27th Annual Masters of Logistics: Will new tools fix our old problems?

The current state of freight transportation has many of the same hallmarks as the past. And while shippers are assessing new technologies to better manage operations, the results of our “27th Annual Study on Trends and Issues in Logistics & Transportation” suggest that these new tools alone will not solve the age-old problems we’re still facing.

The economy’s check engine light is on.

Many companies were lulled into a sense of false well being as the domestic economy didn’t recover from the Great Recession of 2008 at the same pace as previous downturns. Adequate capacity was available early on and freight rates reflected the imbalance in supply vs. demand. However, the economy’s engine began overheating, warning of the issues in freight transportation management that we face today.

Now, companies across all industries are struggling to find the capacity they need while managing escalating costs. How did we get to this current state when the tools and technologies available have never been more powerful or readily accessible by logistics operations of all sizes? And how did we ignore the check engine light?

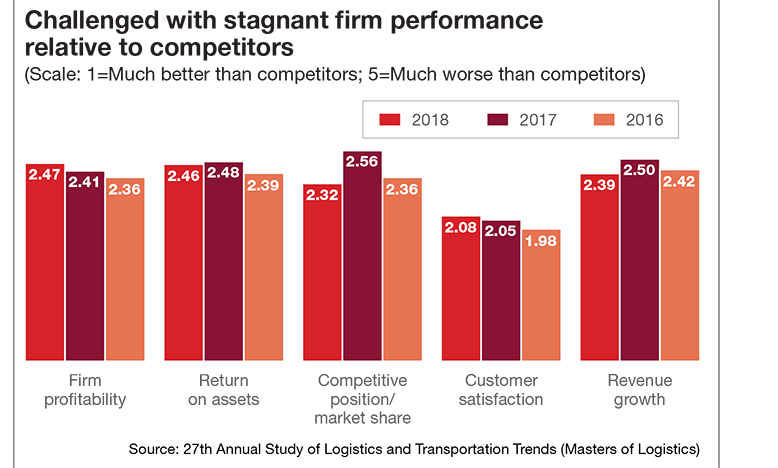

The signals of an approaching malfunction can be found in two key items that have been collected and analyzed in our “27th Annual Study of Logistics and Transportation Trends (Masters of Logistics).” The first indicator comprises five items—firm profitability, return on assets, market share/competitive position, customer satisfaction and customer growth—that provide an overall comparison of a company’s performance relative to its competitors.

The data presented below indicate that from a competitive standpoint, most companies reported that their performance has been somewhat stagnant over the three-year time period. However, in 2018, market share posted significant improvements with revenue growth reporting an impressive gain as well. The increase in these two areas year-over-year (YoY) was a signal of increasing demand for products and services.

What remained elusive was translating these improvements in company performance into profits, especially as compared to competitors. Profitability, along with customer satisfaction and return on assets, did not report appreciable improvement.

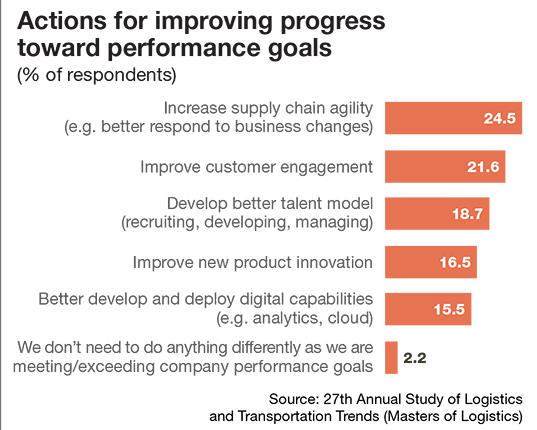

When asked what your company will do differently to improve performance, 24.5% of the participants in our annual study reported that increasing supply chain agility was at the top of their list. This action item was followed closely by improving customer engagement from 21.6% of respondents. Perhaps a reflection of the pressure to continuously improve in today’s business environment, only 2.2% reported that their companies did not need to do anything differently as they are meeting/exceeding performance goals.

