2024 Warehouse/DC Outlook Survey: Cautious, but seeking efficiencies

If you thought our annual survey on the outlook for warehouse and DC equipment and systems spending would indicate off-the-charts spending plans, think again. However, you will find interest in goods-to-person robotics, labor management, as well as more respondents tapping third-parties for maintenance analytics as companies look for more efficiencies.

Related Slideshow

Industry analysts predict that after a slow year of growth for warehouse automation in 2023, this year the market will return to faster growth.

But our annual Industry Outlook survey reflects that many organizations are taking a conservative approach to warehouse automation spending plans, with many of the survey’s key spend-related findings trending downward, and a greater proportion of respondents taking a wait-and-see approach.

However, distinct plans and interests are clear, especially for optimizing labor resources. For one, some respondents continue to have substantial budgets for materials handling solutions, and the survey shows growth or strong interest across several categories. The bright spots include increased interest in labor management systems (LMS), high interest in goods-to-person (GTP) robotics, and growing attention to maintenance services and advanced analytics to draw value from existing systems.

Our annual survey, which was in the field during December 2023, drew 101 qualified responses from readers of Logistics Management and Modern Materials Handling involved in materials handling system decisions and warehouse automation. We ask them about how the macro economy is affecting spending decisions, which technologies they’re using or evaluating for best practices, capacity levels, top industry issues, and their methods for measuring performance.

Peerless Research Group’s (PRG) e-mail survey questionnaire was sent to readers of Logistics Management and Modern Materials Handling in December 2023, yielding 101 qualified respondents. The respondents were from sites whose primary activity is corporate headquarters (27%), warehouse/distribution (41%), manufacturing (21%), and warehousing supporting manufacturing (7%). The average annual revenue size for respondent companies was $263.7 million this year—up from $238.1 million last year. Qualified respondents—managers and personnel involved in the purchase decision process for materials handling solutions—hold influence over an average of 103,182 square feet of DC or facility space.

We again shared the results with consultants from St. Onge Company, a supply chain strategy and consulting firm, to get their views on trends they see in the survey and how that stacks up against broader market observations.

While the economy proved resilient at the start of 2024, the survey was fielded at the close of last year, and a cautious approach to spending was understandable, says Don J. Derewecki, senior consultant with St. Onge, given all the continued disruption to the global economy.

“There seems to be a lot of moderation out there, which ties into the level of uncertainty about continuing geopolitical issues and disruptions to global trade, including the wars that are ongoing,” says Derewecki. “High levels of uncertainty are generally going to lead people in the C-suite to hold back on more spending until they get a clearer picture of where things are headed.”

Norm Saenz Jr., managing director and partner with St. Onge, also notes an overall conservative outlook in this year’s survey, but sees high interest in targeted areas like maximizing the productivity of available labor with LMS, or eliminating non-value-added labor time with GTP robotics.

“There are some conservative answers in the survey, but it’s also apparent that many have an open eye toward automation, looking for instance at solutions that help them get more from the labor force,” says Saenz.

Spend numbers

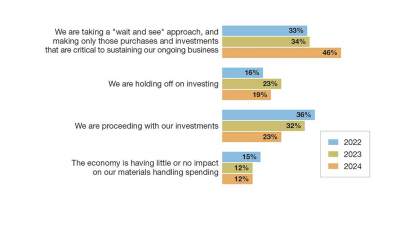

Each year, the survey asks how the present state of the economy is affecting spend on materials handling systems and related technologies. And in this year’s survey, 46% say they are taking a “wait-and-see” approach, up from 34% last year.

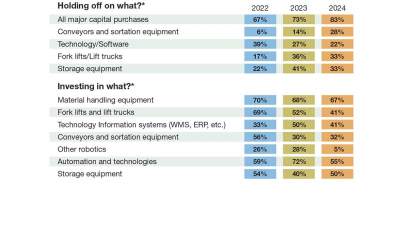

Those who say they are proceeding with investments, given the present state of the economy, also fell, from 32% last year to 23% this year. The survey had a 2% decrease this year in those saying they are holding off investing (19%, down from 23%). When asked what they are holding off on, 83% said all capital purchases, with much smaller percentages holding off on specific types of systems or software.

