Warehouse/DC Management: Smarter funding for the future

Though often characterized by feast or famine, this year’s view into warehouse and distribution spending plans instead strengthens a pattern of deliberate investment. Today, readers are determined to get the most out of every dollar spent.

Latest Material Handling News

When an operation needs an infusion of capital in order to improve, a “Band-Aid” solution is often a shortsighted way to waste what little money is available. On the other hand, a massive project can feel like a “Hail Mary” attempt to make the most of resources that will probably not come around again for several years.

The results of Peerless Research Group’s (PRG) 2015 State of Warehouse/DC Equipment Survey suggest the industry has tired of both paths. Instead, readers tell us that they prefer the middle ground and are steadily investing in targeted solutions that position them for efficiency, productivity, and growth.

According to Norm Saenz Jr., managing director of St. Onge Company, a consulting firm specializing in implementing solutions in warehouse and distribution operations, the survey results indicate that companies are growing smarter about getting the most out of every dollar spent. “Many of our clients are also looking to invest in the right level of technology to support steadily increasing volumes,” he says. “The low-hanging fruit has been cut by many warehouse managers, and the next step is to make smart investments.”

About 60 percent of readers have less than $250,000 to spend, but a full 25 percent have more than $1 million, which Saenz says can enable major changes. Nearly the same amount of readers plan to take their business to a new supplier, and Judd Aschenbrand, director of research for PRG, says that means a lot of opportunity.

“It’s a good sign for the vendor community, but it’s also a good sign for the end-users who are making it clear that they either need more suppliers and solutions or aren’t satisfied with what they have,” Aschenbrand says. “There are more shifts in this survey than in previous years. Still, the results show that this is a deliberate industry that doesn’t make knee-jerk decisions.”

The yellow light turns green

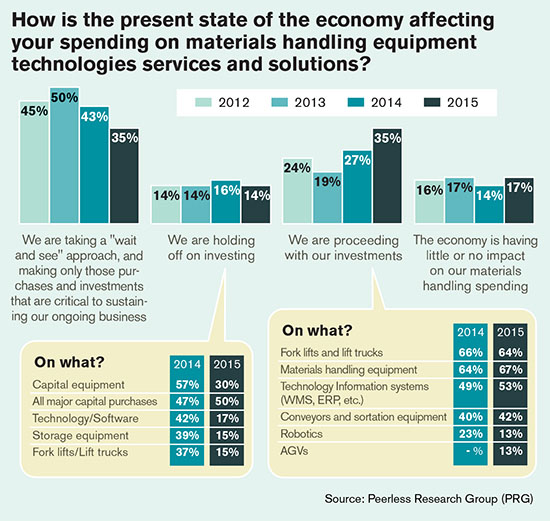

Throughout the history of this survey, the “wait and see” approach has been the most popular one by a large margin. This year, the number of hesitant readers sharply dipped from 43 percent to 35 percent, the second 8 percent drop in a row. It now ties the number who are ready to proceed with investments, which shot to 35 percent from 27 percent in 2014 and 19 percent in 2013.

The survey captures both actual spend on materials handling equipment in the previous year and anticipated spend in the coming one to three years. Readers’ projections tend to be accurate, if a bit conservative, and this year’s forecast suggests more of the same in 2015.

Although more are ready to spend, the average amount has held flat at about $345,550 for three years. However, Aschenbrand notes that in the same time period the median spend has jumped nearly $14,000, indicating more companies moving into higher spending levels.