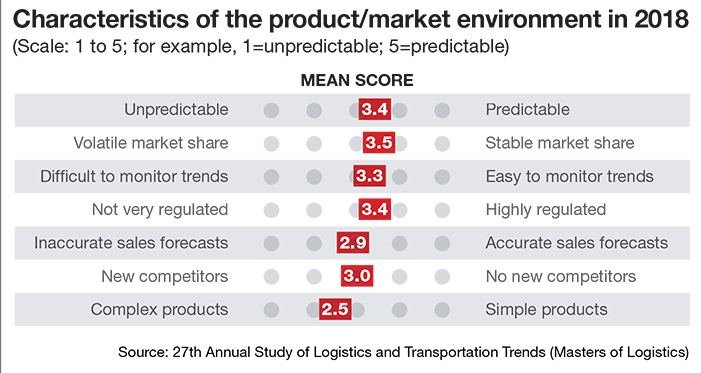

As experienced business managers know, the internal and external environments make an impact on firm performance. We asked participants in this year’s study to characterize several elements of their product market environment in order to gain some perspective on this facet. The 2018 results suggest that market elements tend to be more “unchanging” as compared to the product characteristic that is moving toward “complex.”

Where are companies heading?

The second indicator is the alignment of the strategy for the company, division or business unit, with the primary goals of the functional areas that support the business.

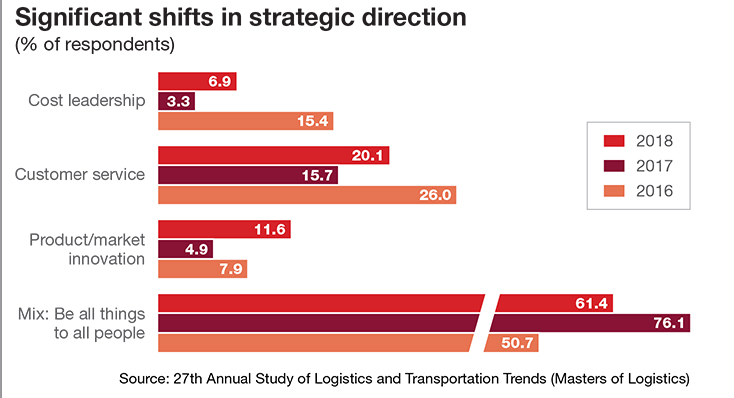

The last three years have posted the largest shifts in strategic direction since this study began 27 years ago. The dramatic changes firms have faced from 2016 to now can only be compared to those that happened from 2001 to 2003. As our survey found, the biggest decline since 2016 has been in the mix strategy—the “be all things to all people” approach to business.

We have long opined that this strategy is the most difficult to successfully deploy, particularly at the operational level where manager and associates often do not have the necessary tools or information.

Our analysis also revealed an interesting finding. When study participants were sorted into two groups—those that reported firm profitability better or much better than competitors compared to everyone else—our analysis indicated a significant difference in terms of strategic direction. More profitable firms frequently followed a customer service strategy. Companies in the second group more often pursued a mix strategy.

Many of us recall the significant shift in strategic direction that occurred after 9/11 resulting in immediate and long-term economic impacts. The tragedy contributed to a deepening recession, and, as a result, many companies pursued a cost leadership strategy. Thankfully, we have not experienced the magnitude of such an event during the most recent time period; hence, we were curious as to this swing in strategy, and its cause. What we found were yesterday’s problems being addressed and viewed in light of new tools to solve them.

Old, rusty supply chain problems

Solomon wrote that “there is nothing new under the sun,” and this year’s study validates his perspective. Today’s supply chain managers are grappling with problems their predecessors faced years ago. Time remains a critical service element, as companies seek to respond to customer requirements and expectations in hours, not days.

Firms are using supply chain capabilities in an attempt to build a long-term, sustainable advantage in the market. Visibility of the supply chain—in motion and at rest—is essential to firm performance, yet end-to-end supply chain visibility is not improving at a pace that’s needed to achieve this goal. And to a large extent, companies are still trying to determine how to structure their organizations to be more collaborative with suppliers, customers and transportation service providers. “Supply chain visibility is no longer a ‘nice to have’ for any organization, no matter the size, geography or industry. The best real-time visibility solutions available today offer vast data integration possibilities and complement the planning and executional capabilities of a TMS or ERP to create efficiencies, decrease transportation costs, and deliver a superior brand experience,” notes Tommy Barnes, President of project44, the sponsor of this year’s survey.

