2013 Warehouse/DC Equipment and Technology Survey: Moving more, spending less

Our annual outlook survey finds the industry steadying for a new, slower pace of growth following the release of pent-up demand after the downturn. Yet, even as planned spending drops off, facility activity is the highest since 2007—signaling that “doing more with less” has stuck.

Just as an effective materials handling system cannot be shaped around one data point, interpreting the results of an industry survey is about more than just the bottom line.

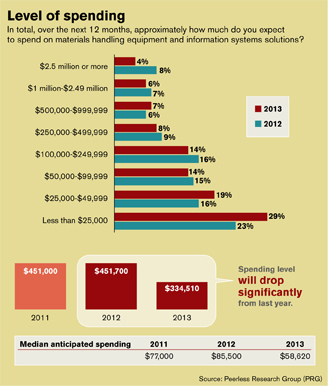

For instance, take a look at the average materials handling budget as reported by Peerless Research Group (PRG) in the 2013 State of Warehouse/DC Equipment and Technology Survey. At nearly 26% less than last year, the average anticipated spending among the survey’s 597 respondents is just $334,510. In fact, about half of those respondents plan to spend less than $50,000.

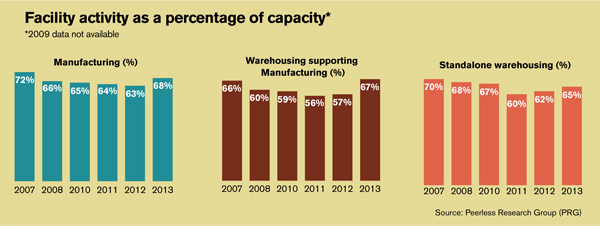

But if we look at activity levels, facility capacity numbers have jumped up by as much at 10% in one year—following six consecutive years of decline. According to John Hill, director at St. Onge, capacity figures between 60% and 70%, although a big improvement, are still below a certain threshold. When they rise above 70%, he says, it’s often necessary to spend on materials handling equipment just to keep up. In the meantime, most businesses will tend to sit tight.

“In the past couple of years, we saw the effect of delayed spending,” says Hill. “Now, many have caught up; and unless growth is phenomenally good, there won’t be as much pressure to spend. We’re looking at modest growth that perhaps many feel they are able to handle.”

In fact, respondents expressed a great deal of optimism that they could handle it. When asked about their anticipated activity levels over the next two years, almost 95% said that they expected activity to increase or stay the same. To be fair, more than 50% of respondents suggested their warehousing activity would stay the same.

According to George Prest, CEO of Material Handling Industry (MHI), growth is projected to improve into 2014. Following industry growth rates of 14% in 2011 and 10% in 2012, 2013 could hover around 6% before breaking double digits again in 2014.

“We’re on the declining side of the growth curve,” says Prest, “but we can expect to see things trending upward from here. Specific industry segments will pick back up at different times, but the overall outlook is good.”

Demographics and reduced spending

This year’s respondent base of 597 is about twice last year’s base of 314 survey responses. However, according to Judd Aschenbrand, director of research for PRG, the demographic breakdown of the group remains statistically similar to last year.

One notable change is in the level of participation in the southern and southeastern part of the country, where 20% of respondents are located—as compared to just 10% in last year’s results. Aschenbrand also pointed to the political and economic climate at the time of the survey, which was fielded in January as President Obama was poised to begin his second term.

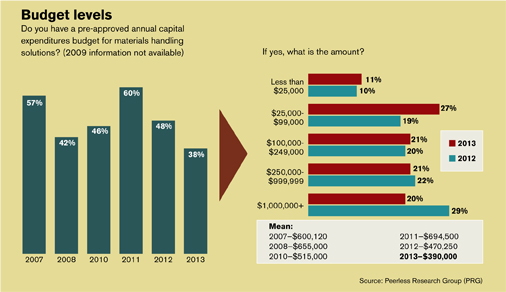

A level of uncertainty was reflected in the 50% of respondents who said that they will take a “wait-and-see” approach in 2013, up from 46% last year. Those with pre-approved capital expenditure budgets for materials handling solutions dropped from 60% in 2011 and 48% in 2012 to 38% this year, averaging just $390,000. Both figures are the lowest in seven years.

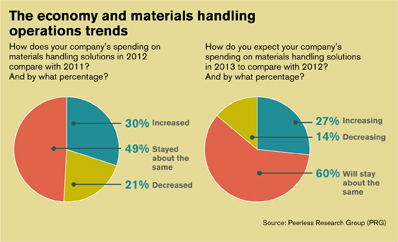

The uncertainty also made an impact on optimism as compared with January 2012, when 40% of respondents to last year’s survey said they expected their materials handling spending to increase in 2012. This year, only about 30% said that had been the case, and just 26% expect spending to increase in 2013. In 2012, 45% said they expected spending to stay the same in the coming year, but now almost 60% expect their spending to remain unchanged in 2013.

According to Jim Moran, chairman of the Industrial Truck Association and member of the board of directors at Crown Equipment, the industry might want to get used to a slow and steady approach.

