Top 20 lift truck suppliers, 2014

Our list grows top heavy following another big merger, but after a year of relative calm, the market is heating up once again.

The past few years have been a roller coaster for the lift truck industry, which has proved innovative and resilient enough to rapidly overcome the tumult of the Great Recession. But the market is a far cry from its pre-downturn self, as fleet management and a proliferation of new technologies have reshaped how lift trucks are procured and used.

Thankfully for all stakeholders, the market is now enjoying increased stability, as evidenced in Modern’s annual list of the Top 20 lift truck suppliers.

Brian Butler, chairman of the Industrial Truck Association (ITA) and president and CEO of Linde Material Handling North America, says last year’s strong 5% growth in unit sales is on track for a repeat performance.

But the transactions will look very different as fleet owners increasingly value and quantify the impact of a lift truck on the entire business. Butler suggests the changing and deepening relationship between suppliers and end-users is not unique to the lift truck market.

“Customers are becoming smarter about materials handling in general,” Butler says. “They will continue to be diligent about managing their businesses, but 2009 opened a lot of people’s eyes. They’re looking harder at a huge wealth of opportunities and longer-term solutions.”

Traditionally, a business might spend in some areas and squeeze others, Butler says. Lift trucks were often among the first places to see spending cuts, but increased visibility into total cost of ownership has exposed the true costs of maintaining aging equipment. “Investment in a fleet is a way to improve productivity,” Butler says. “We find some customers are buying units earlier or in greater numbers because they can actually see savings while improving productivity. For those who haven’t bought a lift truck in the last five years, there are a lot of things they might not be aware of, but all OEMs are prepared to have those discussions.”

Growth by region

The Worldwide Industrial Truck Statistics (WITS) organization tracks quarterly and monthly statistics on lift truck sales, and is compiled by six trade groups based in North America, Brazil, Japan, Korea, Europe and China. According to the 2013 WITS figures, global orders increased by 7% from 944,405 to 1,009,777. This follows a 3% decline in orders in 2012. Shipments were up 5% after staying level from 2011 to 2012.

Since 2008, shipments to the Asia region have increased 46%, while shipments to the Americas rose 6% over the same period. Europe’s shipments have yet to recover from the losses of the recession, with shipments down a total of 21% since 2008. Globally, shipments are up 7% in the last seven years. Highlights of the 2013 WITS figures include:

-

The Americas posted the strongest growth in shipments at 238,455 units, up more than 8% year over year and following a 6% increase last year. According to figures from the ITA, 172,073 units of Class 1 through 5 lift trucks were United States sales, as compared to 153,083 units in 2012, an increase of more than 12%.

-

After a near 15% growth rate in orders and shipments last year, Africa has fallen by 6% and 5% respectively. A total of 18,903 units were shipped to African countries in 2013.

-

In Oceania (Australia and nearby islands), shipments were also up better than 15% in 2012, but have since fallen by 6% to just 20,835 units in 2013.

-

After Asia saw a slight decline for 2012 in orders (-4.4%) and shipments (-2.6%), in 2013 the region saw the largest increase in orders (10.6%) and second-largest increase in shipments (8%). Shipments to the region totaled 394,054, accounting for 40% of global shipments.

- Europe’s orders fell 6% in 2012, but held relatively level in 2013 with shipments down less than half a percent and orders up 1.6%.