Firms are using supply chain capabilities in an attempt to build a long-term, sustainable advantage in the market. Visibility of the supply chain—in motion and at rest—is essential to firm performance, yet end-to-end supply chain visibility is not improving at a pace that’s needed to achieve this goal. And to a large extent, companies are still trying to determine how to structure their organizations to be more collaborative with suppliers, customers and transportation service providers. “Supply chain visibility is no longer a ‘nice to have’ for any organization, no matter the size, geography or industry. The best real-time visibility solutions available today offer vast data integration possibilities and complement the planning and executional capabilities of a TMS or ERP to create efficiencies, decrease transportation costs, and deliver a superior brand experience,” notes Tommy Barnes, President of project44, the sponsor of this year’s survey.

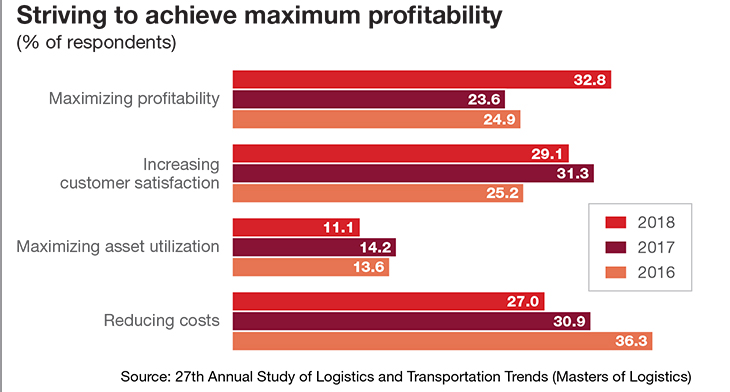

While companies have been altering their strategic path, they’ve also been making changes to objectives and goals that affect the priorities and management of logistics and transportation processes and activities. Our findings indicate that as a significant change, as more firms are focused on maximizing profitability. This increase was primarily realized through comparable shifts away from reducing costs and maximizing asset utilization.

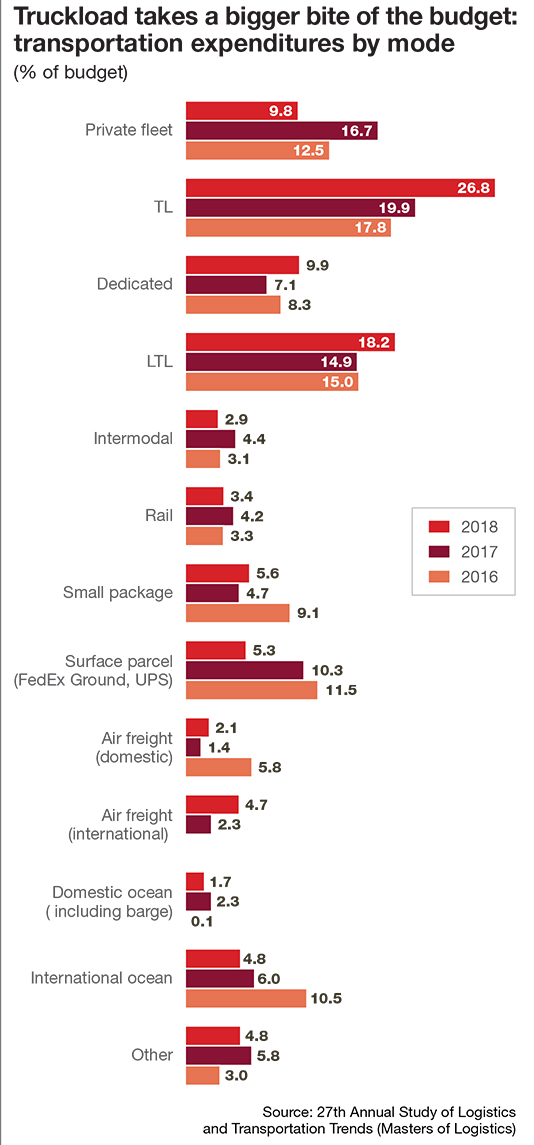

The issues and challenges faced by shippers and carriers are reflected in YoY changes in transportation expenditures by mode. Truckload expenditures are now commanding 26.8% of the transportation budget—this is approximately a 35% increase from 2017. Less-than-truckload (LTL) posted the second largest increase in expenditures YoY, representing 18.2% of the transportation budget.

