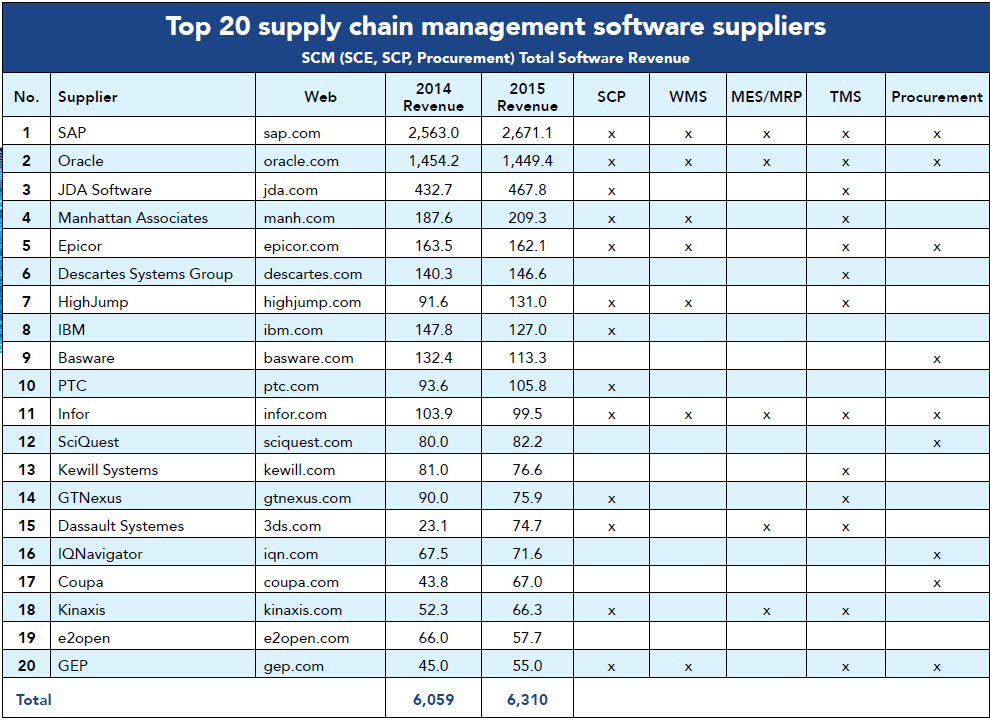

Top 20 supply chain software suppliers, 2016

The market for conventional solutions continues to rise, even as innovative variations help the industry chart a new course.

Latest Material Handling News

Automation/Retail Special Issue: Savvy users embrace change Research Report: Use of Automation in Warehouse/DC Special Digital Issue: Warehouse/DC Robotics System Report: Building the world’s best warehouse Top 20 Warehouses 2019 More Special Reports

The story for the 2015 market for supply chain management (SCM) software, maintenance and services is a tale of two currencies, according to Chad Eschinger, vice president at the research firm Gartner.

Measured in current currency—that is a comparison of results based on currency values for 2014 and 2015—the market grew by about 2.8% to $10.145 billion. That total includes applications for supply chain execution (SCE) (+3.4%), supply chain planning (SCP) (+3%) and, for the third year in a row, procurement software (+1.9%), which is increasingly integrated with supply chain management. Growth is growth in a tough economy, but 2.8% is not much more than last year’s yield on a 10-year treasury note.

If you look at the market in constant currency, you get a different story, according to Eschinger. Now, that $10.145 billion translates into an 11% gain, or the equivalent of a pretty good growth stock. Individually, SCE grew by 11%, SCP grew by 11.3% and procurement grew by 10.8%. “As you can see, there was ample demand for supply chain software last year,” he adds. “But currency values created a 7% headwind, even for market leaders like SAP and Oracle.”

Looking forward, Gartner is predicting a compound annual growth rate (CAGR) in constant currency for supply chain management software— including procurement—of 9.5% for the next five years, reaching $16.283 billion in 2020.

The drivers behind that growth are a familiar story. “As in years past, organizations are trying to gain visibility both internally and externally,” Eschinger says. That said, analytics is driving more software-related projects within supply chain organizations, as is network redesigns, sales and operations planning (S&OP), and integrated business planning initiatives.

