Top 20 industrial lift truck suppliers, 2017

The top lift truck suppliers list is changing with industry acquisitions causing a dramatic departure from the norm.

This year’s list of the Top 20 Lift Truck Suppliers is unlike any other in the more than 70-year history of this magazine. Although the company names are familiar, the makeup of the top two has changed substantially since this time last year. Toyota acquired systems integrators Bastian Solutions and Vanderlande Industries, and KION acquired Dematic, which is ranked No. 3 on Modern’s Top 20 Systems Suppliers list.

These developments constitute a dramatic departure from the norm, according to Brett Wood, chairman of the Industrial Truck Association (ITA) and president and CEO of Toyota Material Handling North America.

“I like to think of it as Consolidation 2.0,” he says. “In the past, acquisitions tended to be like for like; forklift manufacturers acquired other forklift manufacturers, and automation companies acquired automation. Under the new paradigm, we’re witnessing acquisitions across different segments. It’s the first time the materials handling world has seen this kind of cross-pollination.”

Consolidation might not even be the right term, Wood concedes. What’s happening is a true merging of technologies and products with an eye toward approaching customers with a message of “one-stop shopping.”

“In the near future, customers will use one supplier for anything they need in the warehouse,” Wood says. “It’s great news for the customer, who will be able to focus all their energy on one or two suppliers and do what they do best without worrying about materials handling needs.”

In the meantime, the global forklift industry is in the midst of robust growth, reaching all-time highs in 2016 as orders topped 1,182,000, up 7% from 2015, which set the previous record. The performance of the Top 20 suppliers reflects this growth, with several posting double-digit gains.

“I don’t think any of us expected that,” Wood says. “It really outperformed all expectations. In fact, we might have expected a slowdown by now due to the cyclicality of our industry, but we’re not complaining.”

The Top 10

Toyota Industries Corporation (TICO) retained the No. 1 spot with $8.563 billion. After the company reclassified its logistics segment, it amended its fiscal year ’15-’16 figures upward from $8.346 billion as reported in last year’s list to $8.559 billion. As a result, Toyota’s revenues are effectively flat for fiscal year ’16-’17.

TICO’s net sales of materials handling equipment totaled 1,001.5 billion yen, a decrease of 3% attributable mainly to the impact of exchange rate fluctuations despite an increase in unit sales in European, Japanese and other markets.

According to a TICO representative, the materials handling equipment market as a whole continued to expand globally due mainly to increases in unit sales in Europe and North America as well as a recovery in China, although unit sales in Japan were on par with the previous fiscal year.

The representative added that the acquisitions of Bastian Solutions and Vanderlande Industries were a response to “structural changes in the logistics industry and in order to strengthen Toyota Industries’ logistics solutions business on a global scale.”

In second place, KION grew 4% to $5.879 billion. In early 2017, the company launched five new models of its Linde and Baoli brands developed for the North American market. At the time, Vincent Halma, president and CEO of KION North America, said “the rate at which we’re releasing new products and services is truly unprecedented.” KION also recently announced plans to expand its South Carolina facility capacity to 12,000 lift trucks a year by 2020, up from 3,000 in 2015.

Following its acquisition of last year’s seventh-place finisher UniCarriers, effective Jan. 1, 2017, Mitsubishi Nichiyu Forklift is now in third place, up from sixth. The reported revenues are a tentative figure based on consolidation for the financial year 2016, with UniCarriers converted into a wholly owned subsidiary.

The combination of Mitsubishi and UniCarriers moves Jungheinrich to No. 4 despite its strong performance in 2016. The company grew 8.5% year-on-year in USD, and 12% in Euro. This reflects an order intake of 109,200 forklifts (+12.5%) and 106,300 units produced (+16.6%). Jungheinrich also expanded its global sales and service network, bringing its worldwide presence to 36 countries.

“The Jungheinrich Group posted significant increases in all key performance indicators in 2016,” says Hans-Georg Frey, chairman of the board of management of Jungheinrich AG. “The main growth drivers were new truck business and the Logistics Systems Division. For the first time, we surpassed the €3 billion mark in terms of net sales and incoming orders.”

Crown Equipment is fifth after growing more than 10% to finish 2016 with just shy of $3 billion in revenues.

Sixth-ranked Hyster-Yale Materials Handling held flat this year at $2.57 billion. A spokesperson cited “lower unit volumes, the unfavorable effect of deal-specific selling prices, the strong U.S. dollar, and a shift in sales to lower-priced lift trucks during 2016 compared with 2015.”

