Chinese warehouse automation market set to grow at CAGR of 13.5% over next 5 years

Interact Analysis details findings on the warehouse automation market in China, including domestic warehouse automation suppliers gaining market share.

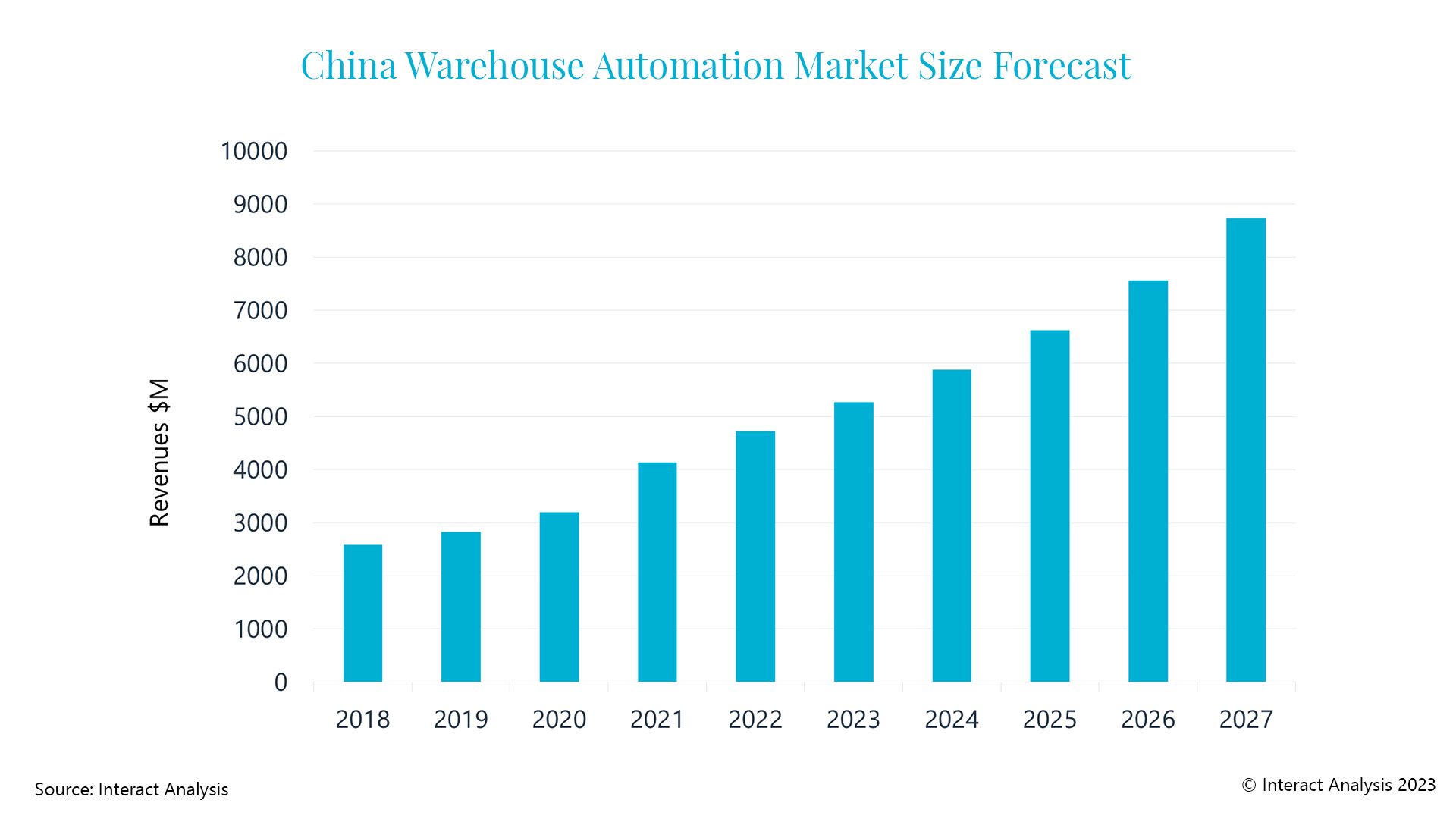

The Chinese warehouse automation market has fared well over the past five years, maintaining a market growth rate of around 16%, with steady growth expected to continue over the next five years, according to a new research report from market intelligence firm Interact Analysis.

