Automation Survey: Budgets healthy, though labor availability issues grow

Our annual automation survey finds increasing budgets for automation and rising interest in automated solutions with reliable parts availability, as well as turnkey, integrated solutions. And though budgets are up, stresses show around labor availability, raising its importance as a driver for automation.

Related Slideshow

For our annual Automation Solution Study, we asked readers where they are in their use of warehouse automation and plans and budgets for deploying more systems, as well as the factors they consider important in solutions. The main positive finding is that as we enter the second year of the global Covid-19 pandemic, readers expressed more certainty about moving forward with plans, increasing budgets for automation.

Those over-arching findings on budget and outlook are driven by familiar needs in the materials handling industry: more labor-intensive filling of e-commerce orders, tighter fulfillment cycle times, and difficulty finding enough labor. In fact, difficulty finding enough labor shot up this year as a driver for automation investments.

Modern Material Handling’s “2022 Automation Solutions Study,” conducted by Peerless Research Group, was in the field during November 2021, a year after the 2021 survey was in the field in November 2020, and roughly 18 months since the 2020 survey was conducted in April of 2020. That results in three automation surveys we’ve conducted since the pandemic hit, with less uncertainty expressed about automation plans today.

Our 2022 survey shows that budgets are growing, with more than 50% expecting more automation spending in the coming year, but stresses like concerns about labor availability, are showing more than ever. Those stresses are reflected in our survey, along with user preference for solutions that are integrated, turnkey and not prone to parts-availability problems. In short, our readers are dealing with high order volume, more difficulties finding labor, and subsequently, they want reliable automation to help them step up to these challenges.

Budgets up

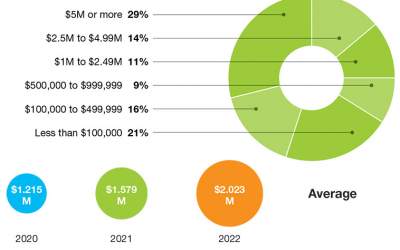

Let’s start with the positive: increasing budgets. This year, when we asked respondents how much their companies would spend on materials handling solutions and automation in the present year (choosing from budgetary dollar-range brackets), the average came to $2.02 million, up from an average of $1.57 million last year, and $1.21 million for the survey conducted in April 2020. Of course, each survey brings a new respondent mix from our reader base, but the overall trajectory shows strong growth.

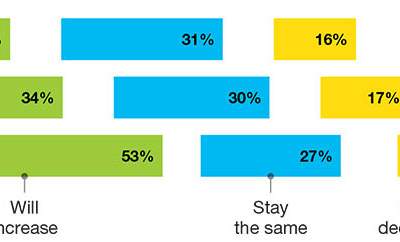

We also asked how current spend compares with anticipated spend in the coming year, and this year, 53% are expecting automation and systems spending to increase, up from 34% who answered that way in late 2020, and 24% who predicted growth in the survey before that, back in April 2020.

Given that the April 2020 survey came during the early stages of the pandemic, when plant and business shutdowns were fairly widespread, it’s not surprising the warehouse automation budget showed some hesitancy then. In that survey, 29% said it was “too soon to tell” on automation spend for the coming year. Now two surveys later, 13% have that response, a significantly lower level of uncertainty. Additionally, 7% this year expect automation spending at their company to decline, down from 17% last year, and 16% for the survey in 2020.

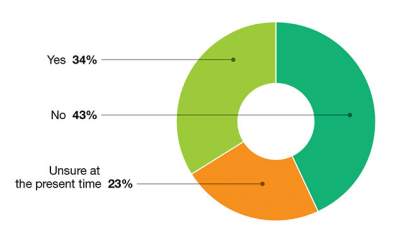

We also asked respondents whether the pandemic is causing a change in purchase plans for automation. This year, 43% said “no,” 34% said “yes,” and 23% were unsure. By comparison, last year, 24% said “no,” 35% said “yes,” and 32% were unsure. That higher “no” level indicates less uncertainty this year. This is not surprising given that the pandemic has led to an increased level of e-commerce, making many warehouses busier than ever.

The reality is that efficient DC operations are a must for a retail economy that is becoming more e-commerce based. For instance, Mastercard recently announced that preliminary analysis of its “SpendingPulse” data on the 2021 holiday season showed that e-commerce buying was up 11% versus the 2020 holiday season, and constitutes 20.9% of total retail sales for the 2021 season, up from 20.6% in 2020 and 14.6% in 2019.Add in the increased difficulties in finding enough labor, and the macro-level pressures driving the need for more automation are clearly there.

Of the 117 readers who participated in our 2022 automation study, 24% are with companies with less than $50 million in revenues, 11% are with companies with $1 billion or more sales, while the average revenue size is $710 million, down a bit from last year’s $784 million average.

