2016 Top 20 Automatic Data Capture Suppliers

Suppliers and users of scanners, printers and rugged mobile devices find themselves at the intersection of technological advances, increasing consumer demands and rising labor costs. The top players are finding ways to meet each challenge with minimal risk as the market landscape continues to shift.

Latest Material Handling News

NetLogistik partners with Vuzix subsidiary Moviynt to offer mobility solutions for warehouses AI-based inventory monitoring solution provider Gather AI raises $17 million ProGlove and topsystem partner on hands-free picking solution JLT Mobile Computers launches warehouse productivity software Zebra Technologies introduces wearable computers More Data Capture

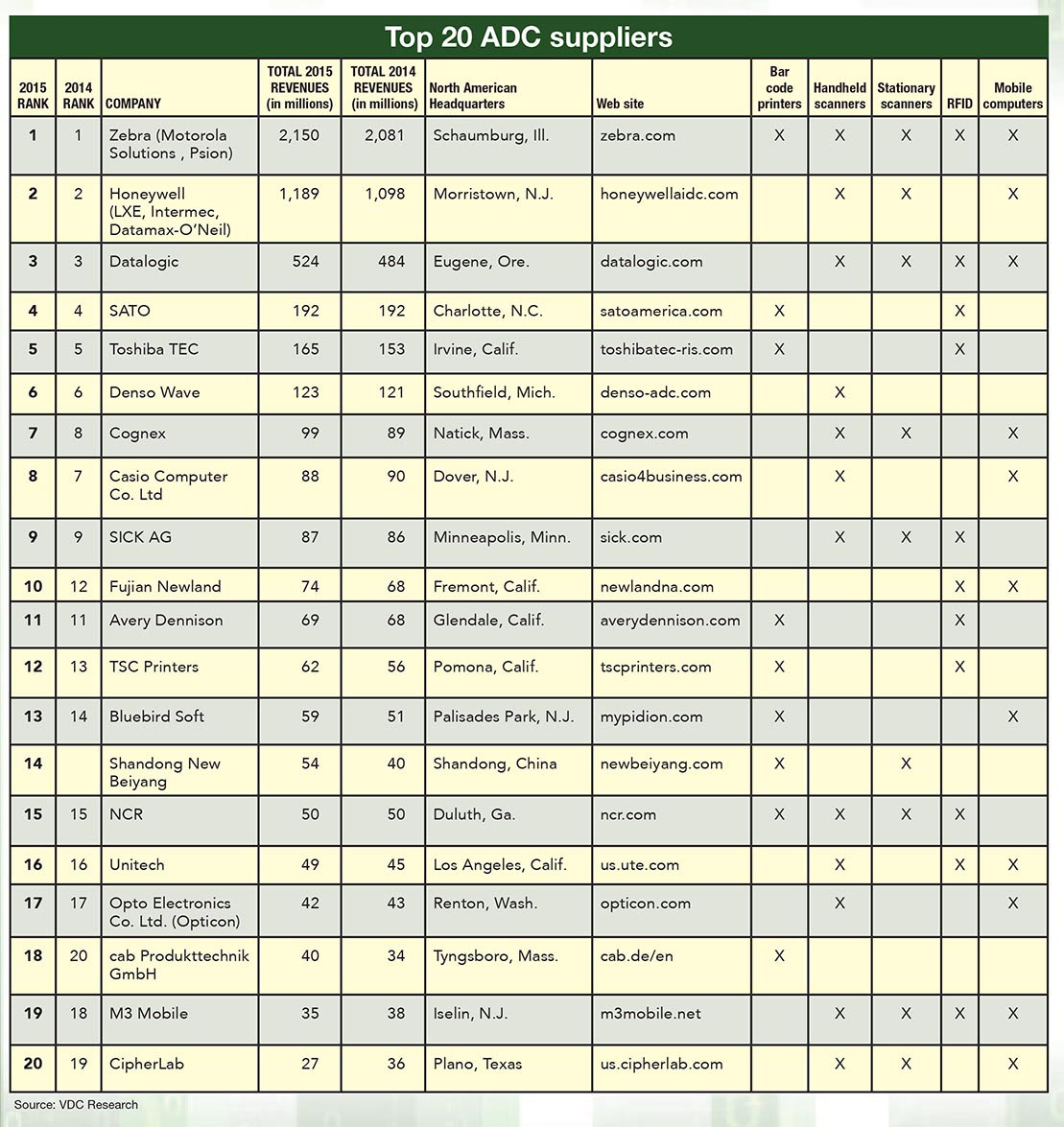

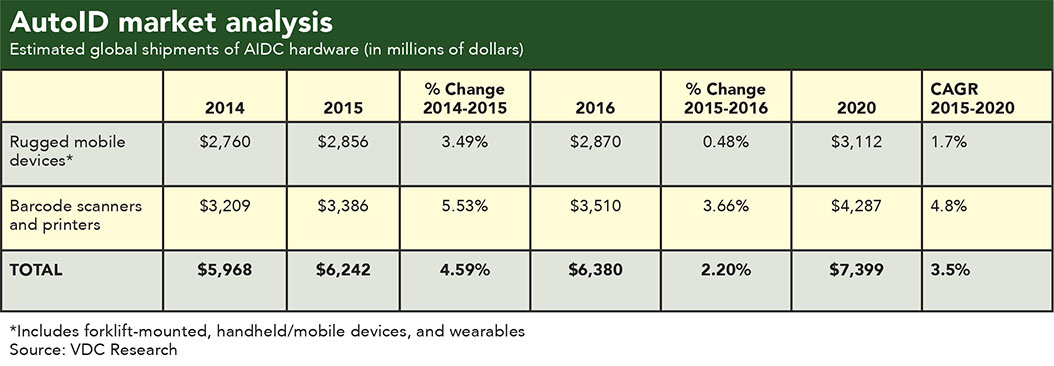

Last year, the global market for automatic data capture solutions (ADC) used in factories, warehouses and logistics applications reached $6.242 billion in sales, according to Massachusetts-based VDC Research Group. Global figures, each ADC market segment and 14 of the Top 20 suppliers reported gains over last year, when dramatic fluctuations in currency exchange rates adversely impacted many of the reported revenues.

Still, the market in 2014 enjoyed a banner year that analysts did not expect to be replicated in 2015, according to Richa Gupta, senior analyst for AutoID and data capture at VDC Research. Following double-digit growth in the previous year, the combined revenues of the Top 20 still grew by another 2.6% in 2015.