In 2022, the Chinese warehouse automation industry was worth $4.72 million, compared with $2.59m in 2018, Interact's research finds. The parcel, durable manufacturing and general merchandise sectors have been largely responsible for driving this growth, registering CAGRs of 22.1%, 22.5% and 18.4% respectively. Between 2023 and 2027, the outlook for the market is still rosy as companies continue to look for ways to optimize efficiency on the factory floor, with a CAGR of 13.5% predicted by Interact Analysis.

International suppliers have played a significant role in China’s warehouse automation industry. However, Interact Analsys noted it is now beginning to see a gradual decline in the share of business taken by international suppliers, as domestic suppliers gain a competitive advantage. International suppliers held a substantial share of the Chinese fixed warehouse automation market in 2018, but this has been declining over time. This is largely because local suppliers have a clear price advantage compared with international vendors, Interact added. Furthermore, Chinese suppliers are often able to offer more flexible solutions that can be tailored to the needs of the customer and have greater knowledge of the Chinese market and economy, further boosting their competitive advantage. Chinese suppliers have also been successfully expanding into overseas markets.

“There are four main drivers of growth for the Chinese warehouse automation market," said Irene Zhang, senior analyst at Interact. "Firstly, China’s economic growth has remained strong over the past few decades, while, secondly, government support and promotion of warehouse automation has boosted the market significantly. Our research provides detailed analysis of government subsidies that warehouse automation suppliers have received, of which make up a substantial amount of their net profits."

As with many countries across the globe, labor costs continue to rise in China, Zhang added, which has led many companies to re-evaluate their strategy and implement warehouse automation solutions in order to reduce costs. Additionally, the localization of warehouse automation equipment has driven down the price of components such as sensors and PLC’s, further increasing Chinese vendors’ competitive advantage.

However, where there are drivers for market entry there are also barriers, Zhang added. "Project implementation cycles tend to be longer in China due to a lack of experience and expertise among some local suppliers, which hampers growth of the market," Zhang said. "Additionally, although labor costs are high, the labor force is plentiful in China compared with other countries, such as the US. This means there is an abundant supply of blue-collar workers and less of an incentive to invest in automation.”

Overall, the mobile warehouse automation market has grown at a faster pace in China than that of fixed warehouse automation, the Interact Analysis report also found.

Article Topics

Interact Analysis News & Resources

Forklift market to be 50% bigger by 2032, Interact Analysis forecasts Interact Analysis: warehouse automation market to return to growth in 2024 Chinese warehouse automation market set to grow at CAGR of 13.5% over next 5 years Interact Analysis: warehouse construction declines by 25% in 2023 ‘Steady’ growth of 5-7% forecast for global industrial robot market Robotic picking market worth $6.8 billion by 2030, up from $236 million last year Interact Analysis: logistics and other new application scenarios key to cobot market success More Interact AnalysisLatest in Materials Handling

Geek+ and System Teknik deploy PopPick solution for pharmacy group Med24.dk Beckhoff USA opens new office in Austin, Texas Manhattan Associates selects TeamViewer as partner for warehouse vision picking ASME Foundation wins grant for technical workforce development The (Not So) Secret Weapons: How Key Cabinets and Asset Management Lockers Are Changing Supply Chain Operations MODEX C-Suite Interview with Harold Vanasse: The perfect blend of automation and sustainability Consultant and industry leader John M. Hill passes on at age 86 More Materials HandlingSubscribe to Materials Handling Magazine

Find out what the world's most innovative companies are doing to improve productivity in their plants and distribution centers.

Start your FREE subscription today.

April 2024 Modern Materials Handling

Latest Resources