“We are seeing providers like SAP launch initiatives to incorporate information from customer relationship management (CRM) systems, financial systems and other functions besides supply chain into the S&OP process to get a fuller view on the dashboard of what’s going on in the organization,” Eschinger adds. What’s more, there is a bit of a refresh cycle going on, as companies upgrade or replace aging systems to gain new functionality.

Last, but not least, the challenges wrought by the globalization of business is having an impact on the overall supply chain management space. Smaller vendors, for instance, are struggling with expansion into new regions where their clients are staking out territory and want support. That is compounded in regions like mainland Europe and Brazil, where there are country-specific markets and suppliers. Cloud providers are also contending with privacy issues.

“In Canada, you can’t let data leave the border, so you have to find local telco or hosting providers, or you can’t do business,” says Eschinger. “Latin America doesn’t have that issue.”

Inside the numbers

Market leaders in the broad category of supply chain management continued to capture the lion’s share of the market in 2015, with the Top 5 providers once again accounting for nearly 49% of the total market.

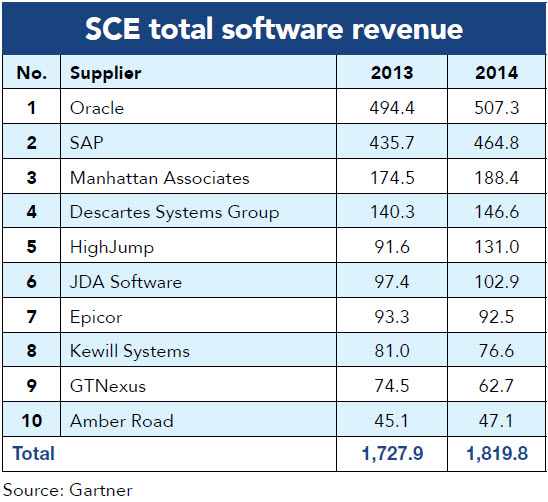

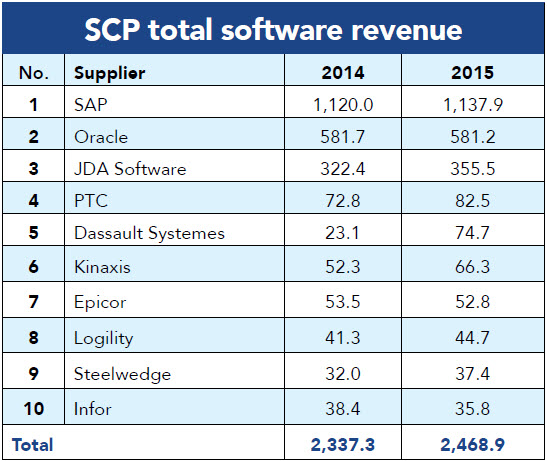

The individual market segments also posted impressive gains. For instance, supply chain execution systems, which includes warehouse management systems (WMS) and transportation management systems (TMS), topped $3.155 billion, with nearly 46% of revenues going to the top five providers. Meanwhile, the market for supply chain planning systems rose to $3.785 billion, with the top five companies accounting for nearly 59% of the list’s total revenues.

The same top five market leaders have dominated the list since at least 2012, with SAP ($2.671 billion), Oracle ($1.449 billion), JDA ($468 million), Manhattan Associates ($209 million) and Epicor ($162 million) leading the pack. Collectively, those five companies have added nearly $1.1 billion in SCM revenues since 2012. Only Epicor showed a year-over-year decline of about $1.4 million, with $162.1 million, down from $163.5 million in 2014.

From there, it’s a tightly packed bunch. Less than $100 million separates fifth-place finisher Descartes Systems Group ($147 million) from GEP, one of the procurement leaders and No. 20 on the list with $55 million.

Notable trends

Several trends were at work last year in each of the four categories relevant to our readers: enterprise resource planning (ERP) and supply chain planning, WMS, TMS and manufacturing execution systems (MES).

SCM: When Modern created our first list in 2002, procurement software was hardly a blip on the radar screen and supply management, as it’s referred to by many, it was barely a discipline, let alone a supply chain function. Things have changed as companies increasingly look at procurement as a partner in supply chain management processes, ranging from new product development to manufacturing to distribution and transportation. The result is a push to automate procurement processes, everything from managing direct and indirect spend to the procure-to-pay process.