The biggest percentage of respondents (64%) are locations with warehouse operations, 21% are at a corporate headquarters, and combined 12% are either at a manufacturing site or at a DC that supports a manufacturing site.

Reliability as priority

The leading evaluation priorities revealed by this survey tend to stay fairly stable year to year. Once again, system uptime and reliability are the No. 1 factor with an 89% response, same as last year. The second top factor—support and response time—stayed at the same 85% response level it did last year.

We did see a change in third spot, where “parts availability/risk of obsolescence” was cited by 80% of respondents, 10% higher than last year—enough to move this factor into third. Meanwhile, total cost of ownership (cited by 72%) slotted in at fourth this year, down from third last year. Other evaluation criteria that saw an elevated response this year were integration and compatibility, up 5%; warranty strength, up 7%; and turnkey solutions approach, up 4% versus last year. Down a bit were factors including purchase price, scalability, and green and sustainable solutions.

While we don’t ask respondents to explain their overall approach to evaluating automation investments, it does seem that this year, the respondents are after systems that just work. That means solutions that don’t have issues with parts, and offer reliable integration to warehouse management systems (WMS) or other systems, and that don’t place a systems integration burden on the end user organization. Many respondents may be past the “kicking-the-tires” phase when it comes to using more automation and may be more focused on the practical aspects of integrating, running and maintaining systems.

The annual survey also asks to what extent various operations and information management functions have been automated. This year, the category that saw the biggest gain is replenishment, which was automated for 6% of respondents last year, but climbed to 14% this year. Automated reporting also gained, reaching 22% this year, up from 17% last year, as did conveyance (now automated by 18%, up from 13%).

In a related question for these processes, the survey asked whether the process is currently fully automated, partially automated, or “currently manual, but with plans to automate,” or finally, “mostly/fully manual, with no plans to automate.” For example, for “storage” this year, 9% say it is fully automated, 23% say it is partially automated, and another 28% says it is currently manual, but they have plans to automate it.

The leading processes that are currently manual, but with growing percentages in terms of plans to automate, include retrieval (31%); picking (30%); storage (28%); followed by packaging (27%).

Pandemic impacts

The study asked whether the pandemic has changed plans around DC automation. As mentioned previously, this year, a much higher percentage (43% compared to 24% a year before) reported that “no,” the pandemic wasn’t changing purchase plans, while those unsure dropped from 32% a year ago, to 23% this year.

Generally, less hesitancy shows in terms of worrying about facility shutdowns and being able to install automation during a pandemic. A year before, the comments included ones like “we put projects off but are now revisiting them in a limited form,” whereas this year, the comments were about pandemic-related demand being strong, driving consideration of solutions to deal with increasing orders and supply chain constraints.

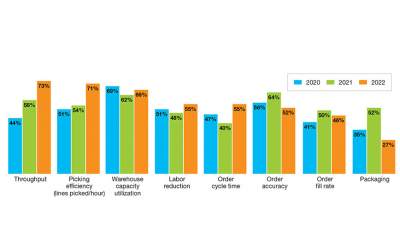

In terms of the operational areas they’d like to improve within the next two years, top areas this year include throughput—highest at 73%—followed by picking efficiency (71%), and warehouse capacity utilization (66%). Additionally, order cycle time, at 55%, was up 15%, while interest in reducing the labor requirement also grew, from 48% last year to 55% this year.

Fulfillment automation needs

While it’s true that very few warehouses can be considered fully automated, “lights-out” facilities, this survey shows that most DCs aren’t manually run sites, either.

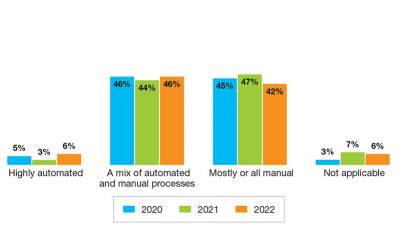

When we asked readers to select the level of automation in their fulfillment operations, on a scale of highly automated, a mix of automated and manual, and mostly or completely manual, as well as non-applicable, 46% said their DCs rely on a mix of automated and manual processes (same as a last year), while 6% said they have highly automated warehouses. That leaves 42% who said their DCs are largely or completely manual, the lowest that response has been in the past three years.

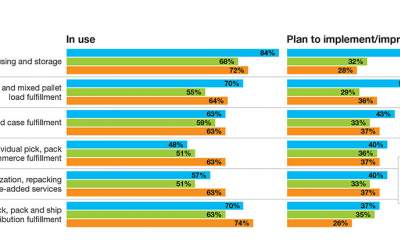

In terms of current order fulfillment activities, most companies (72%) currently use warehousing and storage; 74% do individual pick, pack and ship for wholesale distribution fulfillment; and 64% execute full and mixed pallet load fulfillment. Sixty-three percent currently have case and mixed case fulfillment, and 63% are doing order customization, repacking and value-added services (VAS). Compared to the previous survey’s current use levels, increased responses were seen this year for individual pick, pack and ship for e-commerce (up 12%), as well as customization and VAS (also up 12%).