The ADC market includes handheld and stationary bar code scanning and imaging devices, bar code printers and ruggedized mobile computing solutions for factories and warehouses. VDC’s figures do not include consumables associated with automatic data collection, such as bar code labels.

The 2015 global sales figures represent an increase of 4.6% from 2014’s comparable estimate of $5.9 billion, which had grown 3.8% from 2013. VDC data projects the market will post a compound annual growth rate (CAGR) of 3.5% through the next five years before reaching $7.4 billion in 2020. This includes a 4.8% CAGR for bar code scanners and printers, and a 1.7% CAGR for rugged mobile devices.

“Growth was on the slower side, but 2015 was still a strong year from an AIDC perspective,” Gupta says. “A lot of that was driven by larger vendors, and there continues to be intense competition from Asian manufacturers, particularly in China and Taiwan. Given that AIDC market drivers are tied to broader supply chain and data capture trends, we don’t expect any significant slowdown.”

Notable performances

Zebra again ranks No. 1 by a comfortable margin after its 2014 acquisition of Motorola Solutions’ enterprise business. Second-place Honeywell reported 8.3% growth following its acquisition of Datamax-O’Neil in early 2015.

“Now Honeywell is working to ensure all its brands on the printing or scanning side are communicating with a similar vision in terms of what products are used for, following Honeywell’s policy that a single message be communicated by products under each portfolio,” Gupta says. “They launched new Honeywell printer models, which was a shift in how they previously approached the market when leveraging the Intermec and Datamax brands. They’re now trying to unify under the Honeywell brand.”