We also ask those proceeding with investments what they are proceeding with, and 67% said materials handling equipment, 55% said automation and related technologies, and 50% named storage equipment, up by 10% year-over-year.

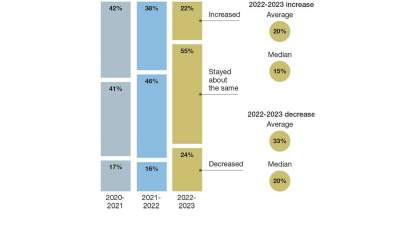

When asked how company spend on materials handling solutions in 2003 compared with 2022, 22% say it increased, down from 38%. Another 55% this year say their 2023 spending “stayed about the same” versus the previous year, whereas last year, 46% answered it stayed level.

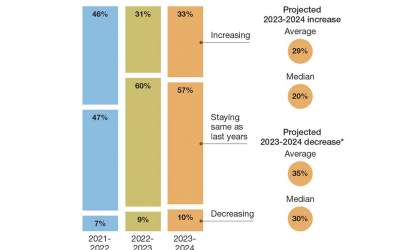

In terms of 2024 spending on materials handling solutions compared to 2023, 33% are predicting higher spend, up from 31%. The majority answer was again “staying about the same,” with a 57% response.

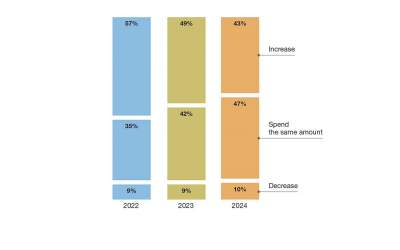

The survey also asks if spending will increase over the next two years to three years, and here caution also prevailed. In particular, 47% predict their companies will spend the same amount on systems over the next two to three years, up from 42%. Those forecasting an increased level stood at 43%, down from 49%.

In terms of anticipated spending, average anticipated spending decreased from $462,634 last year to $329,297 this year. However, the median for this year, at $99,835, was down slightly from $102,360 last year, and a bit higher than two years before.

We ask about spending levels in terms of dollar ranges or brackets, and this year, 4% anticipate spending 2.5 million or more, and 6% marked the range between $1 million and $2.49 million. The bigger percentages were in the middle brackets—12% indicate a spend level over the next 12 months of between $250,000 to $499,999.

When asked the areas in which they will invest over the next 12 months, 58% will spend on new equipment or equipment upgrades, up from 52%. Additionally, 43% plan to invest in IT and software—even with last year. The spend level on staffing/labor also stayed even. However, this year 38% say they would spend on maintenance services, a 4% gain.

This year’s survey found a decrease in the percentage of respondents whose companies have a pre-approved capex budget for materials handling, from 31% last year to 19% this year. However, 30% this year have a budget in excess of $1 million, and the average preapproved budget stands at $482,689, lower than last year’s average, but higher than two years previous.

Derewecki points out that among St. Onge’s clients, many are actively engaged in improvement initiatives and have budget to spend. But when you look at a cross section of the industry, and 30% say they have budget in excess of $1 million, companies will clearly take on substantial projects.

“There is a cautious approach in the survey, but overall, one should view these decisions as a process—what’s the best use of the available budget and other resources you can tap into to improve operations and performance over the long term,” Derewecki says.

Spend category trends

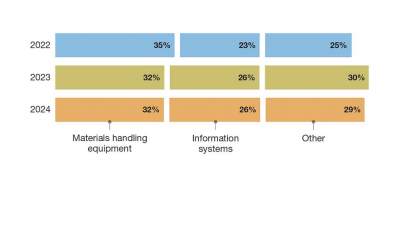

When asked what percentage of overall spending will be on either materials handling equipment, information systems (IS), or “other” over the next 12 months, 32% say equipment, 26% say IS, and 29% say other.

We followed up by asking which categories of equipment respondents will invest in over the next 12 months. The top answers are rack and shelving (38%), mobile and wireless equipment (37%), and lift trucks (32%).

Compared with last year’s response on this question, gaining categories include rack and shelving, up 9%; mobile and wireless, up 6%; and radio frequency identification (RFID), up 9%. Plans for automatic guided vehicles (AGVs) and autonomous mobile robots (AMRs), while down 2% from last year, remain in the mix for 14% of respondents.

