State of Global Logistics: Time for a reality check

A combination of rising global interest rates and ongoing trade protectionism will continue to create unexpected turbulence for logistics managers over the course of 2019, say analysts. Meanwhile emerging markets will provide opportunities for faster growth—yet each faces its own set of operational challenges.

Priorities for global logistics managers are likely to be subject to significant change in 2019, say industry experts and prominent economists. First and foremost, adapting pricing strategies to fit local market conditions will become more important than ever. At the same time, shippers will be tasked with building resilience into global operations to mitigate the impact of trade tensions, currency and debt shock. Finally, shippers must prepare for the eventual end of a robust—but unsustainable—business cycle.

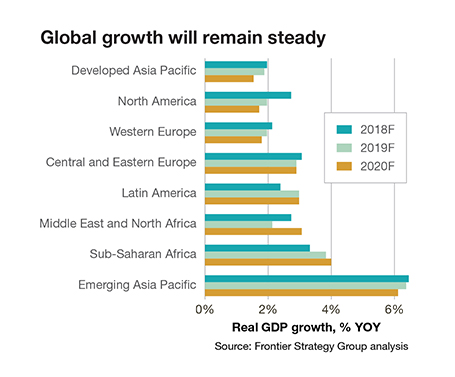

According to the Frontier Strategy Group (FSG), a Washington, D.C.-based consultancy advising Fortune 500 companies on trade opportunities and risk management, developed markets are transitioning out of a long economic recovery and into the expansionary phase. At the same time, the fates of emerging markets are tied to developed markets’ cycles.

“Emerging markets will see increased developed market demand for export products,” says Ryan Connelly, FSG’s senior analyst for global economics. “But as wages continue to increase in developed markets, the rate of return for new investments in low-wage, emerging markets will also ramp up.”

Pricing has become exceptionally complex, says Connelly, who notes that consumers remain price sensitive across much of the world and local competition is increasingly fierce. “But in some markets, high growth has led to an opportunity for each region to differentiate their advantages by offering premium logistical support.”

While most economies in Western Europe are recovering at a steady pace, those of the Middle East and North Africa, Latin America and the Commonwealth of Independent States appear to be less sustainable. China, says Connelly, is staging “a managed slowdown.”

Emerging markets will continue to recover, though China’s decelerating growth will limit significant upward movement. Developed-markets growth peaked in 2018, but will continue to expand in 2019 despite ongoing trade protectionism coming from the United States.

“Across 2019, this will take place in an environment of rising global interest rates, the emergence of inflationary pressure in developed markets and ongoing foreign exchange volatility,” Connelly concludes.

Inflation concerns

The most closely watched index for many logistics managers should be the one that measures global consumer inflation, say international trade experts. Nariman Behravesh, chief economist at IHS Markit, notes that this metric rose from 2% in 2015 to 3% in 2018.

“Most of this was due to a transition in the developed world from deflationary conditions to inflation rates that are close to central banks’ targets of 2%,” says Behravesh. “Over the near term, we expect to see global inflation and inflation in developed economies to remain close to 3% and 2%, respectively.”

While there will be upward pressures in many economies as output gaps close and unemployment rates fall, in some cases to multi-decade lows, there will be downward pressures as well, IHS Markit contends. “Outside the United States growth is weakening,” says Behravesh. “Moreover, relative to 2018, commodity prices will be relatively flat in 2019. Finally, with the trade war with China and the U.S. in a temporary truce, the upward push from tariff increases will be on hold.”

Meanwhile, growth in the emerging world has topped out, and will slide further. At 4.9%, emerging market growth in 2017 was the strongest since 2013. During 2018, growth among these countries has edged down to 4.8%. IHS Markit expects another decline in growth over 2019, to 4.6%.

“These averages hide a large divergence,” says Behravesh. “Some economies such as Brazil, India and Russia experienced a mild pickup in growth in 2018. Others such as Argentina, South Africa and Turkey came under intense financial pressure and suffered recessions or near-recessions.”

Countering headwinds

As logistics managers begin to consider sourcing and shipping alternatives this year, other economists are advising them to consider that the adverse effects of high inflation can fall disproportionately on the lowest wage nations.

According to Shanta Devarajan, chief economist and senior director for development at the World Bank, high inflation has been historically associated with slower economic growth, making efforts to maintain low and stable inflation crucial for reducing poverty and inequality.

“The adoption of a more resilient monetary exchange rate and fiscal policy framework among some emerging and developing economies has facilitated better control of inflation,” says Devarajan. “However, external factors that have held inflation at bay over the past decades may lose momentum or be rolled back.”

Franziska Ohnsorge, prospects group manager of development economics at the World Bank, advises a “nuanced” policy approach is necessary to mitigate the impact of global food price shocks on poverty without adverse side-effects.

“The use of certain trade policies to insulate domestic markets from food price shocks may compound the volatility of global prices,” says Ohnsorge. “Instead, storage policies and targeted safety net interventions can mitigate the negative impact of these shocks.”

Infrastructure issues

Jens Zimmerman, senior equity analyst for Credit Suisse, says global transport infrastructure concerns have been relegated to the back of line lately, but the need for upgrades and investments remains as pressing as ever.

