Top 50 in Trucking: Great management, even better operations

Analysts say our annual listing reflects the management teams that are willing to get their hands dirty in order to compete in the cutthroat world of deregulated trucking. Here are the carriers that are leverage rolling assets and technology to post the most impressive financial numbers.

Latest Material Handling News

They all operate basically the same trucks. They all haul similar trailers. They all hire from the same pool of driver candidates. They compete for the same shippers. And they all try to abide by the scores of federal and state regulations that control this economically deregulated, $720 billion industry we call “trucking.”

So what sets apart the best from the rest? “To me, it’s how senior management rolls up its sleeves and gets dirt under their nails,” says Satish Jindel, principal of SJ Consulting, a research firm that keeps a close eye on the trucking industry. “If they’re hands off and all they want to do is sit in fancy meetings and look at flip charts all day, they’re not going to cut it. If you don’t have depth of understanding in this industry, you’re not going to do well.”

Whether a trucking company has 300 or 3,000 employees, size shouldn’t make much of difference at the end of the day, Jindel adds. His research shows that it’s how trucking managers and employees interact with one another—and ultimately their customers—that matters when measuring success.

Experts and top executives agree that it’s that tactical, day-to-day awareness of what’s going on in a trucking operation that helps to set the top carriers apart. The “ins and outs” of the ever-changing trucking world change, sometimes rapidly, and top management needs to be nimble enough to answer those challenges daily.

The importance of having an active management team took on greater importance in the wake of the Motor Carrier Act of 1980, which deregulated interstate trucking. Donald Broughton, chief market analyst for Avondale Partners and a long-time trucking analyst, says that deregulation in 1980 created the “nimble” trucking industry that we know today.

Prior to deregulation, logistics costs amounted to nearly 19 percent of GDP. Today that figure is about 8.5 percent, or just about half what it was in 1980. “That’s because they deregulated the industry,” Broughton says. “This country has the lowest distribution costs in the world, which is a remarkable thing given our size.”

The best motor carriers are the ones who have adapted to that changing landscape—and many haven’t or couldn’t. Of the Top 50 motor carriers in 1979, the last full year of economic regulation, only five remain today—YRC Worldwide, ABF Freight System, UPS Freight (then known as Overnite Transportation), Central Freight Lines, and Central Transport. The rest have either ceased operations, gone bankrupt, or have merged with other entities under different names.

Today, virtually every one of the Top 25 truckload (TL) companies didn’t exist prior to deregulation—and most trucking veterans wouldn’t recognize the operations of the surviving LTL carriers because of their technology, modern freight routing software, and other 21st Century advances necessary to keep pace in today’s rapid paced delivery environment.

“It boils down to management,” says Broughton. “This is a tough business with very complex issues. With some brands, like Coca-Cola, any jockey could ride that horse. That’s not the case in freight transportation. Management does matter. Operations do matter.”

The importance of operations is underscored by the huge variables inherent every day in trucking—uneven demands due to seasonality and other factors, managing a huge capital- and labor-intensive business, and, of course, the unevenness of the overall national economy.

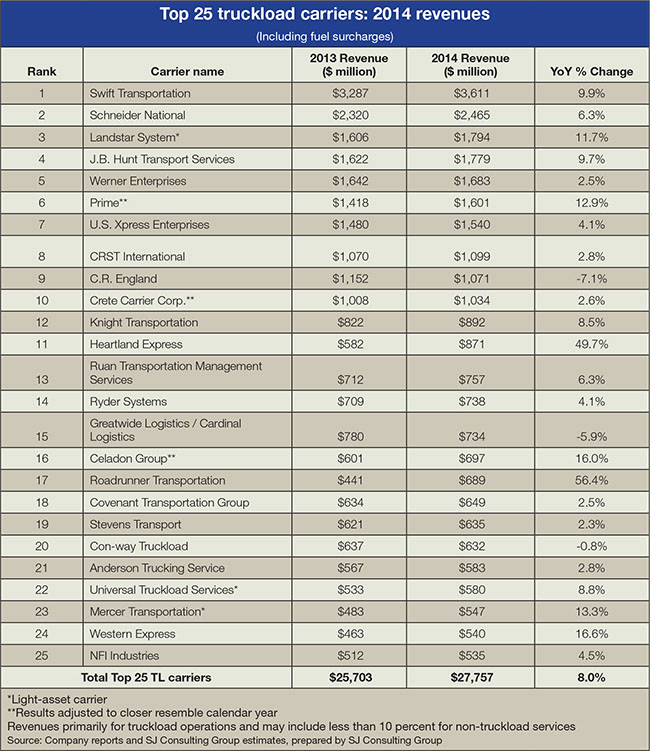

“What drives the trucking industry is variability of demand, variability of freight flows, weather, and a huge number of people and machines that help you deal with variability,” says Mark Rourke, president of truckload for Schneider National (No. 2 TL on our list). “Variability is the biggest cost driver in the industry.”