When asked the IS subcategories they will spend on, the niche on the rise this year was LMS, cited by 13%, up from 5%. Also making slighter gains were enterprise resource planning (ERP) solutions, up 1% to 21%, while voice picking software was steady at 13%.

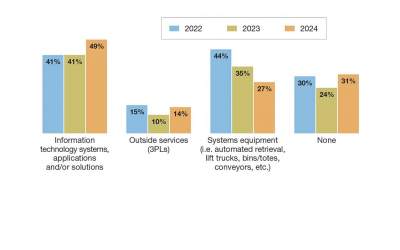

The survey also asked, in regard to new solutions or substantial process changes, which of three broad areas they fall into: use of IT and software; use of 3PLs; and various “system equipment” such as automated retrieval, lift truck, totes or conveyors. The big gainer here was IT, indicated by 49% this year, up from 41%. Use of 3PL services rose to 14%, while system equipment purchases decreased from 35% last year to 27% this year.

Performance measures

The survey also asks about methods for gauging productivity, today and two years out, including whether the measures are automatically generated by software. Once again, our survey finds that managers have intense interest in being able to assess factors such as inventory levels, on-time shipment, and shipment accuracy, in an automated manner.

For example, measuring on-time shipments is an automated process for 32% today, but 56% want this automated within two years. Likewise, order fulfillment cost tracking is automated for 27% today, but 45% want to automate within two years. Another big delta is seen with inventory accuracy, an automated metric for 26% today, but 61% want to have this automated within two years.

Taken in combination with the healthy interest level in LMS, the high interest in a more automated approach to performance measures shows companies are looking to be more data driven, notes Saenz.

“You can see in the survey results that companies are looking to harness data more effectively, whether it’s to have better metrics to help them make smart decisions on a daily basis, or in motivating and managing their workforce in a better way,” says Saenz. “This interest in being more data driven is one of the more encouraging trends from this year’s survey.”

When it comes to plans for mobile technologies, the net percentage having at least some plans fell from 69% to 48% this year. Some mobile technology niches, however, show interest when asked about plans over the next 12 months.

This includes RFID tags, in use by 28% today, but 40% having plans for RFID tags in the coming year; drones, in use by 6% today but 29% have plans or interest. Voice technology is in use by 16% today, but 20% have some voice technology plans over the next 12 months.

Robotics interest sticks

While some declines showed in terms of current “in-use” levels for AGVs/AMRs, and for industrial robot solutions (articulating arm robots or cobots), the percentages looking to evaluate robotics solutions trended higher.

This year, while 13% are using AGVs or AMRs (down from 18%), 23% have plans to, which is up by 3%. Similarly, fixed robots are in use by 10% this year, down from 25%, but this year 24% are evaluating articulating arm robotics, up from 18%.

We also ask which applications AGVs, AMRs, and industrial robots will be used for. Growth applications for AMRs and AGVs this year include storage, with 48% having interest, up from 33% last year, as well as order fulfillment, part-to-picker (a GTP workflow) reached 52% using AMRs in this fashion, up from 38%.

For fixed-position robotics, applications that garnered a higher interest level this year include order fulfillment, part-to-picker systems, cited by 42%, up from 14%; truck unloading, cited by 31% this year, up from 7%; and packaging or packing robotics, cited by 39%, up from 28%.

Maintenance, capacity trends

The survey also asks about who performs the maintenance function for materials handling systems, and the leading answer is again in-house staff, cited by 62% of respondents this year, up from 54%. However, as multiple choices were allowed, we saw a slight uptick in outsourced maintenance (now at 20%) and 27% use a combination of in-house and third-party resources, up from 23%.

When asked what role automation vendors or third parties play in maintenance (regular maintenance, upgrades, consulting, data analysis or other), this year, the leading role was overall maintenance (51%) up from 40%.

There were also modest gains in those using third-parties for maintenance (now 40%, up from 36%) and data analysis (now 23%, up from 19%). Using vendors for data analysis is on the rise, cited by 26% this year, up from 23%. This marks three years running survey respondents have indicated an increased use of suppliers for maintenance analytics.

Data analysis for predictive maintenance, or even analytics that uncover the root cause of recent downtime events, can be an advantage to more heavily automated DCs, notes Saenz, but it can take special skills that some will end up tapping suppliers for. “These systems are always generating data, and there can be efficiencies to be found in that data,” says Saenz.