When we followed up on which activities respondents are looking to improve over the next 24 months, this year’s survey saw increased percentages for improving or implementing new systems for full and mixed pallet load fulfillment (up 7%), case and mixed case (up 4%), customization and VAS (up 4%), as well individual pick, pack and ship for e-commerce fulfillment (up 1%).

Equipment needs

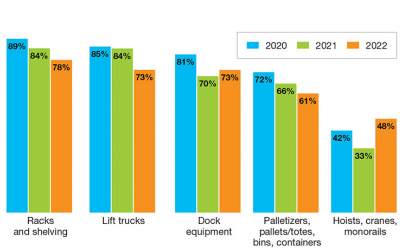

Conventional equipment like lift trucks and dock doors, some of which may have digital elements, remain widely used, with use rates over 70% for some key categories.

For example, 78% said they use rack and shelving, while 73% use lift trucks, 73% use dock equipment, 61% use palletizers, and 48% report using hoists, cranes and monorails. Compared to last year’s snapshot of present use for such equipment, the “in-use” level for hoists and cranes was up 15%, but the others remained fairly stable.

When asked about two-year plans for these categories of conventional equipment, companies are most interested in upgrading or implementing hoists, cranes and monorails (52% this year vs. 35% last year), as well as the broad category of palletizers, pallets, totes, bins and containers (40% this year, up 1%).

Robotics growth

Our study asks about various types of fixed and mobile warehouse automation, including robotics. We also ask about plans to upgrade or implement these technologies over the next 24 months.

For example, one of the most widely used categories of automated equipment is conveyor and sortation systems, reported to be in use by exactly half of respondents, even with last year’s survey. When it comes two-year plans, 50% said they have plans for conveyor/sortation.

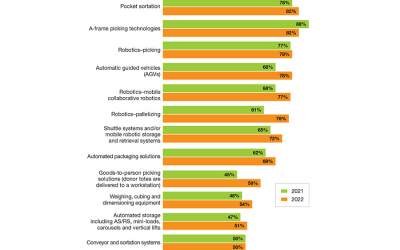

Current in-use levels were down a bit for most robotics categories compared to last year, but when it comes to plans to upgrade or implement over the next 24 months, the robotics categories drew higher percentages compared to last year. For example, this year, 23% said they use collaborative, autonomous mobile robots (AMRs), down from 32% last year. However, 77% this year report they have plans for AMRs over the next two years, 9% higher than last year’s response.

Robotic piece picking was reported as in use by 22% this year, versus 21% last year. However, over the next 24 months, 78% have plans for robotic picking solutions, up from 68% last year.

Another growth area is robotic palletizing, reported to be in use by 24% this year, but when it comes to plans to upgrade or implement robotic palletizing over the next 24 months, this year, 76% reported they had plans for robotic palletizing, up from 61% last year.

Other categories on the upswing when it comes to 24-month plans for upgrading or deploying include pocket sortation; automatic guided vehicles (AGVs); shuttle systems; goods-to-person picking systems; automated storage and retrieval systems (AS/RS); automated packaging solutions; and cubing, weighing, and dimensioning solutions. Goods-to-person solutions in which donor totes are delivered to a workstation, was particularly high growth in terms of two-year plans, up 14%.

Data capture solutions

When it comes to data collection technologies, our survey found the highest use level for bar code scanners (66%), though at a lower percentage than in the previous two surveys. We also found that mobile/wireless technologies are in use by 63% this year (up from 58%), while radio frequency identification (RFID) technology is now in use by 39%, up 14% versus last year.

Use of heads-up displays and vision technologies is in use by 26% of respondents this year, up from 12% last year. Voice directed solutions were at 21% this year, down 2% from last year. Pick- and put-to-light systems were in use by 31% this year, up from 15%.

We also ask respondents if they plan to upgrade or implement new data collection technologies over the next 24 months. We found the leading areas for improvement are RFID, with 51% having plans, pick/put to light (49%), and voice solutions (also at 49%). Forty-three percent have plans for heads-up glasses displays/vision, which is 10% higher than last year.

Software priorities

Last year, when we asked which categories of supply chain execution software were currently in use, most categories were down slightly, except for slotting. This year, almost all categories rose in terms of “in-use” percentages, except for warehouse management system (WMS) software, which dipped 1%, but remains the most widely deployed type of software we ask about.