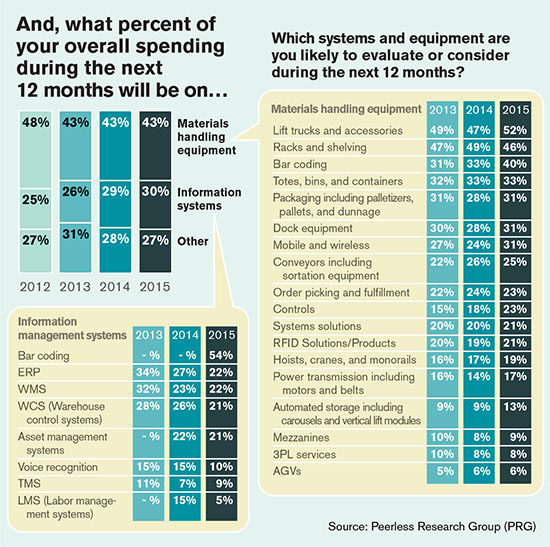

In the next 12 months, 43 percent of total planned spending will go toward materials handling equipment. Of that amount, readers are looking to buy lift trucks and accessories (52 percent), racks and shelving (46 percent), and totes, bins and containers (33 percent). Both bar coding (40 percent) and mobile and wireless solutions (31 percent) saw significant spikes in reader interest from previous years.

The trend is reflected in new survey questions this year designed to capture readers’ current and future usage of mobile technologies. More than half (57 percent) are using or have plans to use mobile solutions, which are used by more employees (40 percent) in more locations (15 percent)—including outside the four walls (19 percent).

Barcode scanners (65 percent) and labels (56 percent) top the list of devices or technologies either currently in use or planned for the coming year, as well as smart phones or tablets (62 percent), RFID readers (25 percent) and tags (22 percent), and voice technology (13 percent). “Mobile technology is certainly an emerging phenomenon in the warehouse,” Saenz says, “and five years ago it wouldn’t have shown up on a survey. This will increase every year going forward.”

Planned spending on information technology suggests many businesses have already modernized their platforms and will now focus on execution in 2015. When asked whether any recent purchases were firsts or constituted a substantial change in historical practices, 40 percent pointed to their new information technology systems. About a third said recent investments in materials handling equipment had contributed to their new course, and another third said purchases hadn’t had much impact on processes.

As readers settle into their new IT systems, the survey highlights an elevated equipment spend and a nearly universal dip in anticipated spend for IT systems. Interest in labor management systems (LMS), which debuted on the survey last year at 15 percent, fell to 5 percent. Because LMS modules are now found in all tiers of warehouse management systems (WMS), and since a number of other new solutions can boost labor visibility, a shifting market could account for the data dip. Elsewhere, the survey clearly illustrates a strong focus on labor management, safety, and productivity.

Best practices and their outcomes

Safety again topped the list of readers’ current pressing issues, with 89 percent of readers ranking it as very important. When asked which issues will become even more important in the next two years, respondents predicted increased emphasis on training (65 percent), labor availability (57 percent), and ergonomics (52 percent).

“Every distribution center needs quality people to run efficiently,” Saenz says. “With a growing amount of technology used in the traditional warehouse, finding and keeping the best people is fundamental to the success of the operation.”

Among manufacturing operations, labor productivity again scored high, but was leapfrogged this year by lean manufacturing. With 57 percent of readers currently focused on lean and nearly two thirds expecting the trend to grow in the next two years, the only topic with a faster anticipated rate of growth is just-in-sequence production. Distinct from just-in-time (42 percent now, 45 percent in two years), just-in-sequence is now an issue for 29 percent of readers, and 38 percent see added pressure coming.

Among warehousing and distribution operations, labor productivity is still toward the top of the list (59 percent now, 65 percent in two years), but efforts to lean inventories are also primed for growth (50 percent now, 58 percent in two years).

“It’s not surprising to see a push into measuring performance and lean principals over the next two years,” says Saenz. “It seems more surprising that it’s less important right now. Tracking and measuring performance is the sure way to discover productivity-increasing opportunities.” He also notes that reader interest in outsourcing, which concerns one in 10 readers now, could become a focus for one in five in coming years.

This year’s survey included a new question geared specifically toward capturing reader interest in outsourcing the maintenance of their automated materials handling systems. Slightly more than half maintain such equipment in-house, and only 12 percent exclusively outsource. Another 35 percent employ a mix of the two. According to readers, vendors and maintenance suppliers are chiefly focused on maintenance (49 percent), upkeep/upgrades (46 percent), consulting (43 percent), and data analysis (17 percent).