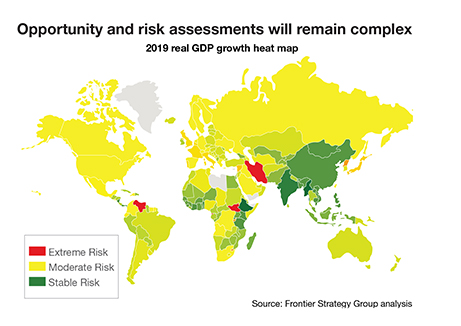

The global economic expansion masks significant divergence within and across regions. Rising global interest rates will create new issues for economies reliant on external financing. Logistics managers will need to carefully assess geopolitical, economic, and technological risks across their plans and portfolios.

“We see interesting new points of focus on the infrastructure issue,” says Zimmerman. “Namely, two continents often absent from outside investments—Africa, one of the most underinvested continents, and Latin America.” His firm’s recent report titled “The Global Infrastructure Outlook of the G20” forecasts that infrastructure investments in the global transport sector in those two continents offer the greatest potential by 2040.

This is particularly true for motor carrier transport. Investments in road infrastructure are expected to absorb 36% of the globally projected needs of $94 trillion. Adding rail, airports and ports to the pool means that over half of the sum will go to transport infrastructure.

“Unsurprisingly, the G20 infrastructure outlook report also projects the largest investment gap in the transport sector through 2040,” says Zimmerman. He also notes that of the total 15 trillion funding gap, a little more than two-thirds (69%) is expected to occur in the transport infrastructure sector, with road transport accounting for over half of the total funding gap by 2040.

“While much focus has been on the One Belt One Road initiative to interconnect infrastructure of overland corridors and shipping lanes between China and Eurasian countries, we believe that Africa and Latin America are interesting regional highlights,” says Zimmerman.

According to the report, the African Development Bank expects annual investment costs for road, ports, railways and air transport of $35 billion to $47 billion by 2025. Of these investments, 80% is required to preserve existing infrastructure and 20% to develop new projects. In Latin America, more than 60% of roads are unpaved, compared to 46% in emerging Asian economies and 17% in Europe.

According to Zimmerman, it often takes longer to move agricultural or other products by rail within one Latin American country than to ship them to Europe. “In both regions, China has become a very important partner and catalyst,” he adds. “In Latin America, China’s banks invest more than the World Bank and the Inter-American Development Bank combined.”

Labor worries

Finally, logistics managers who have been long reliant on Asian manufacturers may have to adjust their strategies. This is the view of Alvarez & Marsal, a global professional services firm noted for its work in turnaround management and performance improvement of high-profile businesses.

Geoff Pollak, a managing director with the firm, says that many shippers will weigh the cost of ocean and air transport in the new era of tariffs and consider on-shoring or near-shoring in this hemisphere.

“The new United States-Mexico-Canada Agreement [USMCA] could make cross-border sourcing much more attractive,” says Pollak. “At the same time, shippers should not be lulled into complacency by the temporary truce with China. This sense of détente makes some suppliers feel that they have the best hand in future contract negotiations.”

The global trade intelligence firm Panjiva says that there are “two disappointments, two delays and a high-wire act” all going on simultaneously regarding U.S. trade policy.

“The two disappointments—the passage of USMCA and the automotive section 232 review—may not go the way the administration wants,” says Chris Rogers, Panjiva’s research director. “Passage of USMCA is dependent on the support of the Democratic Party-led Congress, though Canadian elections in October may prove the more challenging hurdle.”

Furthermore, notes Rogers, the automotive industry review may fall foul of restrictive actions by any or all of the Court of International Trade, the General Audit Office and both houses of Congress. Its effectiveness will also be limited by narrow coverage that excludes Canada, Mexico, the EU and Japan.

“The administration’s delayed and ongoing trade negotiations with the EU and Japan could unlock $12.40 billion and $4.16 billion of tariff reductions respectively,” says Rogers. “Yet, the fact that the trade deal reached between the EU and Japan took four-and-a-half years to complete would indicate a finalization in 2019 is unlikely.”

That leaves a “high wire act” with China, where talks are currently scheduled to run through this March. Given that a five-fold increase in U.S. exports of energy and agricultural products to China will only cut the U.S. trade deficit with China by one-fifth, there will need to be more than just purchase commitments to avoid a “snap-up” in tariffs.

“The Chinese government has shown some willingness to adapt intellectual property and other practices already,” says Rogers. “The U.S. electronics industry is the biggest potential loser should tariffs be increased to 25% from 10%.”

Article Topics

Magazine Archive News & Resources

Latest in Materials Handling

Beckhoff USA opens new office in Austin, Texas Manhattan Associates selects TeamViewer as partner for warehouse vision picking ASME Foundation wins grant for technical workforce development The (Not So) Secret Weapons: How Key Cabinets and Asset Management Lockers Are Changing Supply Chain Operations MODEX C-Suite Interview with Harold Vanasse: The perfect blend of automation and sustainability Consultant and industry leader John M. Hill passes on at age 86 Registration open for Pack Expo International 2024 More Materials HandlingAbout the Author

Subscribe to Materials Handling Magazine

Find out what the world's most innovative companies are doing to improve productivity in their plants and distribution centers.

Start your FREE subscription today.

April 2024 Modern Materials Handling

Latest Resources