Although LTL took a bigger bite out of the budget from 2017 to 2018, the increase in this mode was around 22% YoY. Overall, the cost to move freight is increasing at unprecedented levels. The study results show that 44.4% of companies are now spending more than 5% of sales on domestic transportation. In 2016, only 17.2% of companies reported this level of expense.

We also found that spending more didn’t necessarily result in better service. As expected, the turndown ratio increased dramatically for TL. Investment by LTL carriers to increase their network capacity contributed to fewer turndowns YoY, but it did not result in better on-time delivery. The percentage of damaged freight also increased for LTL from 2017 to 2018. It’s the same old problem that needs to be fixed—in today’s competitive business environment operational excellence is not an option.

Impact of supply chain digitalization

To complicate matters, the flashing check engine light is happening at a time when over 48% of companies view themselves as either leaders or early adopters in the supply chain digitalization transformation process.

Over 97% of this year’s respondents are paying attention to this developing area. This finding aligns with another finding from the annual study where participants posted the highest level of agreement on the statement: “Being a digital business is important to the success of my company.”

Over 97% of this year’s respondents are paying attention to this developing area. This finding aligns with another finding from the annual study where participants posted the highest level of agreement on the statement: “Being a digital business is important to the success of my company.”

What are the primary drivers leading the digital transformation? The findings from the annual study indicate they are to:

- build a long-term sustainable competitive advantage;

- improve the ability to respond to customer expectations; and

- reduce costs.

A deeper analysis offered some interesting insight: leaders in digital transformation were more often associated with customer-oriented strategies, while laggards tended to focus more frequently on cost leadership as their strategy.

More than half of the respondents reported that the planned level of investment by their company in digital business initiatives would be increasing or significantly increasing in the next 12 months to 18 months. However, it’s going to require a lot more than an increased investment to achieve a successful digital transformation. Only 22.3% of companies reported that digital initiatives are a core part of their company’s business strategy. The vast majority (55.4%) stated that digital initiatives are not a core part of the strategy and the business objectives for digitization were not always clear.

The role of shiny new tools

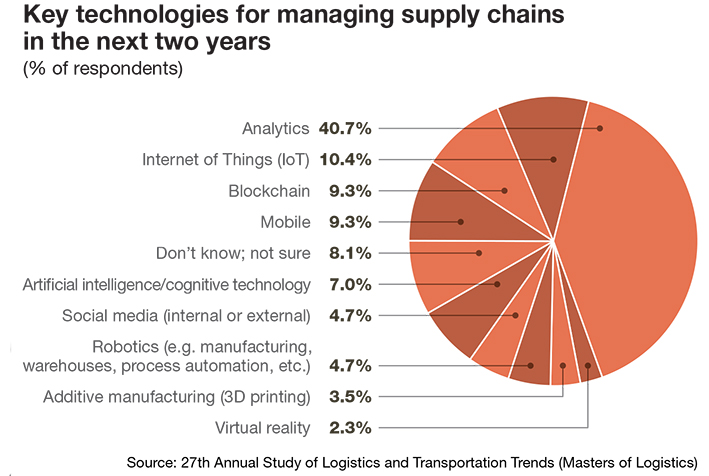

Using new tools with new approaches for managing transportation activities is crucial to improved company performance. In this year’s study we asked participants which technologies would be the most important to their company over the next two years. The results presented may surprise you.

While technologies like Blockchain, artificial intelligence, and additive manufacturing will no doubt have a significant impact on supply chain processes and activities, including transportation, the immediate need centers on analytics. This specific technology stands alone as the key priority for companies.