“Some of the highest-flying software providers, like Coupa (No. 17 on the list with $67 million in revenue) are in the procurement space,” says Eschinger. One reason is that CFOs are paying attention to procurement as companies get leaner and grapple with thinner margins. Another is the recognition that how a company’s supply base performs can be crucial to how a company is perceived. “If you have one supplier that botches everything, it’s your reputation that gets hit,” says Eschinger.

Traditional ERP players are now facing competition from cloud providers, which is getting a serious look from users and best-in-class providers are outpacing traditional suite providers like SAP, Oracle, Epicor and Infor. “SAP and Oracle are pivoting to launch new cloud-based products,” says Eschinger. “Meanwhile, companies like NetSuite have already caught the wind and are growing by 30% to 40% year over year.”

SCP: The last year in supply chain planning was a mixed bag. Software providers who focused on S&OP, such as Steelwedge and Kinaxis, delivered 20% growth. Slimstock, known for its inventory optimization and S&OP solutions, posted growth of nearly 30%. Meanwhile, traditional planning providers “just plugged along,” says Eschinger. Gartner is also keeping an eye on Manhattan Associates and JDA, two leaders with a foot in the SCP and SCE spaces. While both are still driven primarily by their WMS businesses, Eschinger says they are benefiting from their abilities to provide a supply chain software platform that brings together WMS, transportation and planning, especially in the hot retail market.

What to watch in WMS

In the supply chain execution space, Gartner vice president Dwight Klappich notes several important trends, some of which will be familiar to readers of last year’s list, starting with the WMS space.

- Cloud gains ground

According to Klappich, WMS in the cloud is ready to ramp up. “Three or four years ago, cloud WMS wasn’t really an option,” Klappich says. “Today it may not be the first choice of end users, but there is a lot of interest.”

Klappich cites three numbers to make his point: The cloud has only 5% market penetration, yet Gartner research indicates that 25% of companies will favor the cloud in their next go around and 50% say they would consider it, but they’re just not looking now. Three key developments have led to interest: One is that performance is no longer an issue and WMS providers have adequately addressed security concerns.

More importantly, customers recognize there is a significant upfront cost advantage to a cloud WMS. As cloud proliferates, Klappich says two models are emerging: Large companies want a dedicated cloud and a single instance of the application just for them, which allows them to customize the solution for their needs. Small- to mid-sized companies are going with a multitenant model where a single instance of the software is used by multiple customers.

More importantly, customers recognize there is a significant upfront cost advantage to a cloud WMS. As cloud proliferates, Klappich says two models are emerging: Large companies want a dedicated cloud and a single instance of the application just for them, which allows them to customize the solution for their needs. Small- to mid-sized companies are going with a multitenant model where a single instance of the software is used by multiple customers. - WMS goes international On the day we spoke, Klappich was scheduled to take two calls with end users from Asia, highlighting the growing interest in WMS in other parts of the globe. “Most revenue is still coming from North America but eventually, we’ll run out of warehouses without a WMS,” says Klappich. “Now, as we’re coming out of the downturn, there are vast numbers of manual warehouses in Europe and Asia that are still operating like we operated in the 1980s. They want to look at best practices and a WMS is a first step into automation.” Those facilities may not be ready to jump into the deep end of the functionality pool, he adds, but basic WMS applications like those from the ERP players can deliver gains. Klappich also notes that cloud providers like Logfire have done particularly well in regions such as Latin America.

- Automation is here In the last few years, there has been a marked increase in the amount of automation in warehouses and distribution centers. That has opened the market for warehouse execution systems, or WES, to control processes that once may have been managed by a WMS.

- Distributed order management The market forces driving the push for automation, such as multi-channel retail order fulfillment and that eternal quest for visibility, are driving the adoption of distributed order management (DOM). Sitting between ERP and SCE systems, DOM provides visibility into the orders that need to be filled as well as the location of available inventory an transportation resources. That allows it to orchestrate order fulfillment processes based on rules. “DOM is especially useful in organizations that have multiple ERP systems and want to present one face to the customer,” Klappich says. “It’s also being adopted by manufacturers selling through distributors.” Klappich sees further opportunities in industries like health care. “I’ve seen sales people in the medical device industry spend hours on the phone looking for a part that’s needed in an emergency,” he says. “Wouldn’t it be nice if they had all the hospitals and warehouses in their system plugged in so they had visibility and could send a courier to the nearest available location to pick up the part?”