The Top 10

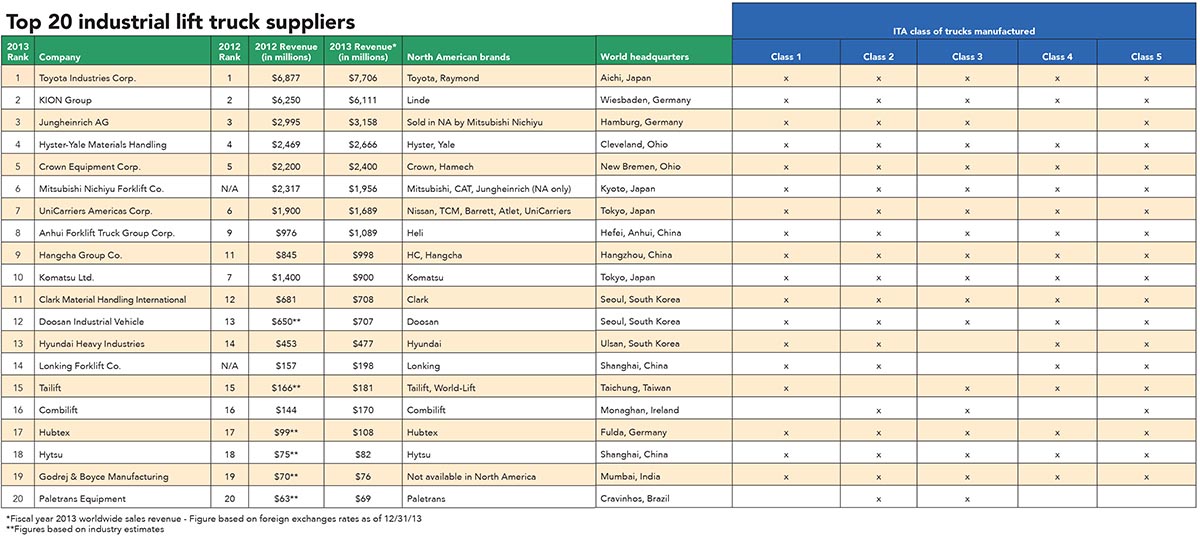

With revenues up 12%, Toyota Industries Corp. is once again No. 1 on our list, pulling further ahead of Kion Group. Toyota’s revenues of $7.7 billion are $1.6 billion more than Kion’s $6.11 billion, with the leader’s revenues 26% larger. In 2011, Toyota was 5% ahead of Kion.

Outlining the factors behind the increased revenues, Toyota executives cited the 2013 acquisition of Cascade Corp., a major manufacturer of lift truck attachments, and the launch of the new Toyota 8-Series lift truck line with new large capacity models and two new engines. “These activities led to an increase in unit sales worldwide,” a statement released by Toyota said. “The markets in China and North America registered growth, the European market showed a recovery, and the Japanese market maintained solid sales.”

Though Kion’s 2013 revenues dipped slightly, the numbers follow 12% growth of nearly three quarters of a billion dollars between 2011 and 2012. In a statement, Gordon Riske, CEO of the Kion Group, said “we now want to take advantage of the economic recovery in Western Europe, expand our excellent position in emerging markets, further strengthen sales and service and increase our profitability yet again. New products and our successful modular and platform strategy will play a key role in this respect.”

The rest of the top five held their rankings from last year, with Jungheinrich ranking third after posting 5% growth to $3.16 billion. Hyster-Yale Materials Handling again ranked fourth, and following a slight drop in revenues in 2012 has bounced back with 8% growth to $2.66 billion. Crown Equipment rounded out the top 5 with 9% growth to $2.4 billion.

In its first appearance on our list, Mitsubishi Nichiyu claimed sixth place with $1.96 billion. The company previously reported separately as Mitsubishi Caterpillar Forklift (ranked eighth last year) and Nippon Yusoki (ranked tenth last year). The companies’ individual revenues last year totaled $2.3 billion. Reporting jointly, the company bumps UniCarriers down one position and makes room for Hangcha to join the Top 10.

Seventh-place finisher UniCarriers is the result of a 2012 merger between Nissan Forklift and TCM, who have previously been ranked eighth and eleventh place, respectively. In its second year on our list, UniCarriers reported revenues of $1.69 billion, an 11% decrease from 2012, which had seen a 9% increase over Nissan’s and TCM’s individual revenues. It’s worth noting that foreign exchange rates impact all members of the Top 20 list. In the case of UniCarriers, sales in yen were actually up 9% before converting to dollars.

Following a slight decline in revenues last year, Anhui Forklift, the Chinese makers of Heli forklifts, reported revenues of $1.09 billion, a nearly 12% increase. Becoming the second Chinese company in the Top 10, Hangcha Group also saw a slight decrease in revenues in 2012. In 2013, the company reported 18% growth to come just $2 million shy of $1 billion in revenues.

