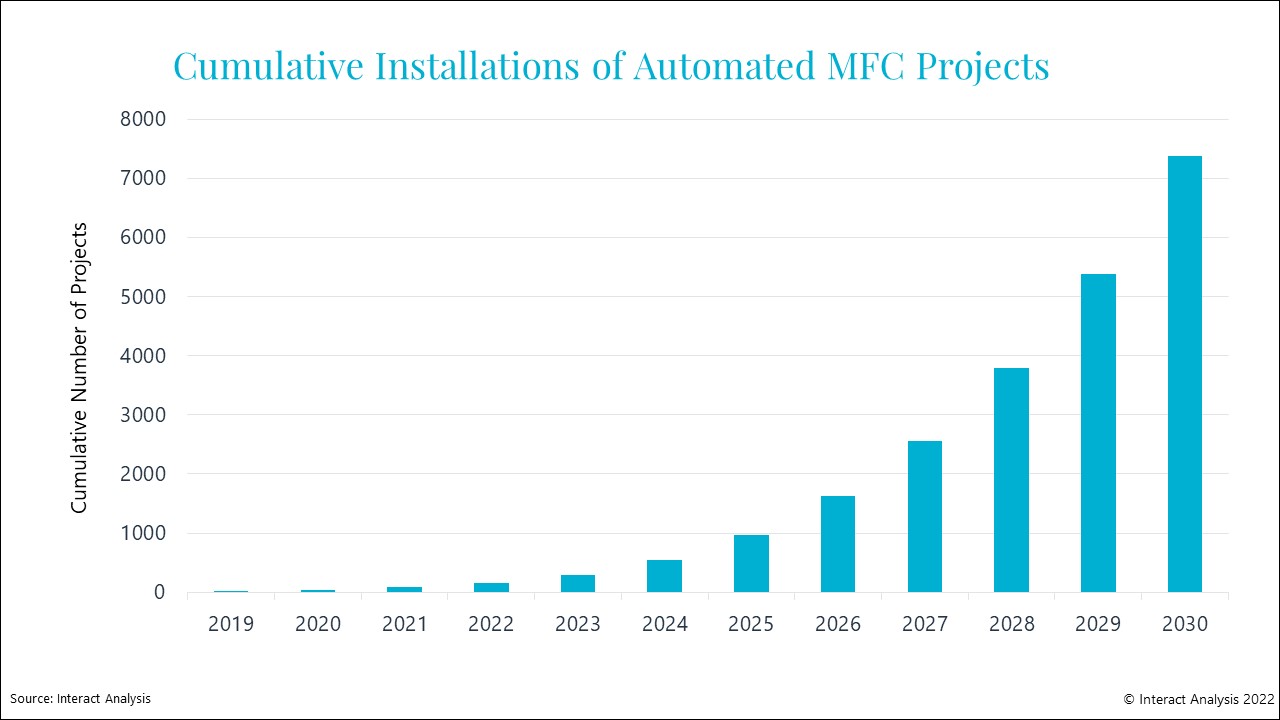

Analyst study: 7,300 automated micro-fulfillment centers to be installed by 2030

Interact Analysis research finds for that for the near future, much of the growth in the automated MFC market will come from the large incumbent grocery retailers, but rapid delivery companies may also invest in automated MFCs longer term.

New research from Interact Analysis shows that just under 7,300 automated micro-fulfillment centers (MFCs) will be installed by the end of 2030, up from just 86 at the end of 2021. With growth in the short-run mainly driven by demand for same-day grocery delivery, the analyst firm added.

In the near future, much of the growth in the automated MFC market will come from the large incumbent grocery retailers, such as Walmart and Tesco, as they strive to offer same-day delivery services. Conversely, demand from non-grocery retailers is far smaller due to a slower uptake of same-day deliveries. The research defines automated MFCs as fulfillment centers smaller than 50,000 ft2, or as automation installed in the back of a store. And it splits potential customers into two categories: grocery (where more than 50% of revenues is from grocery), and non-grocery retailers.

Additionally, Interact Analysis explained, the rapid-delivery companies have so far been slow in deploying automated MFCs. That’s because they’ve been focusing more on network expansion and customer acquisition rather than driving operational efficiency through automation. However, the rapid delivery market will likely undergo a period of consolidation in the coming years which will lead to a strong focus on profitability per delivery site – and investment in automation.

Of the total installed base of 86 automated MFCs at the end of 2021, Takeoff Technologies accounted for 23%. It was one of the first companies to offer automated MFC solutions, allowing it to gain a substantial market share. Following closely behind, Swisslog accounted for 21% of installed projects by the end of 2021. Swisslog is now working with HEB and others to install Autostore systems in MFCs across the US. Meanwhile, Dematic accounted for only 14%. However, this is likely to increase significantly as a result of their collaborations with Walmart and Tesco.

Rueben Scriven, Senior Analyst at Interact Analysis, commented: “There’s no doubt that the growth in the automated MFC market has been slower than expected. This is partly driven by supply-chain constraints and permitting delays, although Instacart’s white-label services are also calling into question the need for in-house fulfillment assets for some grocers. However, while incumbent grocers have been slower to adopt automated MFCs, the phenomenal growth of rapid delivery companies and the Q-commerce market has significantly increased the addressable market, driving future growth.”

The report used extensive primary research interviews with leading retailers, MFC vendors, and software providers, and is said to provide an in-depth analysis of the micro-fulfillment center landscape, covering both automated and manual sites.

Article Topics

Interact Analysis News & Resources

Forklift market to be 50% bigger by 2032, Interact Analysis forecasts Interact Analysis: warehouse automation market to return to growth in 2024 Chinese warehouse automation market set to grow at CAGR of 13.5% over next 5 years Interact Analysis: warehouse construction declines by 25% in 2023 ‘Steady’ growth of 5-7% forecast for global industrial robot market Robotic picking market worth $6.8 billion by 2030, up from $236 million last year Interact Analysis: logistics and other new application scenarios key to cobot market success More Interact AnalysisLatest in Materials Handling

AutoStore to launch U.S. headquarters in greater Boston region Trew expanding manufacturing and development campus in southwest Ohio IFR: robot installations by U.S. manufacturing companies up 12 percent last year Geek+ and System Teknik deploy PopPick solution for pharmacy group Med24.dk Beckhoff USA opens new office in Austin, Texas Manhattan Associates selects TeamViewer as partner for warehouse vision picking ASME Foundation wins grant for technical workforce development More Materials HandlingSubscribe to Materials Handling Magazine

Find out what the world's most innovative companies are doing to improve productivity in their plants and distribution centers.

Start your FREE subscription today.

April 2024 Modern Materials Handling

Latest Resources