This year, the “in-use” findings on the rise included transportation management system (TMS) solutions, in use by 57%, up from 38%; warehouse control systems (WCS), in use by 53%, up from 31%; labor management systems (LMS), now in use by 45%, up from 23%; slotting, in use by 42%, up from 25%; and warehouse execution systems (WES), now in use by 42%, up from 25%. Parcel rating systems and computerized maintenance management systems (CMMS) also made gains in the “in-use” question, with CMMS up by 20%.

We also ask about higher level supply chain and enterprise resource planning (ERP) software. We found the “in-use” levels remained fairly stable for these categories this year, though order management systems (OMS) drew a 79% response this year, up from 57%. The closely related category of distributed order management (DOM) also saw a higher current use level this year, at 63%. Additionally, we found 56% currently use DC network design and optimization solutions, up from 36% last year.

When it comes to two-year plans for upgrades or new deployments across these supply chain categories, this year the only growth categories were customer relationship management (CRM), up by 6%, and ERP, which 41% have plans for, up from 34%.

Provider trends

Overall, our survey did not find huge changes in what type of partners end-user organizations turn to for automation solutions, though systems integrators did make some gains. For example, this year, 62% said they purchase from a distributor or dealer, up 2%. Purchasing a system direct from the manufacturer came in at 66% this year, up from 56% last year.

That was enough to make buying from the OEM the top channel choice this year, higher than dealers at 62%, and systems integrators coming in third at 50%, 10% higher than last year.

In terms of which entities will help with future purchases, things look good for systems integrators, named by 48% as likely channel partners for future automation solutions, which is a sharp 20% gain versus last year.

We also ask about system maintenance issues such as which sources are used for parts, and who handles maintenance. These findings remained very steady, though we saw a 5% gain in sourcing spares or maintenance parts direct from the OEM. In terms of who handles maintenance, internal maintenance crew (67%) tops third-party services firms (44%) and OEM contract (40%).

Tough challenges as driver

As mentioned previously, this survey shows that budgets are on the upswing, with 53% saying their budget for materials handling automation is up for 2022 compared to 2021, a close to 20% gain versus last year.

For some respondents, the automation budget can be substantial. Asked for current year (2021) budget, 11% plan to spend between $1 million to 2.49 million; 14% will spend $2.5 million to $4.99 million; and another 29% plan to spend $5 million or more.

In warehouse operations, one of the top challenges is the ability to find enough reliable warehouse associates. This year, when we asked readers to rank the top challenges influencing automation purchase plans, the “inability to find and retain reliable DC associates” moved up to the third spot as a top challenge driving the automation strategy, right behind the “need to fill orders faster to meet service levels” and “increased piece picking and packing driven by e-commerce.”

It’s difficult to unbundle these top three drivers for solutions, since picking more e-commerce orders, and completing those orders quickly and accurately, either takes more people if you stick with manual workflows, or it takes more automation. Findings like the elevated status of labor concerns as a decision driver, coupled with strong e-commerce growth, bode well for growing automation use in 2022.

Analyst firm IDC, in its supply chain predictions for 2022, is estimating that by the end of 2022, chronic worker shortages will prompt 75% of supply chain organizations to prioritize automation investments, resulting in productivity improvements of 10%. Automation vendors may quibble that the productivity gains from automation can often run higher than that, but that mid-70 percentile increase in plans around automation tracks close to what we found when it comes to two-year plans. In short, more automation is shaping up as a necessity to offset extraordinary challenges, rather than an incremental cost-savings step.

Article Topics

Automation News & Resources

Materials Handling Robotics: The new world of heterogeneous robotic integration Coles automates grocery distribution in Australia 2024 Intralogistics Robotics Survey: Robot demand surges Up close and personal with mind twisting special purpose robots Warehouse automation extends life of cheese DC by a decade C-Suite Interview with Knapp’s Josef Mentzer: MODEX 2024 eclipses expectations MEGALINEAR MLR-45: Innovation in Logistics and Material Handling More AutomationLatest in Materials Handling

Geek+ and System Teknik deploy PopPick solution for pharmacy group Med24.dk Beckhoff USA opens new office in Austin, Texas Manhattan Associates selects TeamViewer as partner for warehouse vision picking ASME Foundation wins grant for technical workforce development The (Not So) Secret Weapons: How Key Cabinets and Asset Management Lockers Are Changing Supply Chain Operations MODEX C-Suite Interview with Harold Vanasse: The perfect blend of automation and sustainability Consultant and industry leader John M. Hill passes on at age 86 More Materials HandlingAbout the Author

Subscribe to Materials Handling Magazine

Find out what the world's most innovative companies are doing to improve productivity in their plants and distribution centers.

Start your FREE subscription today.

April 2024 Modern Materials Handling

Latest Resources