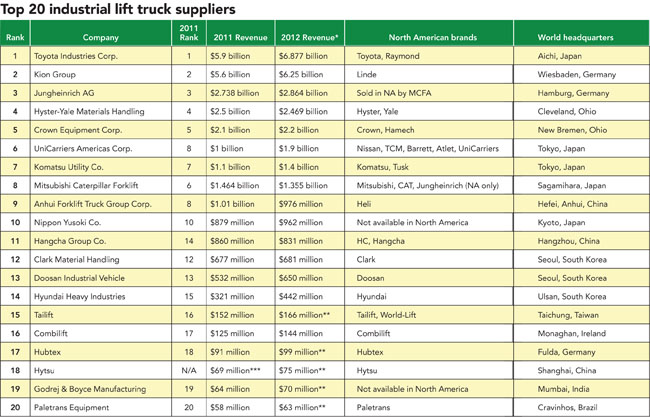

Top 20 Lift truck suppliers, 2013

After making up for 2009 with two years of strong growth, global sales have tapered off, even as the top suppliers saw revenue increases in the double digits.

The dust has settled. Following two years of very strong growth in lift truck sales, shipments leveled off in 2012. With growth at just a fraction of a percent, worldwide sales didn’t match the 27% growth in 2011 or the 32% growth in 2010. Of course, those years came on the heels of a 39% contraction, and many in the industry remain excited to see growth of any kind, however small.

Jim Moran, chairman of the Industrial Truck Association (ITA) and former senior vice president of Crown Equipment, is among them. According to Moran, the growth might be smaller, but it’s more stable as a result of more intelligent practices on the part of both lift truck manufacturers and their customers. Procuring, utilizing and replacing a piece of equipment means something different than it did just a few years ago. (Read last year’s list.)

“Large fleet owners have modified their replenishment cycles,” says Moran, “They just aren’t replacing their lift trucks in the same time frame they were. They’ve discovered, probably, that they can get away with that as long as they’re keeping an eye on maintenance costs and utilization. We’re on a slower but more sustainable curve instead of having a great year, then a slow year, and then falling behind.”

The worldwide picture looks to have reached a plateau, but news is good for this year’s Top 20 lift truck suppliers. Of those who reported their revenues to Modern, only three saw year-over-year decreases. These small, roughly 3% reductions could simply be due to currency conversion rates. As a whole, however, the Top 20 bested last year’s $27.2 billion in revenues by $3.2 billion dollars—an 11.8% increase, breaking the $30 billion mark by nearly half a billion dollars, and coming in around $30.4 billion.

Growth by region

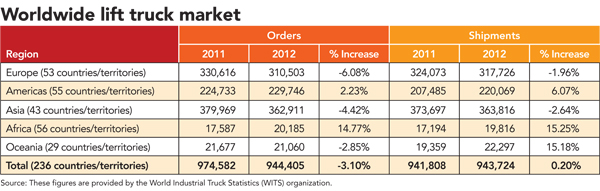

The Worldwide Industrial Truck Statistics (WITS) organization tracks quarterly and monthly statistics on lift truck sales, and is compiled by six trade groups based in North America, Brazil, Japan, Korea, Europe and China. According to the 2012 WITS figures, global orders fell by slightly more than 3% in 2012, from 974,582 units to 944,405 units. Shipments crept up 0.2%, finishing at 943,724. Highlights of the WITS figures include:

- After posting the lowest growth rates in 2011, Africa now boasts the strongest growth, with a near 15% improvement in orders and shipments. Nearly 20,000 units were shipped to African countries in 2012.

- In Oceania (Australia and nearby islands), shipments were also up more than 15%, with 22,297 units shipped.

- The next strongest growth was in the Americas, where a 6% increase in shipments saw about 220,000 units shipped. According to figures from the ITA, nearly 180,000 of those are United States sales, as compared to 166,000 units in 2011.

- Asia saw a slight decline in orders (-4.4%) and shipments (-2.6%), but still shipped 363,816 units, or 39% of global shipments.

- Europe’s orders fell 6%, with shipments down 2%, for a total of 317,726 units shipped.

The Top 10

With revenues up 16.6%, Toyota Industries Corporation once again claimed the No. 1 spot, staying ahead of Kion Group. Toyota’s $6.88 billion is $620 million more than Kion’s $6.25 billion, with the leader’s revenues 10% larger than the challenger’s. In 2011, Toyota was 5% ahead of Kion, which grew by nearly three quarters of a billion dollars between 2011 and 2012.

The rest in the top five are familiar faces. Jungheinrich again ranks third with 4.6% growth to $2.86 billion. Hyster-Yale Materials Handling (which previously reported as NACCO Industries; NACCO’s materials handling business was spun off in mid-2012) held fourth despite a roughly 1% drop in revenues for a total of $2.47 billion. Appearing again in fifth is Crown Equipment with 4.8% growth to $2.2 billion.