Saenz suggests that more and more companies might be looking to in-source materials handling equipment maintenance since it can be less costly. “But that means full-time staff, certain facilities, and technical know-how,” he says. “If it is only lift trucks, it could be managed in-house, but if the system includes conveyors, sorters, automated storage and retrieval systems, it might be safer for some to outsource.”

2015 Survey Supplement: Automation and robotics

In addition to concerns and interest in available solutions, this year’s survey sought to identify those areas where robotics and automatic guided vehicles (AGV) have already penetrated materials handling applications.

According to results, one in 10 readers currently uses an AGV for tasks including transportation (41 percent), storage (38 percent), bin picking (23 percent), truck loading (20 percent) and unloading (14 percent), and order fulfillment (20 percent). About 18 percent use robotics for functions like palletizing (42 percent), pick and place or part transfer (36 percent), packing/packaging (36 percent), depalletizing (19 percent), and unpacking (12 percent).

In each of these applications, AGVs and robots must justify themselves, Saenz says, and there are many semi-automated solutions that might provide the required throughput at a much lower investment than a fully automated one. “Automation can also be a less flexible solution,” he says, “and with uncertainly still in the air, companies are looking to make smart investments that keep their options open.”

2015 Survey Supplement: E-commerce and fulfillment

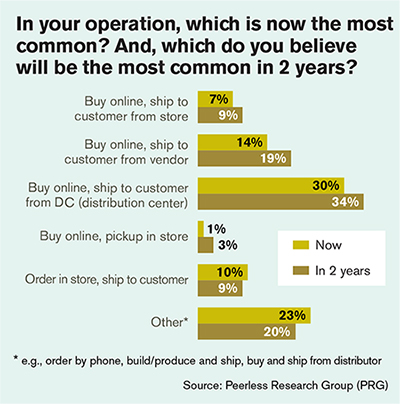

In an effort to illustrate the impact of the e-commerce revolution on equipment purchases, this year’s survey asked which capabilities are now most common and which might be two years from now.

Three in 10 currently support “buy online, ship to customer from DC,” and 34 percent expect it will be common in two years. Readers expect fewer consumers will care to buy in the store and then make a second trip for pickup.

Although 15 percent of companies now offer such services, only 6 percent expect it to continue in the future. “Order in store, ship to customer,” is in practice among 10 percent of respondents, but could also fall somewhat in coming years, according to Saenz.

Those capabilities expected to grow include “buy online, ship from vendor” (14 percent to 19 percent), “buy online, ship from store” (7 percent to 9 percent) and “buy online, pickup in store” (1 percent to 3 percent).

All of these omni-channel pathways also impact where functions are performed. When asked whether a company’s e-commerce activity has prompted or will prompt changes, readers indicated e-commerce has led them to perform distribution functions in a manufacturing environment (46 percent) and perform manufacturing functions in a distribution environment (36 percent).

Packaging and fulfillment might occur at the point of manufacture (47 percent), warehouse (39 percent), DC (22 percent), fulfillment center (11 percent), retail store (4 percent), or is outsourced (3 percent).

Saenz says that he’s surprised to hear many manufacturers would perform e-commerce distribution in their plants. “The large manufacturing companies that I’ve worked with are fulfilling e-commerce either using a 3PL, a separately operated facility, or within an existing distribution center,” he says. “I am less surprised that many distribution centers are required to perform some assembly and or manufacturing to finalize an e-commerce request.”

Article Topics

Magazine Archive News & Resources

Latest in Materials Handling

Registration open for Pack Expo International 2024 Walmart chooses Swisslog AS/RS and software for third milk processing facility NetLogistik partners with Vuzix subsidiary Moviynt to offer mobility solutions for warehouses Materials Handling Robotics: The new world of heterogeneous robotic integration BSLBATT is looking for new distributors and resellers worldwide Lucas Watson appointed CSO for Körber’s Parcel Logistics business in North America Hyster recognizes Dealers of Distinction for 2023 More Materials HandlingAbout the Author

Subscribe to Materials Handling Magazine

Find out what the world's most innovative companies are doing to improve productivity in their plants and distribution centers.

Start your FREE subscription today.

April 2024 Modern Materials Handling

Latest Resources