Rounding out the top 10 is Komatsu, which posted the largest percentage increase on last year’s list after revenues spiked 27% from 2011 to 2012. The company fell short of that $1.4 billion high water mark this year with $900 million, but that number is on par with 2010 and 2011 revenues and 20% higher than the company’s 2009 earnings. And again, the conversion from yen to dollars also played a role in Komatsu’s earnings.

Breaking down the Top 20

Last year, the TCM/Nissan merger shook things up for the top half of the list. This year it’s the merger of Mitsubishi Heavy Industries and Nippon Yusoki into Mitsubishi Nichiyu. With all the consolidation at the top, it could take more than $1 billion in revenues to crack the Top 10 next year. In 2010, that feat took only about $600 million.

In 2012, before Mitsubishi’s merger, the combined revenues for the lower half of the list were $3.2 billion, a 9% increase from the prior year. This year, companies ranked 11 through 20 reported a total of $2.78 billion, a nearly 14% decrease. This reflects the ongoing consolidation at the top of the list.

Earnings of the 2013 Top 20 list total $31.45 billion, a 2.2% increase. Only four companies saw revenues fall in 2013—all of them in the Top 10—but each had enjoyed a banner year in 2012. Despite the fact that those four companies reported a combined $1.2 billion less than in 2012, the Top 10 still collected more than $28.7 billion in revenues in 2013, about $1.4 billion more than in 2012. In 2011, the Top 10 accounted for about $24 billion, meaning the top half of the list has grown by almost 20% in two years.

The Top 5, all of which are the same as last year, have fared well, growing by a combined $1.25 billion, or 6%. The Top 5’s revenues now account for 70% of the Top 20’s total revenues.

Standout performances in terms of year-over-year growth include a 26% surge for China’s Lonking, as well as 18% increases for both ninth-ranked Hangcha and No. 16 Combilift.

Notable performances since 2009

Aside from the recession, factors such as currency conversion rates and restructurings can influence a comparison of revenues over the past five years. That said, in its five consecutive years at the top of our list, Toyota’s revenues have grown by 68%. Holding firm to second place over the same period, Kion’s 2013 revenues are 50% larger.

Clark and Combilift have each boosted revenues by 75% since 2009, but the largest growth is from Hyundai, whose 2013 reported revenues are exactly twice those claimed five years ago. Hyster-Yale and Crown have spent the past five years exchanging fourth and fifth place, with the former growing 78% in that time. Crown is up 50% over the same period.

How the suppliers are ranked

To be eligible for Modern’s annual Top 20 lift truck suppliers ranking, companies must manufacture and sell lift trucks in at least one of the Industrial Truck Association’s seven truck classes: electric motor rider; electric motor hand trucks; internal combustion engine; pneumatic tire; electric and internal combustion engine tow tractors; and rough terrain lift trucks.

Rankings are based on worldwide revenue from powered industrial trucks during each company’s most recent fiscal year. Revenue figures submitted in foreign currency are calculated using the Dec. 31, 2013 exchange rate.

Article Topics

Special Reports News & Resources

Automation/Retail Special Issue: Savvy users embrace change Research Report: Use of Automation in Warehouse/DC Special Digital Issue: Warehouse/DC Robotics System Report: Building the world’s best warehouse Top 20 Warehouses 2019 Top 20 automatic identification and data capture suppliers 2019 Top 20 Lift Truck Suppliers in 2019: Market reaches new heights More Special ReportsLatest in Materials Handling

Geek+ and System Teknik deploy PopPick solution for pharmacy group Med24.dk Beckhoff USA opens new office in Austin, Texas Manhattan Associates selects TeamViewer as partner for warehouse vision picking ASME Foundation wins grant for technical workforce development The (Not So) Secret Weapons: How Key Cabinets and Asset Management Lockers Are Changing Supply Chain Operations MODEX C-Suite Interview with Harold Vanasse: The perfect blend of automation and sustainability Consultant and industry leader John M. Hill passes on at age 86 More Materials HandlingAbout the Author

Subscribe to Materials Handling Magazine

Find out what the world's most innovative companies are doing to improve productivity in their plants and distribution centers.

Start your FREE subscription today.

April 2024 Modern Materials Handling

Latest Resources