The decline in lift truck revenue was partially offset by revenues from Bolzoni, which Hyster-Yale acquired in April 2016 for $61 million. The Italian manufacturer of lift truck attachments under the Bolzoni Auramo and Meyer brand names had consolidated revenues of $152.6 million for the 12 months ended Sept. 30, 2015. Bolzoni is expected to continue to operate as a stand-alone business, with its own management team and board of directors.

Anhui Forklift grew 2.3% to No. 7. The company launched a new brand, CHL, in 2016, which is intended for the emerging market. For the year, its sales totaled 86,625 units, an increase of 16%.

After greater than 10% growth to $781 million in revenues, Doosan jumped from 11th to 8th place on our list.

Achieving nearly 10% growth, Hangcha Group sold 82,350 units across all forklift classes, an increase of more than 23%, and good enough to climb from No. 12 in 2015 to No. 9. The company was published on the Chinese Shanghai Stock Exchange at the end of 2016.

“With the benefit of China’s government’s strategy, including the reform of the supply front, China’s manufacturing industry started to recover mildly with released potential of domestic demands,” a representative writes.

Clark Material Handling again holds 10th place after a flat 2016. Celebrating its 100th anniversary, 2016 was a solid year globally for Clark, says Scott Johnson, vice president of sales and marketing. The company’s global manufacturing platform includes plants in China, South Korea and Lexington, Ky., where its North American headquarters now has full production capabilities for six models. The company is also preparing for several new product releases in 2017.

Growth by region

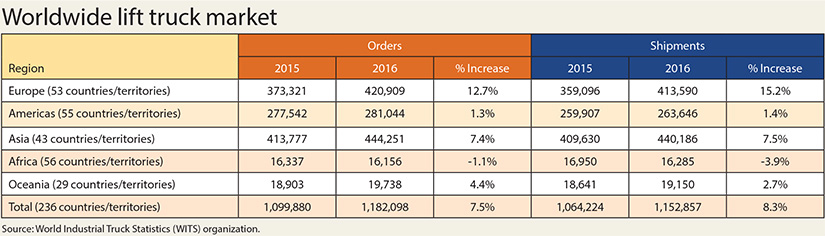

The Worldwide Industrial Truck Statistics (WITS) organization tracks quarterly and monthly statistics on lift truck sales and its report is compiled by six trade groups based in North America, Brazil, Japan, Korea, Europe and China.

According to the 2016 WITS figures, global orders increased by 7.5% and world shipments by 8.3%. This follows 2015’s flat orders and shipments, and 2014’s 8% order increase.

Additional highlights of the 2016 WITS figures include:

- Accounting for 35% of the market, Europe again has the largest growth, breaking double digits for the first time in years with an increase of 13%. Orders increased by more than 47,000 units, while shipments grew by nearly 55,000, a 15% increase.

- The Americas region improved slightly from 2015’s all-time high, with 281,000 orders, and this region now accounts for 24% of the market.

- Following Europe’s strong growth, the Asia region now accounts for 38% of global shipments and orders, down from greater than 40% in recent years. It is still the largest region despite last year’s 6% decline, but rebounded with orders and shipments topping 7%.

- Class 3 lift trucks (electric hand trucks or hand/rider trucks with solid tires) grew by 14% in orders and 16% in shipments, nearly double the growth rate of any other class. Classes 4 and 5 (internal combustion) each grew by 2%.

Electric continues its charge

For decades, the ratio of electric to internal combustion (IC) sales swung back and forth, but the electric segment has dominated in recent years and experts agree the pendulum is unlikely to swing back. Following 8% growth in 2015, electric products grew a further 11% last year. IC fell 10% in 2015, but has recovered somewhat with 2% gains in 2016. Globally, electrics now account for 62% of all sales, up from 60% in 2015.

In North America—which also set a record last year—the electric ratio went from 63% in 2015 to 65.5% in 2016. The North American electric truck market grew 6%, whereas the IC market was down 5%. The IC decline was almost entirely centered on Class 4, indoor cushion tire equipment, which fell 11% as Class 5 remained flat.

Classes 2 and 3, the smaller electric lift trucks used for indoor warehousing applications, also gained against Classes 1, 4 and 5, the larger counterbalanced trucks. “That’s a very important trend that I found very interesting,” Wood says. “Globally, those warehouse trucks were 42% of the market and are now 45%. Over the years I’ve seen maybe a 1% shift in any one year. When you’re talking about a million trucks, that’s still a big number, but to see a 3% shift means the needle is moving.”