And the Top 50 continue to do well, adds Rourke, because they have the ability to invest in the best technologies and latest equipment with enhanced safety features, enabling them to cope with that variability.

“To stay on top of this ever-changing environment, all the Top 50 carriers have progressive and talented management teams,” says James Welch, CEO of YRC Worldwide. “Longevity in the marketplace is another characteristic of the Top 50 as are good operations, certainly. You have to be able to execute on what you say you can do.”

So what internal moves are the best of the best making to stay on top? Let’s take a deeper dive into what makes Logistics Management’s Top 50 tick.

Staying on top

Welch, by all reports, inherited a nearly bankrupt operation when he assumed the chief executive post at YRC Worldwide in late 2011. The company had lost in excess of $2 billion when he decided to return to the company in which he had spent his formative years in middle management.

When he took over, nearly every YRC operating unit was losing money, its workers were demoralized and fearful of losing their jobs, and shippers were beginning to question YRC’s staying power in the market place. And, of course, the company was struggling under the weight of approximately $1 billion in long-term debt.

“Getting our balance sheet right, getting equity back in our business, and extending our labor agreements through 2019 cleared up the murky waters and allowed us to reinvest in the companies and compete in the marketplace,” Welch explains. “We now have a good amount of runway in front of us, and we’re not focusing on the past six or seven years.”

Strategically, Welch has done an excellent job of separating YRC’s operating companies from the holding company that has the large debt load. Holland, New Penn, and Reddaway run as independent companies in the regional marketplace, and he tweaked the Yellow and

Roadway long-haul networks to operate profitably. With these moves service has improved, productivity is up, and employee engagement is back.

“Our employees have been through a lot,” says Welch. “We renegotiated labor concessions in the middle of our contract, something we had to do to get the refinancing done. We knew we had to go through that. Our employees had lost a step or two, and it took some time to get that back.”

Welch is also adjusting operations. YRC is asking the Teamsters for greater use of interline carriers—third-party transportation providers—in areas currently served by YRC drivers due to the lack of density in these remote areas.

YRC has also returned to buying new equipment for the first time in about six years. In the first six months of this year, YRC is on pace to acquire 600 new tractors and 2,000 new trailers. “We’re not back to our normal standards, but we’re making nice strides,” says Welch.

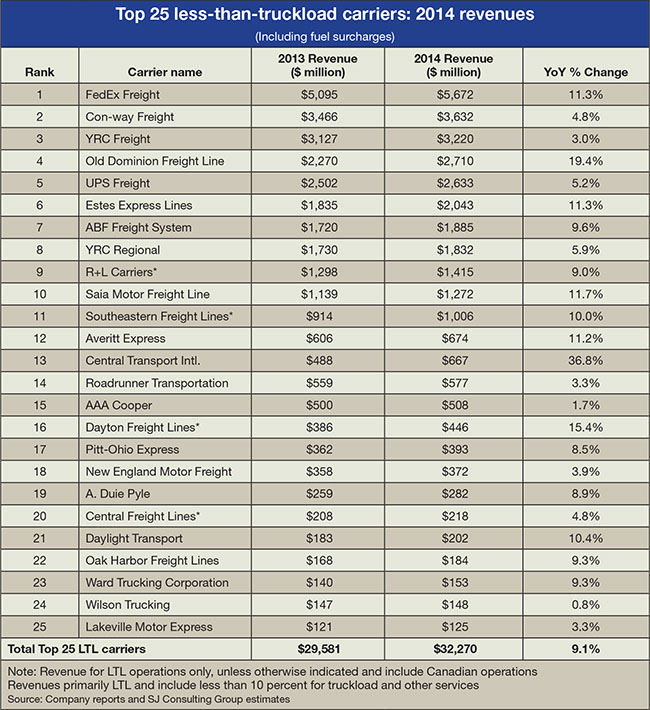

Brian Balius, vice president of transportation for Saia (No. 10 LTL), a multi-regional LTL carrier with 167 locations and 7,500 employees operating in 34 states, says that the carrier is centered around improving the quality experience for shippers. “That means reducing defects, claims, and service failures,” he says.

It must be working. Saia grew revenue by 11.7 percent last year, one of the top growth rates in the LTL sector. Balius says that the carrier is seeing this growth due to investments in retraining employees, raising standards, and making financial investments in rolling stock and equipment such as air bag inflators that go between pallets to optimize trailer space.

Phil Pierce, executive vice president of sales and marketing for Averitt Express (No. 12 LTL), agrees that experienced management and operational teams are priceless. “I’ve been here 33 years, and we’re still growing the business to assure our future,” he says. “We have to bring new ideas to the table to improve and enhance our relationship with our customers.”

Progressive LTL companies such as Averitt and Pitt Ohio (No. 17 LTL) have started offering transportation management systems (TMS) in order for customers to easily plan and track their transportation spend. Logistics Management’s recent Software Users Survey shows that one third of shippers are currently using TMS while another third are looking into the prospect.

