2014 Software Survey: Software marches firmly onward

Modern readers weigh in on their usage of supply chain software, its value to their organizations, and their spending plans for expanding, updating and growing.

Amid sweeping change throughout the supply chain, nimbleness has become the primary weapon with which to combat uncertainty. This change has prompted some to invest heavily in big software projects intended to replace the habits of the past century with the foundations for the future. Others have invested incrementally, taking advantage of solutions’ scalability to target and solve each problem in turn. As a result, software applications have evolved from monolithic to adaptable, a transition reflected in spending and adoption patterns.

This is one of the many trends outlined in Modern’s 2014 Software Usage Survey, conducted in March 2014. To better understand how readers use supply chain software to optimize their warehouse and distribution operations, Peerless Research Group (PRG) recently surveyed subscribers of Modern as well as a sample of recipients of our e-newsletters. Judd Aschenbrand, director of research for PRG, notes a clear upward trend in the adoption of 21st century software, automation and technology. See last year’s survey.

“These operations face a range of issues and challenges, from automation, cycle times and tracking to systems implementations,” Aschenbrand says. “Managers have one headache after another and are increasingly driven to deploy technology for problem solving.”

John Hill, director for supply chain consulting firm St. Onge, adds that “Aleve, Advil and aspirin might help with those headaches, but it’s software that can directly affect the synchronized flow of materials and related information to strengthen supply chain performance and provide managers the relief they are seeking. This report answers the questions: which software, for what applications, and in what sequence?”

Deliberate spending plans

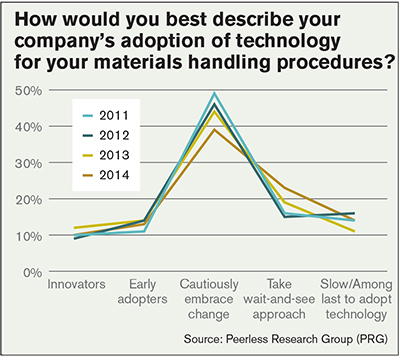

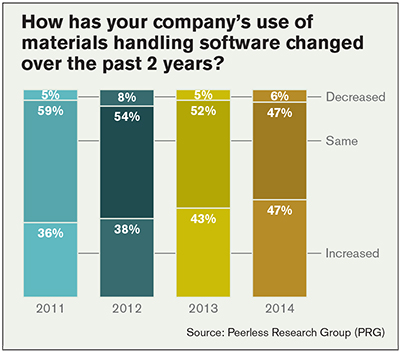

The survey reflects the plans and perspectives of 134 qualified respondents. As with last year’s survey, roughly a quarter of respondents consider themselves innovators or early adopters of warehousing and distribution technology, one in seven are slow or among the last to adopt and 62% cautiously embrace change or take a wait-and-see approach with an eye toward second-generation technology. In total, the field is now split cleanly down the middle: Half of respondents state that their use of warehouse and distribution software increased in the past two years, and half say that their usage stayed the same.

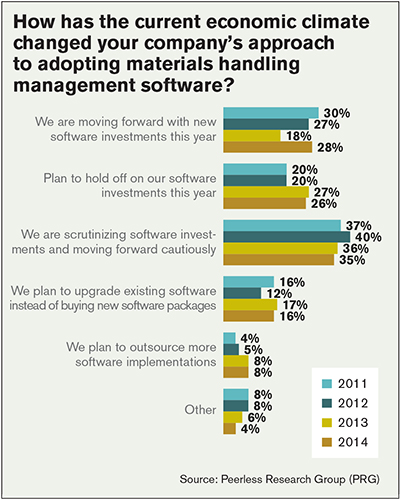

When asked how the current economic climate is affecting readers’ approaches to software adoption, the 2013 and 2014 breakdowns are virtually unchanged; readers are moving forward with software investments this year (21.1%), holding off this year (25.6%), moving forward cautiously (35.3%) and upgrading existing software instead of buying new (16.5%). About 8% of those are making an investment plan to outsource software implementations.

Aschenbrand says the number of respondents holding off seems high given the apparent benefits of modern software, but he suggests these organizations are not simply waiting. “The solutions they need are on their radar,” he says, “and many are making preparations to move forward when the time is right.”

According to Hill, “The time will be right when the prospective user has carefully crafted the value proposition and prepared a fact-based investment proposal that resonates with senior management.”