Wood expects the electric warehouse product segment will continue to grow. Although developed regions like Europe and North America will lean toward electric in response to e-commerce and sustainability initiatives, emerging regions still rely heavily on IC and counterbalanced equipment.

As electric and IC jockey for market share, Wood also notes progress among alternative power sources like lithium-ion and fuel cells. “I might have been a bit cool on fuel cells a few years ago, but I think they are starting to get more traction,” he says. “It’s now worth taking notice of those opportunities.”

Top 20 Industrial lift truck suppliers |

ITA class of trucks manufactured |

|||||||||||

|

2016 Rank |

Company |

2015 Rank |

2015 |

2016 |

% Change 2015-2016 |

North American brands |

World headquarters |

|||||

|

Class 1 |

Class 2 |

Class 3 |

Class 4 |

Class 5 |

||||||||

|

|

1 |

8559 |

8563 |

0% |

Toyota, Raymond |

Aichi, Japan |

x |

x |

x |

x |

x |

|

|

|

2 |

5659 |

5879 |

3.9% |

Linde, Baoli |

Wiesbaden, Germany |

x |

x |

x |

x |

x |

|

|

|

6 |

2012 |

3407 |

69.3% |

UniCarriers, Mitsubishi, CAT, TCM, Atlet, Barrett, Jungheinrich (NA only) |

Kyoto, Japan |

x |

x |

x |

x |

x |

|

|

|

3 |

2998 |

3252 |

8.5% |

Sold in NA by MCFA |

Hamburg, Germany |

x |

x |

x |

x |

||

|

|

4 |

2640 |

2910 |

10.2% |

Crown, Hamech |

New Bremen, Ohio |

x |

x |

x |

x |

x |

|

|

|

5 |

2578 |

2570 |

-0.3% |

Hyster, Yale |

Cleveland, Ohio |

x |

x |

x |

x |

x |

|

|

|

8 |

907 |

928 |

2.3% |

Heli, CHL |

Hefei, Anhui, China |

x |

x |

x |

x |

x |

|

|

|

11 |

706 |

781 |

10.6% |

Doosan |

Seoul, South Korea |

x |

x |

x |

x |

x |

|

|

|

12 |

704 |

774 |

9.9% |

HC, Hangcha |

Hangzhou, China |

x |

x |

x |

x |

x |

|

|

|

10 |

739 |

740 |

0.1% |

Clark |

Seoul, South Korea |

x |

x |

x |

x |

x |

|

|

|

9 |

760 |

616 |

-18.9% |

Komatsu |

Tokyo, Japan |

x |

x |

x |

|||

|

|

13 |

477 |

477* |

0% |

Hyundai |

Ulsan, South Korea |

x |

x |

x |

x |

||

|

|

14 |

212 |

227 |

7.1% |

Combilift |

Monaghan, Ireland |

x |

x |

x |

x |

x |

|

|

|

16 |

160 |

200 |

25.0% |

Big Joe |

Hangzhou, China |

x |

x |

x |

x |

||

|

|

N/A |

185 |

185* |

0% |

Konecranes |

Hyvinkää, Finland |

x |

|||||

|

|

15 |

163 |

163* |

0% |

Lonking |

Shanghai, China |

x |

x |

x |

x |

x |

|

|

|

N/A |

115 |

136 |

18.3% |

Manitou |

Ancenis Cedex, France |

x |

x |

x |

x |

||

|

|

18 |

76 |

76* |

0% |

Hubtex |

Fulda, Germany |

||||||

|

|

19 |

69 |

69* |

0% |

Paletrans |

Cravinhos, Brazil |

x |

x |

||||

|

|

20 |

63 |

67 |

6.3% |

Not available in North America |

Mumbai, India |

x |

x |

x |

x |

x |

|

|

Figures based on currency exchange rates as * 2016 revenues were not available by press time. Source: Modern Materials Handling |

TOTAL |

|

|

|

||||||||

Rest of the list

Several companies at the bottom half of the list were unable to report revenues by press time, so 2015 revenues have been carried over. These companies are: 12th-place Hyundai, 15th-place Konecranes, 16th-place Lonking, 18th-place Hubtex and 19th-place Paletrans.

At No. 11, Komatsu dropped two spots after 2016 revenues decreased by nearly 19%. Up one spot to No. 13, Ireland-based Combilift, makers of four-directional forklifts, side-loading equipment and straddle carriers, grew 7% after selling 4,350 units in 2016, an 11.5% increase from the previous year. In 2016, the company also launched its new multi-directional, stand-on reach truck.