“Everyone is being very conservative, but that’s predictable given the news you hear today and the level of uncertainty,” says Moran. “The tendency is to feel negative, and it’s hard to shake that. The reality is that it’s not that bad, but it’s so much different than anything we’ve seen in the past. I think the industry is moving gradually forward in a positive way, but it’s a pace we have to get used to, because I think it’s going to be around for a while.”

The return of labor

The 14% of respondents who reported that they would hold off on investments in the coming year will avoid primarily big-ticket items like automation, storage, and technology and software. The 19% who plan to proceed with investments are looking at the same technologies, including conveyors and sortation, information technology like warehouse management systems (WMS) and enterprise resource planning (ERP) systems, as well as automatic guided vehicles and robotics.

Hill says that the outlook for robotics suppliers is good as solutions for picking and packing gain momentum. But he was quick to point out that manpower remains an effective solution, particularly for retailers facing the e-commerce boom. He pointed to the 43% of respondents who plan to spend on labor and staffing in 2013, up from 40% in 2012 and 37% in 2011.

However, MHI’s Prest suggests that hiring practices have evolved in recent years. As companies expand their labor forces, they will tend to recruit and train with an eye toward long-term retention. No longer content to “throw bodies at the problem,” businesses will use employees to leverage investments in technology, maximizing the productivity of each. “It’s a different kind of hiring,” he says. “People are being more cautious about the types of employees they bring into their companies.”

As respondents work to grow their workforce and productivity, it is not surprising that safety tops the survey’s list of most important issues, placing above company growth, throughput, and last year’s top issue: cost containment. Moran suggests the reason productivity metrics have fallen in importance is due to the spending on technology in recent years, which has helped many companies to be more efficient and reduce cost.

“It’s one of the reasons we saw employment numbers hold steady while productivity increased,” says Moran. “People are employing every ounce of technology they can as warehousing becomes more and more sophisticated.”

But, there is perhaps a limit to how much productivity can increase while headcount stays the same. Hill suggests that, following the recession’s layoffs and large investments in technology, we might expect to see staffing levels and productivity return to synchronous growth.

This corresponds to the survey’s anticipated increase in the importance of training, which 57% of respondents said is very important today—but which 63% said would be more so in the next two years. As technology spreads to every facet of operations, says Moran, workers will need to become conversant in increasingly complex information systems.

Information technology and supply chain software

New entrants into the workforce will be surrounded by technology designed to make them more productive than ever. The change is already underway with lift trucks, where operators need both the mechanical skills to operate the machine and the abstract skills to interface with tablets and voice-based data systems.

Fully half of respondents report that they plan to invest in information technology hardware and software in the coming year, and Hill says that the trend is toward a convergence of software such as WMS, warehouse control systems (WCS), and ERP—the enterprise applications in which 25% of respondents are planning to invest. In 2011, just 12% had plans for enterprise applications.

“For more than 20 years, we’ve been talking about trading partner collaboration and the importance of sharing information across trading partners to reduce order cycle times and improve visibility,” says Hill. “People are embracing collaboration not just philosophically, but actually. If that’s true, it suggests we need to make investments in technology and systems that enable real-time information.”

Companies are beginning to recognize that unless they’re able to share information with their trading partners, they’re going to fall behind the curve, says Hill, and they are looking to suppliers to provide everything—WMS, WCS, ERP, customer relationship management, and sales and operations planning—on a single platform.

Respondent demographics

In January, Peerless Research Group e-mailed survey questionnaires to readers of Modern Materials Handling and Logistics Management, yielding 597 qualified respondents from manufacturing (39%), warehousing (21%), corporate (25%) and aligned logistics professionals (15%). Revenues of responding companies range from large (26% have annual revenues of $500 million or more) to small (47% are below $50 million). Qualified respondents are those managers and personnel involved in the purchase decision process of materials handling solutions.

Article Topics

Special Reports News & Resources

Automation/Retail Special Issue: Savvy users embrace change Research Report: Use of Automation in Warehouse/DC Special Digital Issue: Warehouse/DC Robotics System Report: Building the world’s best warehouse Top 20 Warehouses 2019 Top 20 automatic identification and data capture suppliers 2019 Top 20 Lift Truck Suppliers in 2019: Market reaches new heights More Special ReportsLatest in Materials Handling

6 Ways to Re-evalute Fulfillment This Year MHEFI awards record-breaking $231,700 in scholarships to 61 students ALAN opens nominations for 2024 Humanitarian Logistics Awards Kenco to install an AutoStore system at its Jeffersonville, Ind., DC Schneider Electric rolling out WMS and TMS solutions from Manhattan Associates at scale Leaders Q & A with Bryan Ferguson: Resurgence of RFID technology Tom Panzarella appointed Chief Technology Officer at Seegrid More Materials HandlingAbout the Author

Subscribe to Materials Handling Magazine

Find out what the world's most innovative companies are doing to improve productivity in their plants and distribution centers.

Start your FREE subscription today.

May 2024 Modern Materials Handling

Latest Resources