“We’ve started offering TMS to our smaller customers,” Pierce explains. “We’re trying to offer things that previously they couldn’t afford on their own.”

Saia and other trucking companies are also eagerly investing in technologies that provide a cost advantage, including telematics for tracking each customer’s freight. The shift to electronic log books also adds efficiencies to operations such as payroll and driver compliance. And then there’s greater use of TMS to help create all-important freight density by carriers eager to achieve as much efficiency on each load.

“Our incremental costs are dramatically less that way,” says Saia’s Balius. “Directionally, the whole magic of logistics is finding carriers that need freight in the direction that shippers have it. That’s what we try to maximize.”

Driver dilemma

According to industry analyst Broughton, attracting and retaining a sufficient supply of compliant truck drivers is the single largest inhibitor to growth in trucking. “I’m sure that there are many TL carriers that would love to grow, but can’t find drivers,” he says. “Money is not the sole answer, but it sure does help.”

Schneider’s Rourke says that the driver situation is as difficult as he can remember—and that’s even with taking several proactive steps to stay ahead of the curve. “We get drivers home every week. Our pay is competitive, and we train drivers for 16 months into an aggressive student program and extend that program an additional five weeks on the road with experience drivers,” he says.

Even so, Schneider says it’s not considering expanding its fleet at this time because of the tightness in the driver supply. Other TL carriers say they are doing the same thing.

Averitt’s Brad Brown says that one of the key components to its driver-training program is mentoring. “We pair younger drivers with older guys for several weeks,” he says. “They get to learn not just driving but safety techniques and the day-to-day challenges of the road. We have finishing schools to teach them more driving skills, such as backing up, giving them a little more confidence.”

There’s no question that carriers are throwing money at the driver problem. Some 42 percent of trucking companies raised driver pay last year, according to the National Transportation Institute’s survey of more than 300 carriers—compared to the 11 percent of that offered raises in 2012.

YRC is recruiting drivers once again, a pleasant enough endeavor for a company struggling with layoffs as recently as 2009. “It’s the first time we have driver recruiters,” says Welch, noting historically that LTL carriers haven’t had problems hiring sufficient drivers.

“We’re really going hard after military,” Welch adds, noting that YRC has joined the U.S. Chamber of Commerce’s “Hiring our Heroes” program. “Vets have been trained well. They’re disciplined, and they’re good workers.”

Capacity and rates

So even with hands-on management teams of the Top 50 trucking companies coping with an array of operational issues, their internal costs are rising at such a degree that rate increases are seen as inevitable for 2015.

In fact, shippers ought to brace for stiff rate increases in their contract renewals. Capacity is tight, and rates should reflect that tightness, carrier executives contend.

“If capacity stays where it is, we’re putting pricing improvement ahead of volume,” says Welch. “From 2008 through 2012, we didn’t stay with the market from a pricing standpoint. We’re taking this opportunity to get pricing and freight mix right, so that’s our priority for 2015.”

Most LTL carriers took a general rate increase of about 5 percent in January. Whether that will suffice for the year is difficult to say in this currently tight freight environment. “My crystal ball isn’t any more pristine than the others,” says Balius. “We’re well prepared to take on additional growth, we’ve invested in sales resources, and we’re optimistic that none of the macroeconomic things will adversely affect this.”

“Our focus is on margins, not so much growing our driver count,” says Schneider’s Rourke. “We think transportation is cyclical, and we want to make sure that we’re nimble and have the ability to adapt and adjust, but adding a bunch of people is a costly endeavor. We think we’re sized in the right way to take advantage of market, whether it goes up or goes down.”

Most executives say shippers should expect rate increases in the 3.5 percent to 5 percent range, perhaps slightly higher on some geographic lanes where capacity is tighter.

However, the strategies of the individual companies comprising the Logistics Management’s Top 50 may change depending on the specific operations and industry niche. But the message from the top senior management teams remains constant: They will be there when and where shippers need them at competitive rates, and they’ll be telling their employees that they are valued members of the team.

Article Topics

Magazine Archive News & Resources

Latest in Materials Handling

Geek+ and System Teknik deploy PopPick solution for pharmacy group Med24.dk Beckhoff USA opens new office in Austin, Texas Manhattan Associates selects TeamViewer as partner for warehouse vision picking ASME Foundation wins grant for technical workforce development The (Not So) Secret Weapons: How Key Cabinets and Asset Management Lockers Are Changing Supply Chain Operations MODEX C-Suite Interview with Harold Vanasse: The perfect blend of automation and sustainability Consultant and industry leader John M. Hill passes on at age 86 More Materials HandlingSubscribe to Materials Handling Magazine

Find out what the world's most innovative companies are doing to improve productivity in their plants and distribution centers.

Start your FREE subscription today.

April 2024 Modern Materials Handling

Latest Resources