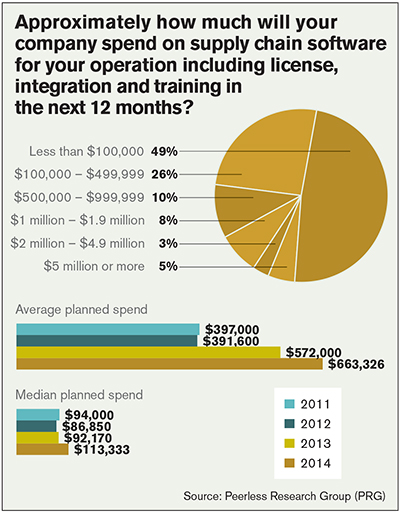

For those prepared for an outlay, half expect to spend less than $100,000 in the next year, a quarter will spend between $100,000 and $500,000 and nearly 8% foresee supply chain software spending of more than $2 million. This year’s average spending is $663,000—a sizable jump from last year’s $572,000 average and well above the roughly $400,000 reflected in both the 2012 and 2011 surveys.

The makeup of each survey base can differ dramatically from year to year, but it’s possible to compare the amount of spending as it relates to the size of the business. This year, a quarter of respondents bring in less than $10 million per year, another quarter between $10 million and $50 million, and about 17% are above the $1 billion mark.

The median annual revenue for 2014 is $81.8 million, up from $70 million in 2013 and $42.8 million in 2012. When analyzed next to median spending in recent years (2014 had $113,000; 2013 had $92,170; 2012 had $86,850) the revenue/outlay ratios indicate software spending was a priority in 2012 (2:1), fell somewhat in 2013 (1.3:1), and is now back on the rise (1.4:1).

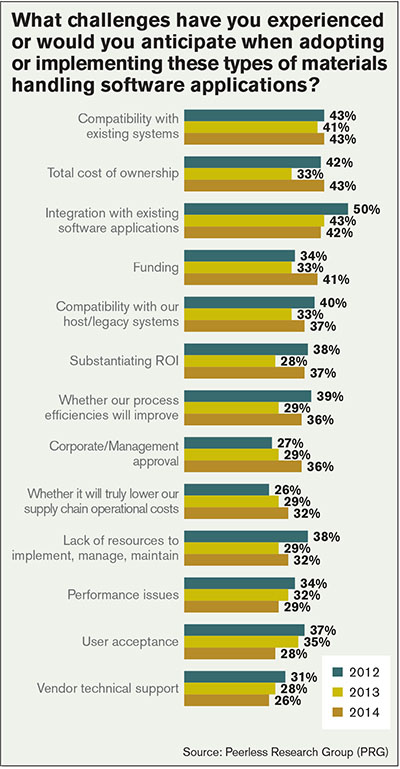

Challenges

This year’s survey asked readers about the challenges they have experienced or might anticipate when adopting or implementing warehousing and distribution software applications. Concerns over a new system’s ability to integrate with existing systems have held at the lowest levels in recent years of the survey (about 42%). Total cost of ownership (43%), funding (40%), substantiating an ROI (37%), corporate approval (36%) and user acceptance (28%) continue to rank high on the list.

In the last two years, respondents have sought to overcome an assortment of problems by implementing a software application in their warehouse or distribution operations. Omni-channel distribution, labor reductions, space utilization, inventory tracking and cycle time reduction top the list. Improvements to automation such as automated storage and retrieval, bar coding and scanning and conveyor controls are also top of mind. Some still struggle to finalize their enterprise resource planning (ERP) or warehouse management system (WMS) implementations, while others cite general problems with computer and data integration technologies.

When asked which software solution or application they would immediately implement if they could, respondents overwhelmingly said a WMS. Other favorites included automated picking, paperless warehouse, RFID, slotting software and voice picking solutions.

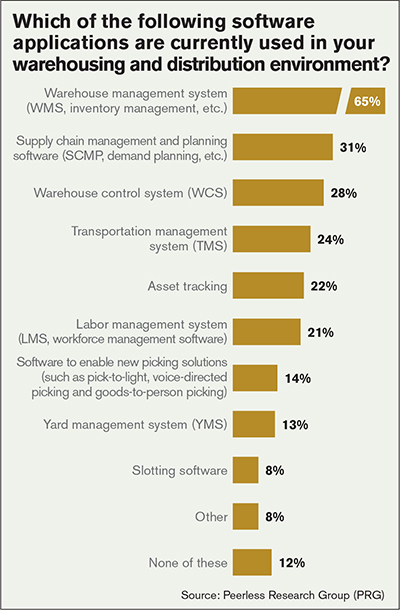

Usage of software applications

Readers already using supply chain management software identified the seven most important objectives: inventory visibility (72%); demand planning (67%); order management (64%); procurement (58%); vendor/supplier collaboration (50%); manufacturing (39%); and event management (17%). These are the same initiatives driving other respondents to evaluate expanded software usage, with nearly half of them pursuing improved inventory visibility or order management.

