US corrugated and paperboard box demand to exceed $39 billion in 2018

Report highlights impacts of nearshoring, on-demand packaging and a rising domestic economy.

Latest Material Handling News

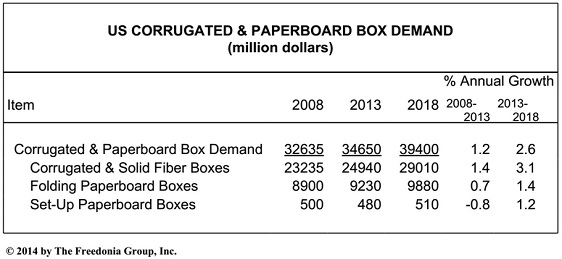

Women in Manufacturing Association to offer 4th annual Moms in MFG Conference Fox Robotics and KION NA announce strategic partnership Parcel handling on the move April Services PMI contracts following 15 months of growth, reports ISM Toyota Industries Corporation launches Toyota Automated Logistics Group to house acquired companies More NewsCorrugated and paperboard box demand in the US is forecast to increase 2.6% per year to $39.4 billion in 2018, improving from the performance of the recession-impacted 2008-2013 period.

These are among the findings of the latest report from The Freedonia Group, a Cleveland-based industry market research firm. Titled “Corrugated & Paperboard Boxes,” the report suggests box production volume will recover from declines of the past decade but will be moderated by the increased presence of lighter weight containerboard and pressures to reduce excess packaging.

According to analyst Esther Palevsky, gains will be driven by a rebound in manufacturing output and continued expansion of the overall economy. “Growing emphasis on sustainability is leading to the lightening of containerboard for boxes and the use of ‘right-sized’ boxes to reduce waste,” she said in a recent interview. “Also, pressures from retailers on vendors to reduce excess packaging will impact the outlook for volume growth.”

The reshoring of some manufacturing activity that was previously moved offshore will have a positive impact on demand for boxes, Palevsky continued, since manufactured goods tend to be packaged where they are produced and most firms buy boxes from nearby suppliers to hold down shipping costs.

Weak market conditions during and after the recession led to a number of containerboard capacity reductions to bring supply more in line with demand. “Now this is reversing and there have been some recent capacity expansions, with some completed and others expected to be completed in 2015,” Palevsky said. “Besides domestic demand due to improvement in the economy, the increased capacity will benefit from export opportunities.”

Growth will also benefit from heightened demand for value added box types such as those that feature high quality graphics and printing or are constructed in display-ready form, she said. Corrugated and solid fiber box demand will expand more rapidly than that for folding cartons and set-up boxes, advancing 3.1% annually to $29.0 billion in 2018. Growth will be fueled by the recovery in the manufacturing sector, especially in the output of food and beverages, pharmaceuticals, and other non-durables. Other factors include an improved outlook for consumer spending, a rebound in construction activity, and continued rapid growth for online shopping.

Folding carton demand is projected to increase 1.4% per year to $9.9 billion in 2018, an improvement from the 2008-2013 performance but held back by competition from other packaging formats—particularly flexible packaging. Still, prospects will benefit from the rebound in non-durable goods output, expanded opportunities in carryout food applications, and paper-based packaging’s appeal as part of sustainability efforts. Set-up box demand will also see relatively slow increases based on competition from less costly alternatives such as folding cartons and plastic containers.

Folding cartons and set-up boxes are mainly used to package single items that are lightweight. Folding carton examples would include cereal or cracker boxes, beverage cartons or carriers, frozen food boxes, carryout food boxes, cigarette boxes, etc. Set-up boxes (or rigid boxes) are non-collapsible and used to package things like chocolates, fragrances, and medical devices.

Corrugated boxes are mainly used as shipping containers for larger quantities of various manufactured products (e.g., case quantities of canned foods) or to ship single units of heavier items (e.g., appliances). They are also used for retail shipping applications (e.g., e-commerce).

Article Topics

Latest in Materials Handling

Boscov’s: Speed regained in retail distribution Women in Manufacturing Association to offer 4th annual Moms in MFG Conference Fox Robotics and KION NA announce strategic partnership Ergonomics Update: Hearing protection in the warehouse Parcel handling on the move An inside look at picking technologies April Services PMI contracts following 15 months of growth, reports ISM More Materials HandlingAbout the Author

Subscribe to Materials Handling Magazine

Find out what the world's most innovative companies are doing to improve productivity in their plants and distribution centers.

Start your FREE subscription today.

May 2024 Modern Materials Handling

Latest Resources