In terms of printers, Gupta says Datamax continues to be a relatively strong competitor to Zebra, which is dominant in the space. Datamax owns significant market share in the Americas and India, she says, while the Japanese market is dominated by 4th-place Sato and 5th-place Toshiba TEC. In mainland China, 12th-place TSC and Top 20 newcomer Shandong (No. 14) are prominent players. One of the only noteworthy acquisitions in the scanning and printing space, Gupta says, was Taiwanese TSC’s acquisition of Printronix, whose bar code printer revenues have ranked it just outside the Top 20 in recent years.

Cognex’s 11.2% growth to $99 million was enough for it to leapfrog Casio Computer to claim 7th place, and Fujian’s 8.8% growth gained it two spots to finish No. 10. Shandong (35%), cab Produkttechnik GmbH (17.6%) and Bluebird Soft (15.7%) posted the highest rates of growth in 2015, and CipherLab (-25%), M3Mobile (-7.9%), Opto Electronics (-2.3%) and Casio Computer (-2.2%) reported lower revenues. SATO and NCR held level at $192 million and $50 million respectively.

Navigating operating systems

David Krebs, vice president of VDC’s enterprise mobility and connected devices, says the big story in the rugged handheld market is consolidation. Although there have not been any big deals among the Top 20, Krebs cites Honeywell’s acquisition of Intelligrated and its attempt to acquire JDA Software as evidence of the trend.

“The other big theme is about operating systems and to what extent Android is wedging itself into the market,” Krebs says. “We estimated Android share to have reached just more than 20% in the first half of the year, and Zebra is the clear beneficiary of this based on the investments they’ve made. While most vendors have Android solutions and products in their portfolios, Zebra has taken a leadership position there, which was important given the lack of direction from Microsoft.”

Microsoft was rumored to release a new mobile operating system for several years before the announcement of its Windows 10 IoT (Internet of Things)mobile enterprise product. “It will be interesting to see how they are received,” Krebs says, “since the platform has a lot of question marks. Android does, too, but Windows is probably about two years behind Android as a platform for rugged mobile applications.”

Specifically in the warehouse materials handling environment, Krebs says there is still pent-up demand for a Windows-based mobile solution. The technology adoption dynamic inside the warehouse is very different than outside applications like retail or field service, logistics and delivery.

“The warehouse tends not to do wholesale upgrades, and instead prefers to hold onto its install base as long as possible,” he says. “We’ve seen terminal emulation continue to have an almost impenetrable hold and, because it is the dominant approach, Windows CE has been resilient. That said, Android is still an emerging opportunity as opposed to something that has reached critical mass. There haven’t been any Android-based, warehouse-specific solutions or vehicle-mounted solutions, so there are still gaps in the portfolio.”

VDC recently conducted a survey among warehouse decision makers, Krebs says, including a telling question: “If you had the choice, would you rather upgrade rugged mobile devices more frequently or continue to use what you have?” A slight majority, 52%, wanted to replace more often.

“I don’t know if there is necessarily a good justification for that, since there tends to be only incremental device improvement; the difference between a device’s capabilities now and three years from now is not huge,” Krebs says. “However, warehousing is changing with technology, automation, robotics, the impact of e-commerce and item-level fulfillment, and the way products move through the supply chain. That is all suggestive of a demand for modernization, including migration from green screen, character-based systems to perhaps more touch-sensitive, intuitive, graphic mobile interfaces. This might portend a growing trend toward managing those devices in the warehouse in a similar way to what we see outside it.”

In terms of top drivers for mobile solution upgrades, the No. 1 factor is that the existing OS has reached the end of its life, Krebs says, and No. 2 is a desire to upgrade to a more modern interface. When evaluating solutions the primary concerns are security, business continuity, and the ability to customize applications. Android is particularly suited to easy customization, Krebs says, whereas the next-gen Windows mobile platform is being managed more as a consumer-style interface that is less customizable.

According to the VDC research, the central business pressures driving investment are familiar concerns. No. 1 is the consumer’s demand for faster delivery, No. 2 is the existing system’s ability to keep up with those orders, and lastly the high cost of labor.

Hardware trends

Sales continue to reflect a shift toward 2D scanning and imaging capabilities as the popularity of laser handheld scanners continues to decline.