In sixth place is UniCarriers, the result of a merger between last year’s eighth-place finisher, Nissan Forklift, and last year’s 11th-place finisher, TCM. Combined, the companies’ individual revenues in 2011 were $1.75 billion. The new entity sits at about 8.6% above that, with 2012 revenues of $1.9 billion.

In seventh place for the fourth year running is Komatsu, which posted $1.4 billion for 27% growth, the largest growth percentage on the list.

Dropping two ranks to eighth place, Mitsubishi Caterpillar Forklift (MCF) reported $1.355 billion in 2012 revenues, down 7% from last year. In June of 2012, the company restructured its forklift production, with plans to transfer production of small- and medium-sized forklifts from Japan to facilities in China and Houston, Texas, by the end of 2013. The move was intended to bring production closer to target markets.

After launching a number of new products, in November of 2012 Mitsubishi Heavy Industries (MCF’s parent company) announced plans to merge its forklift business with that of last year’s 10th place finisher, Nippon Yusoki, by April 2013. Representatives for the new entity, Mitsubishi Nichiyu Forklift Co., Ltd., confirm they intend to report jointly next year.

Holding steady in 2012 with $976 million in revenues, No. 9 Anhui Forklift, the Chinese makers of Heli forklifts, fell slightly off the $1 billion in revenues it has posted in the previous two years, for a drop of 3.4%.

Rounding out the Top 10 is Mitsubishi Nichiyu Forklift, which reported last year as Nippon Yusoki Company. With $962 million in revenues, the company saw more than 9% growth.

Breaking down the Top 20

The TCM/Nissan merger has shaken things up for the top half of the list. By next year, it could take more than $1 billion in revenue to crack the Top 10. Combined, the Top 10 companies collected more than $27 billion in revenues in 2012, just $126 million less than the entire Top 20 list of 2011. In that year, the Top 10 accounted for about $24 billion, meaning the top half of the list has grown by almost 13%.

The Top 5, all of which are the same companies as last year, have fared well, growing by a combined $1.86 billion, or nearly 10%. For the lower half of the list, companies ranked 11 through 20 gained a combined $272 million in revenues, a 9% increase.

Trends to watch

Moran says the lift truck is increasingly becoming a platform for technologies that enable better processes and better productivity. “What people are looking for now is technology for efficiencies beyond the truck, beyond incremental improvements in truck performance like lowering a little faster or traveling a little faster,” he says. “Customers are looking for add-ons that can make their workforce better and more efficient.”

Moran says automation and efficiencies are becoming more popular among those making lift trucks and those buying them. “There’s a lot of conversation around driverless lift trucks, if not a lot of business,” he says. “All of that is still developing. It’s too early to realize how the warehouse would have to change if its lift trucks were driverless. There are infrastructure, safety, security and support concerns, and it’s too early to know.”

Last year, Moran noted an increased interest in green and sustainable objectives with regard to using and powering lift trucks. “The green initiative is kind of a given now,” he says. “You have to be focused on it and be able to communicate that the initiatives make good business sense.”

In the year to come, Moran says he will be watching the initial public offering (IPO) of Kion. “Many are interested in what the Chinese influence on that company might be down the road,” he says. “That could impact the North American market as they add products.”

With regard to the economy, Moran says industry growth will continue at a similarly slow rate as the overall economy. “That said, we’re rapidly approaching the point where we can be slightly more optimistic rather than maintaining this cautious optimism,” he adds.

How the suppliers are ranked

To be eligible for Modern’s annual Top 20 lift truck suppliers ranking, companies must manufacture and sell lift trucks in at least one of the Industrial Truck Association’s seven truck classes: electric motor rider; electric motor hand trucks; internal combustion engine; pneumatic tire; electric and internal combustion engine tow tractors; and rough terrain lift trucks.

Rankings are based on worldwide revenue from powered industrial trucks during each company’s most recent fiscal year. Revenue figures submitted in foreign currency are calculated using the Dec. 31, 2012 exchange rate.

Article Topics

Special Reports News & Resources

Automation/Retail Special Issue: Savvy users embrace change Research Report: Use of Automation in Warehouse/DC Special Digital Issue: Warehouse/DC Robotics System Report: Building the world’s best warehouse Top 20 Warehouses 2019 Top 20 automatic identification and data capture suppliers 2019 Top 20 Lift Truck Suppliers in 2019: Market reaches new heights More Special ReportsLatest in Materials Handling

Boscov’s: Speed regained in retail distribution Women in Manufacturing Association to offer 4th annual Moms in MFG Conference Fox Robotics and KION NA announce strategic partnership Ergonomics Update: Hearing protection in the warehouse Parcel handling on the move An inside look at picking technologies April Services PMI contracts following 15 months of growth, reports ISM More Materials HandlingAbout the Author

Subscribe to Materials Handling Magazine

Find out what the world's most innovative companies are doing to improve productivity in their plants and distribution centers.

Start your FREE subscription today.

May 2024 Modern Materials Handling

Latest Resources