What to watch in TMS

In the TMS space, Klappich is following several trends:

- Serving the mid-market The most important development in TMS has been the growth of solutions for the mid-sized shipper. “TMS has historically focused on large shippers who spend more than $100 million a year on freight,” Klappich says. “The Oracles, JDAs, Manhattans and SAPs of the world have broad offerings with powerful optimization engines for that market. But midsized shippers don’t need all that power and they’re not going to exploit that optimization if they’re only sending five trucks a day out of their DC.” Klappich says that TMS providers like MercuryGate, Cloud Logistics and Kewill are going to market with solutions that are easy to get up and running and easy to use, many of which are cloud based.

- Going global As with the broad category of supply chain management, TMS is going global, for the same reasons driving the global expansion of WMS.

- It’s all about the network TMS is tapping into the power of networks of transportation providers. In the past, Klappich says, networks tended to be application specific. “You might have a great network, but a poor TMS system or a great application, but no network,” he says. “Today, the leading TMS providers are building interfaces into multiple networks of transportation providers for rail, trucking and international ocean. They’re removing that barrier for the client.”

MES on the move

In comparison to the supply chain planning and execution spaces, the manufacturing execution (MES) space has always been fragmented and difficult to quantify. That remains the case today, according to Rick Franzosa, a research director and author of Gartner’s MES Market Guide. “It’s always been frustrating to pin down a precise definition of MES, and each of the 15 industry verticals tracked in the Market Guide has a relatively small number of players.

It has also been a dynamic market, with a significant number of acquisitions over the past decade. Once a supplier gets above $30 million in revenue, it is often a candidate for acquisition by a bigger player.

With those caveats, Gartner pegs the MES market at roughly $3 billion in revenues split into four areas:

- Operational technology suppliers make up about 60% of the MES market, and include companies such as Rockwell Automation, GE Intelligence Platforms and Honeywell that include some MES capability in their core businesses.

- ERP suppliers like Oracle, SAP, FlexSystem and Epicor.

- Companies focused on product lifecycle management (PLM) and CAD/CAM engineering, including Siemens and Dassault Systems.

- Pure-play suppliers, which comprise 11% of the MES market.

One important driver is the need for systems that can analyze the huge amounts of data now being collected on the shop floor to find the needle in the haystack that can move a business. “This goes beyond platform optimization and is aimed at improving the network, global capacity, demand sensing, product mix coordination, line switches and more,” Franzosa says. “The customer wants personalization and wants it yesterday.”

In addition to improved analytical functionality, companies are also considering a solution’s form. “Consumer technology is so far ahead of corporate technology, and many are wondering why they work on a green screen when they have an iPad at home,” Franzosa says.

Cloud is also a contender in MES, where Franzosa says the solutions are much more effective than many potential users believe. “They say they aren’t on the cloud, but instead use a corporate data center 300 miles away,” he says. “In my mind, what’s the difference? Latency, availability, uptime, security, all those things have been taken care of. It’s not rocket science; it’s not the future. It’s today.”

The question for MES companies, Franzosa says, is whether they have the resources to make their products cloud ready. Small and large companies will struggle with this, he says, and currently only about a dozen MES suppliers have more than 10% or of their install base running in the cloud.

Article Topics

Special Reports News & Resources

Automation/Retail Special Issue: Savvy users embrace change Research Report: Use of Automation in Warehouse/DC Special Digital Issue: Warehouse/DC Robotics System Report: Building the world’s best warehouse Top 20 Warehouses 2019 Top 20 automatic identification and data capture suppliers 2019 Top 20 Lift Truck Suppliers in 2019: Market reaches new heights More Special ReportsLatest in Materials Handling

Materials Handling Robotics: The new world of heterogeneous robotic integration Lucas Watson appointed CSO for Körber’s Parcel Logistics business in North America Hyster recognizes Dealers of Distinction for 2023 Carolina Handling names Joe Perkins as COO C-suite Interview with Keith Moore, CEO, AutoScheduler.AI: MODEX was a meeting place for innovation Walmart deploying autonomous lift trucks at four of its high-tech DCs Coles shops big for automation More Materials HandlingAbout the Author

Subscribe to Materials Handling Magazine

Find out what the world's most innovative companies are doing to improve productivity in their plants and distribution centers.

Start your FREE subscription today.

April 2024 Modern Materials Handling

Latest Resources