While technologies like Blockchain, artificial intelligence, and additive manufacturing will no doubt have a significant impact on supply chain processes and activities, including transportation, the immediate need centers on analytics. This specific technology stands alone as the key priority for companies.

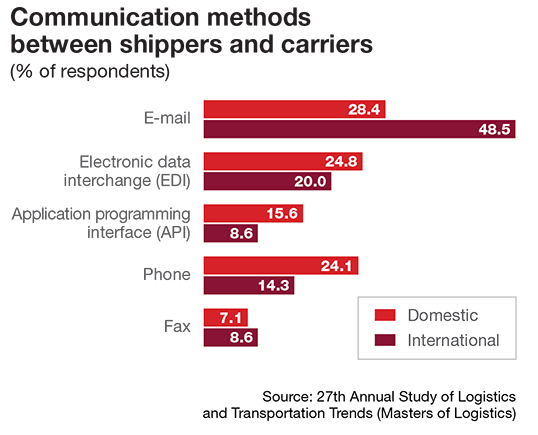

Results from this year’s study lead us to conclude that more sophisticated approaches are needed to communicate transportation activities with carriers. “Shippers need real-time transportation data to make effective decisions,” states T.J. Schaefer, Ph.D., head of strategic programs at project44, Inc., “and the only way to solve for this is through technology, especially one-to-many networks that effectively utilize APIs to connect shippers and carriers in real-time across all transportations modes and full shipment lifecycle from rate to tracking to invoice.” Even with the increasing use of APIs in transportation management systems to facilitate access and the real-time flow of data, the primary means of disseminating data can be characterized as “old school.”

Reliance on e-mail is problematic because it’s not a seamless link with other systems. It also depends on a correct distribution list, and the information/data contained in that communication often requires action by one or more of the recipients. Unless this information/data becomes part of a database, all parties lose meaningful data with which to do analysis—post hoc or as input to predictive analytics.

Changing the future state

The biggest barrier to solving supply chain problems, including transportation issues, is not a limited budget to acquire shiny new tools. Rather, the barriers are familiar ones that have been researched and talked about for several decades including:

- organizational structure is not collaborative;

- moving too slowly; cultural aversion to risk;

- lack of understanding of the technology’s impact;

- lack of strategic direction; and

- insufficient talent and training

The list above doesn’t necessarily require a large capital investment, but it does highlight a need to change. This change should follow three basic steps. First, firms need to define their strategic direction. What will they become in an ever-changing market? Second, they need to align resources to match their defined strategic direction. What role will technology play? What training do we need? What skill sets are critical to our success?

Finally, firms need to combine and collaborate with both suppliers and customers to manage risk, support innovation, and effectively and efficiently meet the needs of end consumers. As businessman Ray Kroc once noted: “None of us is as good as all of us.”

Finally, firms need to combine and collaborate with both suppliers and customers to manage risk, support innovation, and effectively and efficiently meet the needs of end consumers. As businessman Ray Kroc once noted: “None of us is as good as all of us.”

The economy’s check engine light is blinking and needs attention. It’s been on before, and we’ve solved the problem with the tools at hand by working on our individual firms. Yet, working individually will not get the efficiencies needed and expected in this speed-fueled economy.

Today’s tool kit is more complete and encompassing, able to diagnose and analyze the whole supply chain. The big question is whether or not we are willing to work together and really compete supply chain to supply chain.

Article Topics

Magazine Archive News & Resources

Latest in Materials Handling

Hyster recognizes Dealers of Distinction for 2023 Carolina Handling names Joe Perkins as COO C-suite Interview with Keith Moore, CEO, AutoScheduler.AI: MODEX was a meeting place for innovation Walmart deploying autonomous lift trucks at four of its high-tech DCs Coles shops big for automation Kathleen Phelps to join FORTNA as chief financial officer Coles automates grocery distribution in Australia More Materials HandlingSubscribe to Materials Handling Magazine

Find out what the world's most innovative companies are doing to improve productivity in their plants and distribution centers.

Start your FREE subscription today.

April 2024 Modern Materials Handling

Latest Resources