into 10th place with 20.1 million square feet after ranking 20th in 2010 and just missing the list last year with only about 12 million square feet. Armstrong said Schenker’s global footprint had been particularly strong in Canada, where it recently landed some key big box retail accounts.

DSC Logistics and Penske Logistics posted gains in the last year that bumped Menlo Worldwide—whose square footage has not changed—from 14th to 16th place. Armstrong credited DSC’s gains to expansion among its existing customer base, while Penske is successfully transitioning from an automotive focus to incorporate customers in food and electronics as well. At 18.4 million square feet, Penske is up 23.5% over last year’s 14.9 million.

For the most part, says Armstrong, warehousing space is available in North America, with the exception of those regions feeding New York and New Jersey and the Inland Empire in California. “Those were the only places I saw where availability was in the low single digits,” says Armstrong. “Customers in those areas might have difficulty finding a large, modern warehouse.”

Trends for 2013

The big get bigger: Last year, Armstrong predicted “mom and pop” standalone operations would lose ground to global players. Advances in technology and visibility have fueled this transition, he says.

“The growth areas for value-added services, such as pharmaceutical and refrigerated grocery, are being dominated by the large players,” says Armstrong. “The ‘pallet in, pallet out’ warehouses might not require that kind of sophistication, but those in need of sophisticated value-added services are being driven to the larger, more capable players.”

As Top 10 companies get stronger in North America and become more involved in the global supply chain, more customers look to them for end-to-end services and transportation management. These large players can handle product from origin to destination, says Armstrong, with advanced software to provide visibility and traceability through the entire supply chain.

The fall spike is DOA: With increased globalization of economic activity, a strong Black Friday and Christmas shopping season is not going to tip the scales, says Armstrong. European and Asian fluctuations are of much more concern. Still, the holiday season, until recent years, marked a notable spike for North American warehousing.

“If you look at the containers and ocean trade, it’s just not anything robust and exciting. For so many years we had a fall surge that was very dramatic, with a lot of good shipment,” says Armstrong. “Because it was good for business, it was good for third-party logistics. But we’re certainly not going to see the fall surge that many of us came to love.”

Bringing transportation management back in-house: Many will try, few will succeed. The growing value-added capabilities of many 3PLs will ensure that most of their clients will not try to duplicate those strengths in an effort to bring that part of the business back in-house. However, transportation management calls for much less intensive— though still significant—IT and management costs.

“I don’t recommend taking transportation back in-house, but people will try because it seems more affordable,” says Armstrong. “It’s a leadership decision, and those who make the decision to take it in-house, having moved in that direction, are likely to find their operations become more mediocre. They might find that they would have been better off negotiating with a transportation manager who specializes in those capabilities without taking away from their own core capabilities to manage that.”

Article Topics

Special Reports News & Resources

Automation/Retail Special Issue: Savvy users embrace change Research Report: Use of Automation in Warehouse/DC Special Digital Issue: Warehouse/DC Robotics System Report: Building the world’s best warehouse Top 20 Warehouses 2019 Top 20 automatic identification and data capture suppliers 2019 Top 20 Lift Truck Suppliers in 2019: Market reaches new heights More Special ReportsLatest in Materials Handling

Registration open for Pack Expo International 2024 Walmart chooses Swisslog AS/RS and software for third milk processing facility NetLogistik partners with Vuzix subsidiary Moviynt to offer mobility solutions for warehouses Materials Handling Robotics: The new world of heterogeneous robotic integration BSLBATT is looking for new distributors and resellers worldwide Lucas Watson appointed CSO for Körber’s Parcel Logistics business in North America Hyster recognizes Dealers of Distinction for 2023 More Materials HandlingAbout the Author

Subscribe to Materials Handling Magazine

Find out what the world's most innovative companies are doing to improve productivity in their plants and distribution centers.

Start your FREE subscription today.

April 2024 Modern Materials Handling

Latest Resources

{kind=link}