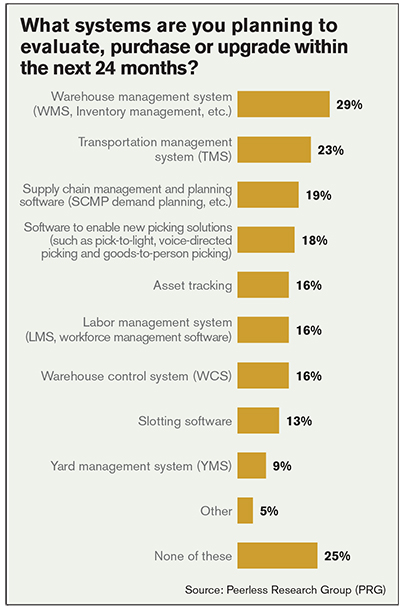

As in year’s past, the most commonly used software application is WMS followed by supply chain management and planning software (SCMP). Roughly two out of three respondents are currently using a WMS, a slight increase since 2011 when 60% reported using a WMS, while 31% report using planning solutions. As a foundational solution, WMS is increasingly sharing turf with warehouse control systems (WCS), which are in use in 28% of respondents’ facilities, second only to WMS and SCMP. More than 20 respondents plan to evaluate or purchase each of the following in the next two years: WCS, asset tracking and labor management systems (LMS).

A fifth of all respondents are using labor management software, and another fifth plan to evaluate LMS in the next two years. The adoption of engineered labor standards has ticked upward among this year’s surveyed group, with 40% now running ELS, a quarter planning to, and 36% expressing no interest. At the same time, the number of respondents using or considering a program to tie employee payment to productivity improvements has fallen sharply from a roughly 50/50 split in last year’s survey. Now just 15% are using, or will use, incentive programs.

Respondent demographics

Modern’s annual Software Usage Survey collected responses from 134 qualified individuals. To qualify, respondents must be personally involved in using, evaluating or purchasing software for their company’s materials handling operations.

This year’s respondents reflect management at all levels. Upper level management, meaning vice presidents, general managers and division managers, account for 36%, while 45% are responsible for managing their company’s logistics distribution, warehouse, supply chain, operations or purchasing functions across both manufacturing and non-manufacturing vertical industries.

In terms of vertical markets served, respondents indicated their businesses were food and beverage (14.1%), automotive and transportation (6.6%), computers and electronics (5%) and industrial machinery (3.3%). On the non-manufacturing side, wholesale trade (12.4%), third-party logistics providers (5%), transportation/warehousing services (4.1%) and retail trade (3.3%) were among the respondents.

While 16.7% of the companies report annual revenue of more than $1 billion, 26% are small businesses that report less than $10 million annually. The median revenue for 2014 is $81.8 million, up from $70 million in 2013 and $42.8 million in 2012. As the number slides upward it represents more responses from medium- and large-sized companies.

New questions

The 2014 survey included a few new lines of inquiry in an effort to capture additional perspective on the factors influencing software adoption.

Thinking about your current level of automated materials handling, has the growth in e-commerce orders or other customer requirements caused you to evaluate or implement new automated materials handling systems for picking, packing and shipping processes?

Yes: 42% No: 58%Are/will those processes be directed by the WMS or are/will they be directed by a WCS or similar order fulfillment software application?

WMS: 43% WCS: 51% Other: 6%Are you considering the fulfillment of some of those orders from your retail store in addition to a distribution center?

Yes: 46% No: 54%Are/will those processes be directed by paper-based picking methods?

Yes: 56% No: 44%

Article Topics

Special Reports News & Resources

Automation/Retail Special Issue: Savvy users embrace change Research Report: Use of Automation in Warehouse/DC Special Digital Issue: Warehouse/DC Robotics System Report: Building the world’s best warehouse Top 20 Warehouses 2019 Top 20 automatic identification and data capture suppliers 2019 Top 20 Lift Truck Suppliers in 2019: Market reaches new heights More Special ReportsLatest in Materials Handling

The (Not So) Secret Weapons: How Key Cabinets and Asset Management Lockers Are Changing Supply Chain Operations MODEX C-Suite Interview with Harold Vanasse: The perfect blend of automation and sustainability Consultant and industry leader John M. Hill passes on at age 86 Registration open for Pack Expo International 2024 Walmart chooses Swisslog AS/RS and software for third milk processing facility NetLogistik partners with Vuzix subsidiary Moviynt to offer mobility solutions for warehouses Materials Handling Robotics: The new world of heterogeneous robotic integration More Materials HandlingAbout the Author

Subscribe to Materials Handling Magazine

Find out what the world's most innovative companies are doing to improve productivity in their plants and distribution centers.

Start your FREE subscription today.

April 2024 Modern Materials Handling

Latest Resources