After growing 25%—the highest organic growth rate on the list—EP Equipment finished 2016 with $200 million in revenues, reflecting a 33% growth in unit sales to 32,000.

France-based Manitou, a newcomer to our list, produced 5,566 units in 2016, an increase of 10% from 2015. Industrial truck revenues totaled $136 million for the year, an 18% increase. The company announced plans to introduce 14 industrial forklifts to the North American market. Manitou Americas, which operates three manufacturing facilities in the United States, will introduce the new models through 2017 and 2018.

Rounding out our list, Godrej and Boyce moved 3,088 units in 2016, a nearly 22% increase from the previous year. A spokesperson says the company’s materials handling equipment segment grew 7%, while the company as a whole grew 13%. “India’s GDP was up 7.2% last year with growth in all major sectors like automotive, retail, etc.,” the spokesperson adds.

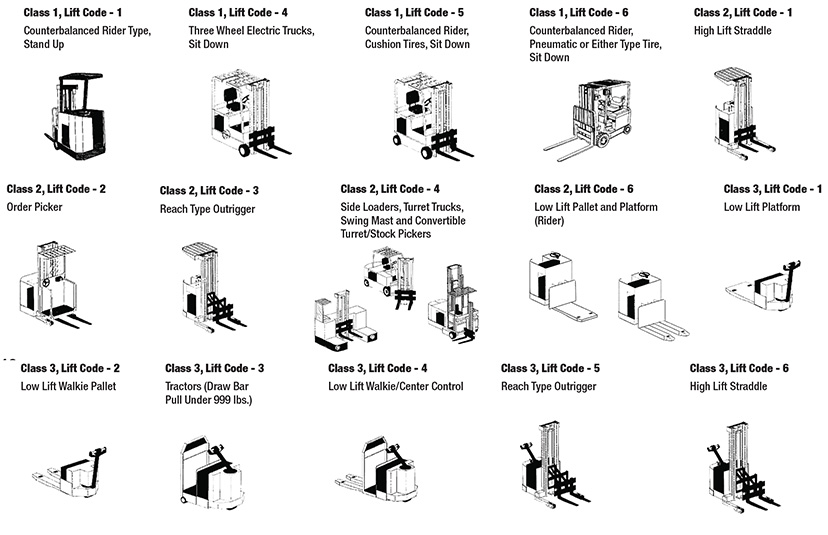

ITA’s lift truck classes

The Industrial Truck Association (ITA, indtrk.org) has defined seven classes of lift trucks, or forklifts, which are defined by the type of engine, work environment, operator position and equipment characteristics.

Lift truck classes include:

- Class 1: electric motor trucks with cushion or pneumatic tires

- Class 2: electric motor narrow aisle trucks with solid tires

- Class 3: electric hand trucks or hand/rider trucks with solid tires

- Class 4: internal combustion engine sit down rider forklifts with cushion tires, suitable for indoor use on hard surfaces

- Class 5: internal combustion engine sit down rider forklifts with pneumatic tires, suitable for outdoor use on rough surfaces

- Class 6: electric or internal combustion engine powered, rider units with the ability to tow (rather than lift) at least 1,000 pounds

- Class 7: almost exclusively powered by diesel engines with pneumatic tires, these units are suitable for rough terrain and used outdoors.

Since primarily classes one through five are used in materials handling applications inside the four walls, Modern has only specified those on our supplier table.

Article Topics

Special Reports News & Resources

Automation/Retail Special Issue: Savvy users embrace change Research Report: Use of Automation in Warehouse/DC Special Digital Issue: Warehouse/DC Robotics System Report: Building the world’s best warehouse Top 20 Warehouses 2019 Top 20 automatic identification and data capture suppliers 2019 Top 20 Lift Truck Suppliers in 2019: Market reaches new heights More Special ReportsLatest in Materials Handling

Geek+ and System Teknik deploy PopPick solution for pharmacy group Med24.dk Beckhoff USA opens new office in Austin, Texas Manhattan Associates selects TeamViewer as partner for warehouse vision picking ASME Foundation wins grant for technical workforce development The (Not So) Secret Weapons: How Key Cabinets and Asset Management Lockers Are Changing Supply Chain Operations MODEX C-Suite Interview with Harold Vanasse: The perfect blend of automation and sustainability Consultant and industry leader John M. Hill passes on at age 86 More Materials HandlingAbout the Author

Subscribe to Materials Handling Magazine

Find out what the world's most innovative companies are doing to improve productivity in their plants and distribution centers.

Start your FREE subscription today.

April 2024 Modern Materials Handling

Latest Resources