“Vendors are really pushing the value proposition of imaging and helping customers migrate away from laser because of the additional capabilities imaging offers,” Gupta says. “In terms of mobile scanning, we’ve noticed the emergence of companion scanners to support the functionality of consumer-grade products that are winding their way into the enterprise environment. This is becoming a bigger discussion point.”

With a smaller form factor, connected typically by Bluetooth, companion devices like sleds and sleeves that attach a scanning engine to smart phones or tablets are in use as alternatives to industrial-grade rugged mobile computers. Consumer products don’t always have warranties or robust durability, Gupta says, but certain applications have several opportunities.

In the warehouse, Krebs also notes the continued penetration of imaging technology, particularly with regard to vision capture for dimensional applications. Perhaps more importantly, given that labor costs are among the largest expenses, Krebs says the analytics associated with labor are seeing greater attention.

“Training and onboarding of part-time and seasonal staff is a much more critical issue,” he says. “Customers are asking for solutions that are more intuitive and can reduce training time.”

Because warehouse applications also tend to be harsh environments for mobile devices, Krebs says there has not been as much adoption of consumer-grade solutions.

“We recommend—and see the majority of customers using—fully rugged devices,” he says. “We’re seeing consumer devices becoming more robust, with drop-proof or waterproof features, but they still are not ‘rugged’ by any stretch of the imagination.”

In the industrial rugged mobile handheld market, there is a clear downward trend in average sale price, which Krebs says has affected the overall market’s desire for “semi-rugged” devices, particularly in applications like healthcare and retail. These solutions have also contributed to the lower average sale price.

“It has been a tough year so far for rugged mobile,” Krebs says. “There was a large rollout with the United States Postal Service last year, which makes it difficult to compare year over year. But there is still is bit of a wait-and-see attitude, which will start to break up since we now know what operating system we’re getting from Microsoft.”

Going forward, wearable technology continues to be an important form factor and growing segment. Voice-directed solutions are also continuing to grow.

“We’re seeing some really interesting, although very much nascent, augmented reality (AR) technologies,” Krebs says. “Based on the demos I’ve seen, there’s a cool factor there, but I wonder if it’s really solving a problem that exists or just doing something cool. We have seen some larger logistics organizations, at least in labs, continuing to play with all sorts of ways to support workers and make them safer and more efficient.”

Collecting the data

Because this industry includes both public and private companies, this is the eighth year in a row that VDC Research Group compiled the data. They are covering this technology every day and are therefore very close to the market.

To make this list, companies must sell in North America, though the chart includes worldwide revenues. The list does not include resellers, systems integrators or other companies that do not manufacture ADC hardware. Because our readers are focused on supply chain solutions, we do not include companies whose primary focus is the retail checkout counter or non-industrial settings, like hospitals, libraries or resorts. Nor do we include companies that only manufacture consumables like bar code labels and RFID tags.

Article Topics

Data Capture News & Resources

NetLogistik partners with Vuzix subsidiary Moviynt to offer mobility solutions for warehouses AI-based inventory monitoring solution provider Gather AI raises $17 million ProGlove and topsystem partner on hands-free picking solution JLT Mobile Computers launches warehouse productivity software Zebra Technologies introduces wearable computers Peak Technologies exhibits machine vision solutions The reBound Podcast: Innovation in the 3PL supply chain More Data CaptureLatest in Materials Handling

Registration open for Pack Expo International 2024 Walmart chooses Swisslog AS/RS and software for third milk processing facility NetLogistik partners with Vuzix subsidiary Moviynt to offer mobility solutions for warehouses Materials Handling Robotics: The new world of heterogeneous robotic integration BSLBATT is looking for new distributors and resellers worldwide Lucas Watson appointed CSO for Körber’s Parcel Logistics business in North America Hyster recognizes Dealers of Distinction for 2023 More Materials HandlingAbout the Author

Subscribe to Materials Handling Magazine

Find out what the world's most innovative companies are doing to improve productivity in their plants and distribution centers.

Start your FREE subscription today.

April 2024 Modern Materials Handling

Latest Resources