The survey also tracks DC activity/capacity levels across manufacturing, warehouses serving manufacturing, and stand-alone DCs, and again this year, the trends point to high utilization for many. For example, when we asked about activity/capacity level for stand-alone warehousing, 32% have between 81% and 99% capacity level, and another 2% say they are at 100%.

Generally, most operations would like to be in the 71% to 80% capacity range to allow some locations/room for extra volume during peaks, without being underutilized. This year, 16% of respondents were in that 71% to 80% capacity range.

In asking respondents with stand-alone DCs if they expected activity level to change over the next two years, 37% expect it to increase, down from last year’s 43%, while 55% expect the level to stay about the same, up from 46%.

Industry issues

Each year, we ask respondents to rate how important a set of key issues are to their operations today, and looking two years out, how important these issues will be then. This year, we found the top four issues were safety (68%); cost containment (65%); labor availability (58%); and company growth (58%). Compared to last year’s top four, cost containment, which was in fifth last year, grew in importance.

Additionally, this year when rating issue importance two years out, cost containment rose to 72%; safety dipped to 63%, labor availability fell to 52%, and the importance of company growth rose to 70%. Clearly, this year’s respondent pool reflects perceived pressure to contain costs and foster growth, even as labor availability continues to be a top challenge.

The survey also looks at how e-commerce orders are fulfilled, today and two years out. The most common practice today is to “buy-online, ship to customer from a DC,” in use by 33% today and expected by 35% respondents two years from now. Today, 20% practice “buy-online, ship to customer from vendor” (or “drop ship”), and this is forecast to stay at 20% two years from now. Additionally, “buy online, ship from store” held at 16%.

When asked where packaging and fulfillment occurs, the leading place (multiple answers were allowed) is a warehouse (51%), followed by manufacturing (42%), while 33% name DCs, and another 15% say fulfillment centers.

Given the stream of global threats and disruptions late last year, another surprise in the survey was 31% say they have a plan for evaluating and mitigating top supply chain risks, down from 55%. Of those with plans, the top three areas were logistics risks, supplier risks, and data breaches, with the latter climbing by 12%.

Risk planning is always a good idea, says Derewecki, who notes: “If you don’t have a plan for a risk, then when an event does happen, you’re just going to be reacting and when you react, that’s suboptimal.”

The larger takeaway from the study, Derewecki and Saenz note, is that operations continue to invest in new systems and equipment, but in a more targeted way, often looking for data insights and analytics to help them squeeze more uptime from existing systems or help their workforces be more productive.

“We also see strong interest in the market in goods-to-person solutions, and in labor management software, and in putting in place solutions that help associates with their daily tasks, and help supervisors manage the workforce,” says Saenz. “It’s important to remember that automation alone can’t solve every DC operations challenge—you also have to manage the workforce better through solutions like LMS projects, maybe even establishing an incentive program. It’s important to remember that having an effective, motivated labor force is still foundational for most operations out there.”

Article Topics

Peerless Research Group News & Resources

2024 Intralogistics Robotics Survey: Robot demand surges 2024 Warehouse/DC Outlook Survey: Cautious, but seeking efficiencies We love research The employee satisfaction survey: Don’t worry, be happy MRO Survey: Finding and keeping the best technicians 2024 Automation Study: How automation is transforming the warehousing landscape Top 20 Warehouses 2023: Demand soars and mergers slow More Peerless Research GroupLatest in Materials Handling

Geek+ and System Teknik deploy PopPick solution for pharmacy group Med24.dk Beckhoff USA opens new office in Austin, Texas Manhattan Associates selects TeamViewer as partner for warehouse vision picking ASME Foundation wins grant for technical workforce development The (Not So) Secret Weapons: How Key Cabinets and Asset Management Lockers Are Changing Supply Chain Operations MODEX C-Suite Interview with Harold Vanasse: The perfect blend of automation and sustainability Consultant and industry leader John M. Hill passes on at age 86 More Materials HandlingAbout the Author

Subscribe to Materials Handling Magazine

Find out what the world's most innovative companies are doing to improve productivity in their plants and distribution centers.

Start your FREE subscription today.

April 2024 Modern Materials Handling

Latest Resources